The homeowner does not get any deductions, but neither do they pay tax on the ‘imputed’ rent to themselves. This is a huge benefit, particularly for top-bracket taxpayers in large houses, and it is tax-free.

This is not the only area where the government seems confused.

While looking at upping the tax on mum and dad investors, they have halved the tax on foreign Managed Investment Trusts (MITs) to encourage them to provide build-to-rent (BTR) accommodation.

Advertisement

While mum and dad investors could end up paying capital gains at a rate approaching 47 per cent over time, properly structured MITs will face a tax rate of only 15 per cent.

Fiddling with capital gains will not only affect housing. It will also affect shares and superannuation, putting retirees and savers in the gun.

This is not just about profits foregone. Share portfolios are actively adjusted to manage risk. If the CGT discount goes, it becomes 50 per cent more expensive to manage that risk, and it will take longer for a retirement nest egg to grow to a level that can support someone in old age.

Or perhaps the saver falls short of self-sufficiency and becomes a pensioner, clawing some of the government’s capital gains tax back through social welfare.

Then there is the effect on entrepreneurs. It is fair to say the entrepreneur is not really interested in the income from an idea, but the potential capital payoff. So too are the investors every entrepreneur needs to turn an idea into a potential unicorn.

This becomes even more true the earlier the stage of investment. If you increase CGT by around 50 per cent you have just increased the cost of capital and the hurdle rate and made other jurisdictions more attractive.

Advertisement

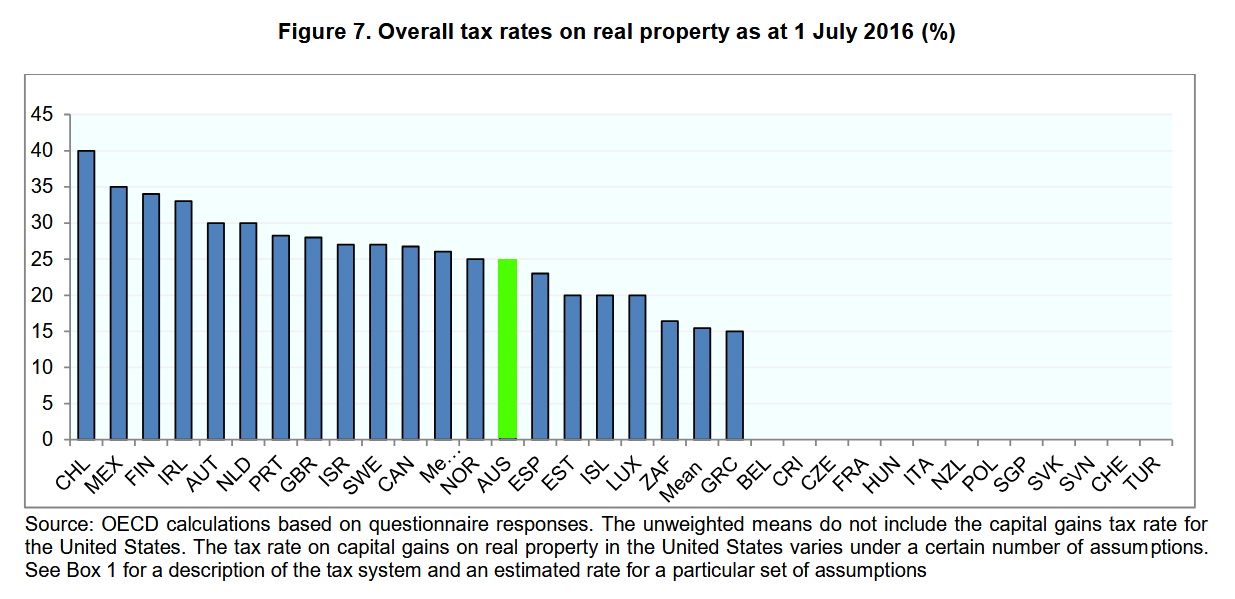

It is not as though Australia’s CGT rate is particularly low. The OECD puts us 13th highest for CGT among the 33 countries they measure. This is above average, and there are 13 countries on that list that do not charge CGT at all. Those 13 include New Zealand, France, Singapore, and Poland.

Source: OECD Taxation Working Papers No. 34 Statutory tax rates on dividends, interest and capital gains: The debt equity bias at the personal level. https://www.oecd.org/content/dam/oecd/en/publications/reports/2018/02/statutory-tax-rates-on-dividends-interest-and-capital-gains_1746a468/1aa2825f-en.pdf

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

2 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon