Y= C+ I+ G+ (X-M)

Y= National Income

C == Consumption expenditure

Advertisement

G = Government

(X-M) = Net exports

The fall in consumption from 59.7% of GDP in 1983 to 51% represents a redistribution of national income from consumption to other sectors of the economy represented in the national income equation. Our informed commentators appear blissfully unaware of the sharp decline in Household Consumption from 56.8% of GDP in 2016 to 48.7% in 2022. Post Covid there has been some recovery in Household Consumption to 51% in 2024. No doubt this explains government household support programs which are consistent with underconsumption theory from pre 1920's.

Meanwhile Compensation of Employees falls from 54.9% of GDP in 1983 to 45% in 2024. The contraction in compensation of Employees would explain the decline in household consumption expenditure as a percentage of GDP. The contraction of compensation of employees will be directly related to income distribution resulting from industrial policy, and net imports post 1983.

Compiled from RBA Statistical tables online

Advertisement

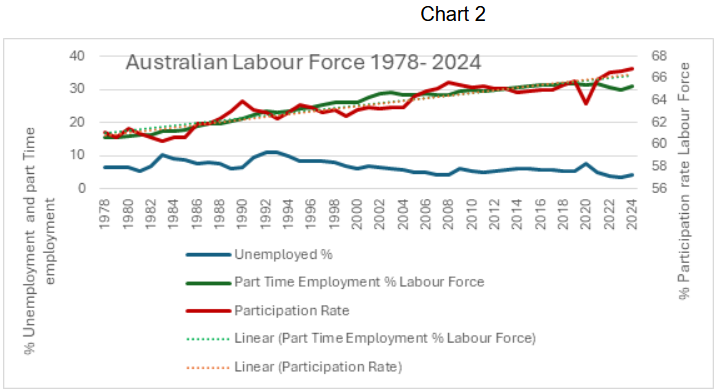

Chart 2 provides an insight into the impact of applied economic policy upon the labour force from 1978 to 2024. The interesting phenomenon is that the Participation Rate and Part Time Employment curves share a common trend line. Moreover, from 1982 onwards declining unemployment appears to have been achieved by restructuring the labour force between full time and part time employment. As part time employment includes low-income employment, the rise in part time employment provides a reasonable explanation of the declining share of wages percentage in GDP. It also raises questions over employment and unemployment statistics measured by statistical sampling.

III Monetary & exchange rate policy

Policy framework was influenced by the academic literature, but the academic debate on monetary policy has not run parallel with problems faced by practitioners.Stephen Grenville RBA Annual Conference, 1997

The collapse of post War Keynesian economics and the inflation of the early 1970's, fostered a move to monetarism pursuing monetary targets. Monetary targets were first implemented in Australia in 1976 under the Fraser Administration. Monetary targeting finally broke down in 1985 when it was abandoned by the Hawke Government. However, some eight advanced economies adopted what Stephen Grenville[i] identifies in his 1997 RBA Paper as pragmatic monetarism.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

6 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon