Monetaryand economic management are inextricably a part of the larger problem of income distribution in the modern economy. JK Galbraith Money whence it came, where it went, p 322

I Introduction, the US debate

The election of Donald Trump has thrown contemporary economic commentary into overdrive. It has also exposed the limitations of contemporary economic knowledge and comment. Supply side free traders are incensed that Trump proposes to rebuild the American industrial sector and provide jobs for the long term unemployed and raise incomes for the US labour force. Committed supply siders argue that industry protection will exacerbate inflation and erode prosperity not only for the US, but for the wider world of advanced economies. Trumps election appears to have destroyed the historical base of both the Republican and Democratic Parties. Consequently, he appears to have become anointed as the J.M. Keynes of the twenty first century.

A more sensible analysis suggests that Trump has been politically astute enough to tap into the political discontent across the US rust belt and low-income groups exposed by Covid for everyone to see. The Covid experience appears to have generated a mass rejection of the 1980's Reaganomics supply side economics that has driven domestic agendas of both major US political parties. The progressive social agendas of the left of centre democrats did not impress the masses experiencing unemployment, low incomes, and increasing poverty.

Advertisement

Free-market advocates ignore the concept of internal and external balance of an economy. Internal balance is achieved when an economy operates at full employment. External balance is measured by the balance of payments position. The current account needs to be in balance. For the US, exports comprise 10.89% of GDP whilst imports are 15.59% of GDP. In other words, whilst the US has a trade ratio of 27% of GDP, it has a negative current account imbalance equal to -4.7% of GDP. Given the rust belt and social dislocation in the US, the rejection of both major political parties continued support of the economics of the 1980's becomes understandable

The difficulty for Trump is that he is talking about erecting a tariff wall around the US to rebuild the US industrial base to provide employment and improve domestic income distribution. What he proposes is Keynesian demand management economics. Meanwhile he plans to lower domestic taxes and deregulate the economy. Domestically that continues Reaganomics supply side economics. This clash of economic philosophy appears beyond media and political commentators; but a clash of economic philosophy lies at the centre of Trumps agenda.

II The Australian economy

Compare Australia's situation with the US. In June 2024, Australian exports equalled 23.9% of GDP whilst imports equalled 22%. To free traders, this will be a commendable achievement; but the reality is that Australia's current account balance was -1.6% of GDP. This BOP deficit is defined as the net income deficit which is the difference between income inflow from Australian foreign investment overseas and foreign income outflow from overseas investment in Australia. In other words, Australia's has an external imbalance or net income out-flow of -1.6% of GDP. This means that the first 1.6% of Australian economic growth is earmarked to meet the imbalance of our external account. In reality, the current account imbalance is met by continued overseas borrowing which is documented on the financial account.

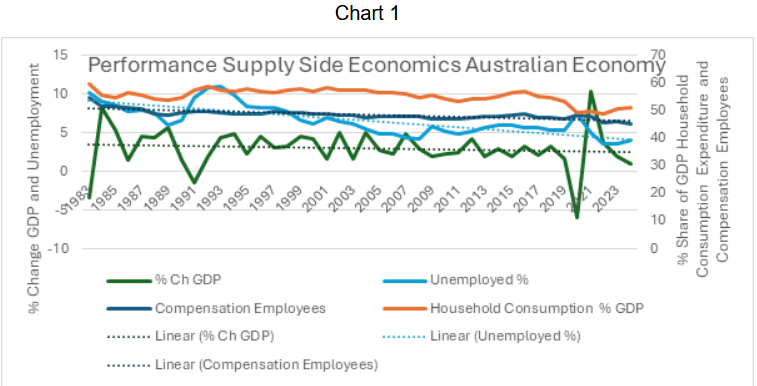

The version of supply side economics adopted in Australia by all major political parties was Thatcherism. Chart 1 below identifies the performance of the Australian economy post 1983 when the move to supply side economics began.

Compiled for RBA Statistical tables online

Advertisement

Chart 1 contains some disturbing outcomes that don't seem to interest our media and political experts. The trend line through GDP identifies long-term declining economic performance under supply side economics. The Covid impact is clearly identifiable over 2020-21. The strange outcome is the unemployment trend curve which depicts long-term decline despite declining economic performance: Compensation of Employees, and Household Consumption are two major contributors to economic performance; but they do not support falling unemployment.

The failure of major political parties, media commentators, and academia to discuss the sharp decline in Household Consumption expenditure post 2015 reflects poorly upon prevailing economic commentary in Australia. Household Consumption has fallen from 59.7% of GDP in 1983 to 51 % in 2024. From 2016, Household consumption Expenditure collapses from 56.8% of GDP to 49.6% before rising slightly to 51% in 2024.

The importance of consumption expenditure to economic performance can be understood from the national income equation:

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

6 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon