The Howard Government heralded its New Tax System (ANTS) and the Goods and Services Tax (GST) as a major reform of Australia's taxation system that would also enhance the financial capacity of Australia's states and territories to provide community services.

It was claimed these reforms would arrest the erosion of states' and territories' fiscal capacity, which occurred with the Commonwealth expanding its role in the social and economic affairs of the nation over the course of the 20th century. In reality, ANTS and the GST have done exactly the opposite. Furthermore, recent comments from the Federal Treasurer suggest these reforms will provide the means by which the Commonwealth strengthens its control over state and territory finances, and as a consequence, their policy and budgetary priorities.

As such, ANTS has been yet another manifestation of the “creeping centralisation” within the institutional design of the Australian federation, a dynamic which continues to be the dominant force shaping the relationship between the Commonwealth and the states and territories. For contrary to the claims of the Commonwealth, ANTS and its embedding of the GST at the core of the complex set of financial relations at the heart of Australian federalism is further diminishing the fiscal autonomy of the states and territories by making them increasingly reliant upon a revenue source over which they have no control.

Advertisement

The fiscal dominance of the Commonwealth

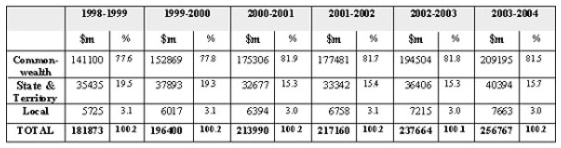

As well as enhancing the Commonwealth's budgetary position, the implementation of ANTS has reinforced the Commonwealth's fiscal dominance within the federation as the responsibility for revenue collection is being further centralised with the Commonwealth. As shown in the following table, the Commonwealth collected 77.6 per cent of total Australian taxation in 1999-2000. Since the introduction of GST, the Commonwealth share of total taxation collections has remained in the range of 81.5 per cent to 81.9 per cent. Over the same period, the proportion of total taxation collected by the states and territories slumped from 19.5 per cent to less than 16 per cent, with the share of total taxation collected by local governments remaining steady at around 3 per cent.

Australian Taxation - Proportion of Total Taxation Raised by Tier of Government 1998-2004

State and territory revenue

As the Commonwealth assumes a greater level of responsibility for raising revenue within the federation, the states and territories are becoming increasingly reliant upon Commonwealth payments to support their expenditure programs. The change in the structure of the states' and territories' revenue base since the introduction of the ANTS reforms can be clearly seen in the following graph, which shows the growing importance of grants and subsidies, overwhelmingly Commonwealth transfers to state and territory budgets.

State and Territory Governments - General Government Operating Statements (Revenue) 1999-2004

Advertisement

Source: ABS Government Finance Statistics 1999- 2004 Cat. No. 5512.0

Controlling the agenda: Section 96

The increasing fiscal dependence of the states and territories on Commonwealth grants and subsidies has also been associated with a loss of state and territory government autonomy over their budget priorities. The Commonwealth has exploited its constitutional power under Section 96 to extend its policy reach into areas traditionally within the legislative and administrative responsibility of the states, such as education, health and disability services, by providing financial assistance on terms that require states and territories to contribute additional funds and comply with prescriptive administrative or policy requirements.

With the implementation of ANTS, the Commonwealth has increasingly seen distributions to the states and territories from the GST revenue pool as merely another means by which it can obtain leverage over the states' and territories' spending and revenue raising priorities. An example of this can be seen in recent statements from the Federal Treasurer indicating that the Commonwealth will make the receipt of GST revenue conditional upon state and territory compliance with the Commonwealth's desire that certain state taxes, particularly stamp duty on business transactions, be abolished.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

2 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon