Monetaryand economic management are inextricably a part of the larger problem of income distribution in the modern economy. JK Galbraith Money whence it came, where it went, p 322

I Introduction, the US debate

The election of Donald Trump has thrown contemporary economic commentary into overdrive. It has also exposed the limitations of contemporary economic knowledge and comment. Supply side free traders are incensed that Trump proposes to rebuild the American industrial sector and provide jobs for the long term unemployed and raise incomes for the US labour force. Committed supply siders argue that industry protection will exacerbate inflation and erode prosperity not only for the US, but for the wider world of advanced economies. Trumps election appears to have destroyed the historical base of both the Republican and Democratic Parties. Consequently, he appears to have become anointed as the J.M. Keynes of the twenty first century.

A more sensible analysis suggests that Trump has been politically astute enough to tap into the political discontent across the US rust belt and low-income groups exposed by Covid for everyone to see. The Covid experience appears to have generated a mass rejection of the 1980's Reaganomics supply side economics that has driven domestic agendas of both major US political parties. The progressive social agendas of the left of centre democrats did not impress the masses experiencing unemployment, low incomes, and increasing poverty.

Advertisement

Free-market advocates ignore the concept of internal and external balance of an economy. Internal balance is achieved when an economy operates at full employment. External balance is measured by the balance of payments position. The current account needs to be in balance. For the US, exports comprise 10.89% of GDP whilst imports are 15.59% of GDP. In other words, whilst the US has a trade ratio of 27% of GDP, it has a negative current account imbalance equal to -4.7% of GDP. Given the rust belt and social dislocation in the US, the rejection of both major political parties continued support of the economics of the 1980's becomes understandable

The difficulty for Trump is that he is talking about erecting a tariff wall around the US to rebuild the US industrial base to provide employment and improve domestic income distribution. What he proposes is Keynesian demand management economics. Meanwhile he plans to lower domestic taxes and deregulate the economy. Domestically that continues Reaganomics supply side economics. This clash of economic philosophy appears beyond media and political commentators; but a clash of economic philosophy lies at the centre of Trumps agenda.

II The Australian economy

Compare Australia's situation with the US. In June 2024, Australian exports equalled 23.9% of GDP whilst imports equalled 22%. To free traders, this will be a commendable achievement; but the reality is that Australia's current account balance was -1.6% of GDP. This BOP deficit is defined as the net income deficit which is the difference between income inflow from Australian foreign investment overseas and foreign income outflow from overseas investment in Australia. In other words, Australia's has an external imbalance or net income out-flow of -1.6% of GDP. This means that the first 1.6% of Australian economic growth is earmarked to meet the imbalance of our external account. In reality, the current account imbalance is met by continued overseas borrowing which is documented on the financial account.

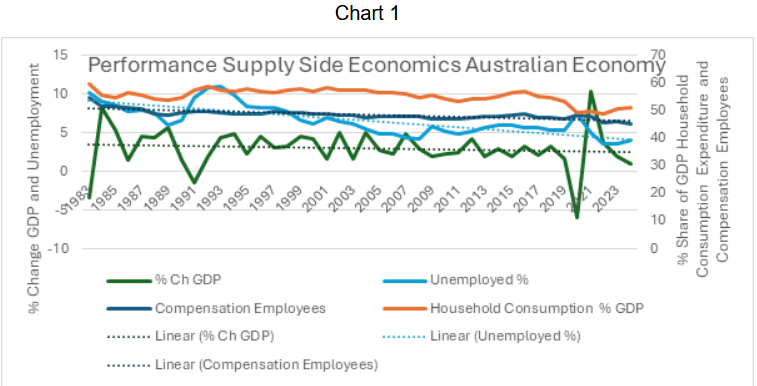

The version of supply side economics adopted in Australia by all major political parties was Thatcherism. Chart 1 below identifies the performance of the Australian economy post 1983 when the move to supply side economics began.

Compiled for RBA Statistical tables online

Advertisement

Chart 1 contains some disturbing outcomes that don't seem to interest our media and political experts. The trend line through GDP identifies long-term declining economic performance under supply side economics. The Covid impact is clearly identifiable over 2020-21. The strange outcome is the unemployment trend curve which depicts long-term decline despite declining economic performance: Compensation of Employees, and Household Consumption are two major contributors to economic performance; but they do not support falling unemployment.

The failure of major political parties, media commentators, and academia to discuss the sharp decline in Household Consumption expenditure post 2015 reflects poorly upon prevailing economic commentary in Australia. Household Consumption has fallen from 59.7% of GDP in 1983 to 51 % in 2024. From 2016, Household consumption Expenditure collapses from 56.8% of GDP to 49.6% before rising slightly to 51% in 2024.

The importance of consumption expenditure to economic performance can be understood from the national income equation:

Y= C+ I+ G+ (X-M)

Y= National Income

C == Consumption expenditure

G = Government

(X-M) = Net exports

The fall in consumption from 59.7% of GDP in 1983 to 51% represents a redistribution of national income from consumption to other sectors of the economy represented in the national income equation. Our informed commentators appear blissfully unaware of the sharp decline in Household Consumption from 56.8% of GDP in 2016 to 48.7% in 2022. Post Covid there has been some recovery in Household Consumption to 51% in 2024. No doubt this explains government household support programs which are consistent with underconsumption theory from pre 1920's.

Meanwhile Compensation of Employees falls from 54.9% of GDP in 1983 to 45% in 2024. The contraction in compensation of Employees would explain the decline in household consumption expenditure as a percentage of GDP. The contraction of compensation of employees will be directly related to income distribution resulting from industrial policy, and net imports post 1983.

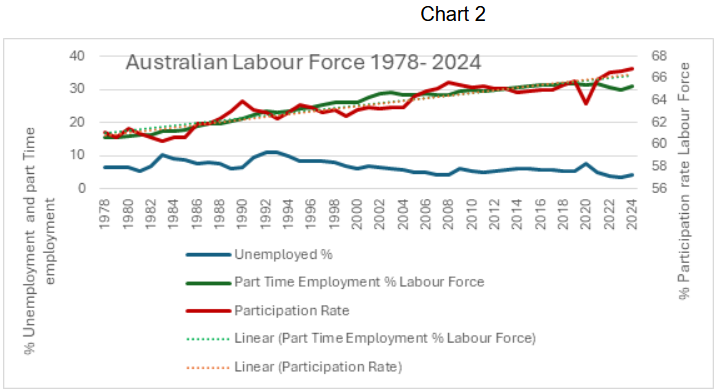

Compiled from RBA Statistical tables online

Chart 2 provides an insight into the impact of applied economic policy upon the labour force from 1978 to 2024. The interesting phenomenon is that the Participation Rate and Part Time Employment curves share a common trend line. Moreover, from 1982 onwards declining unemployment appears to have been achieved by restructuring the labour force between full time and part time employment. As part time employment includes low-income employment, the rise in part time employment provides a reasonable explanation of the declining share of wages percentage in GDP. It also raises questions over employment and unemployment statistics measured by statistical sampling.

III Monetary & exchange rate policy

Policy framework was influenced by the academic literature, but the academic debate on monetary policy has not run parallel with problems faced by practitioners.Stephen Grenville RBA Annual Conference, 1997

The collapse of post War Keynesian economics and the inflation of the early 1970's, fostered a move to monetarism pursuing monetary targets. Monetary targets were first implemented in Australia in 1976 under the Fraser Administration. Monetary targeting finally broke down in 1985 when it was abandoned by the Hawke Government. However, some eight advanced economies adopted what Stephen Grenville[i] identifies in his 1997 RBA Paper as pragmatic monetarism.

In 1958, Bill Phillips identified a direct link between wage movements and unemployment. In 1960, two eminent American economists, Paul Samuelson and Robert Solow, argued that when US unemployment was high, inflation was low and vice versa[ii]. Their research had identified that in the USA, when unemployment was at 5%-6% inflation would be zero. Further, if unemployment was 3%, then inflation would be within the range of 4%-5%. Consequently, the Phillips Curve evidence suggested that by manipulating policy, governments could choose the relationship between inflation and unemployment. Pragmatic monetarism followed.

Over the 1970's, the established interpretation of the Phillips Curve broke down across advanced western economies[iii]. The breakdown of the Phillips Curve encouraged Friedman and others to assert the superiority of micro level theoretical competitive equilibrium theory over established macroeconomics. They argued that the breakdown of the Phillips Curve discredited Keynesian economics and the belief that governments could manipulate tax rates and spending to control the level of employment.

Free market economist argued further that governments could no longer manipulate policy to ensure full employment. As the Phillips Curve relationship had broken down, attempts to vary output through expenditure and tax rates would result in inflation. The free-market school offered a different interpretation of theory. Free market economics combined the Philips Curve with rational expectations to re-establish economic orthodox theory, and the micro foundations of macroeconomics

The rational expectations Phillips Curve argues that there is a unique level of unemployment at which unemployment and inflation will neither accelerate nor decelerate. This level of unemployment is known as the Non-Accelerating Inflationary Rate of Unemployment or NIARU. This theory passed quickly from theory to the world of politics.[iv]

As NAIRU is a supply side phenomenon, it cannot be affected by government policies designed to alter the level of demand in the economy. Consequently, reform of supply side phenomenon in the economy becomes the focus of economic policy. The concept has become very influential across academic circles, financial journalists, and policy makers. However, it is the underlying assumption of rational expectations that holds the key to its relevance in the real world.

Rational expectations asserts that when economic agents make decisions, they learn from past experiences. Whilst some mistakes will be made, correct expectations of the future will dominate decision making.

The importance of the underlying rational expectations assumption cannot be overstated. It is the dominant assumption used in business cycle and finance theory. Moreover, it is the cornerstone of the efficient market hypothesis.

IV Monetary policy in Australia

On election to Government in 1983, the Labor Government renounced monetarism in its pragmatic form; and it was finally abandoned in 1985. Labor saw a wages and incomes policy as the principle means of achieving price stability. Consequently, some mix of a wages policy and monetary policy seemed the way forward. Targeting M3 was seen as an intermediate target rather than the prime instrument of monetary policy. Neither did the RBA see monetary targets as a realistic operational target. Price expectations were left to the Accord.

Over the late 1980's, monetary policy underwent structural reform. Monetarist principles were incorporated into a new neoclassical synthesis which replaced the old neoclassical synthesis from the 1930's. By 1988, the Australian money supply was redefined from an exogenous variable to an endogenous variable. Monetary policy changed from demand management to supply management. By the early 1990's the RBA moved to employ the cash rate as the supply side policy instrument. Unofficial independence emerged for the RBA to pursue both external and internal balance.

The RBA adopted Inflation targeting in 1993. As rational expectations underwrote the inflation augmented Phillips Curve, NAIRU became the policy objective. The RBA decided that this level of unemployment should lie between 2% and 3% inflation. In other words, Marx's nineteenth century reserve army of unemployed returned to the economic agenda of the late 20th century.

In 1996, the RBA was granted official independence. Consequently, through monetary and exchange rate policy arms, both internal and external balance became the responsibility of an independent central bank. This effectively removed administration of internal and external balance from voter assessment at election time.

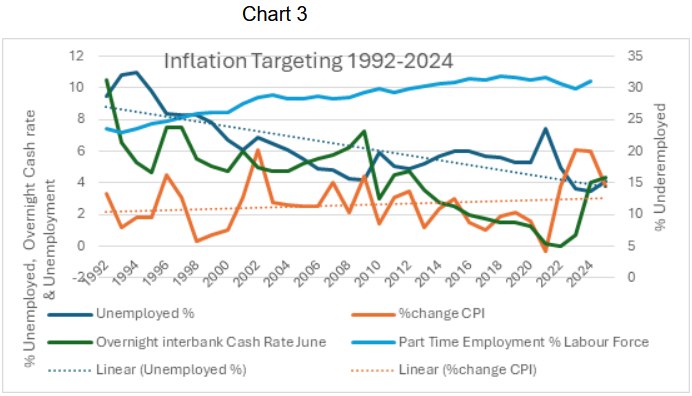

Chart 3 depicts graphically, applied monetary policy from 1993 to 2024

Compiled from RBA Statistical Tables, online

From around 2007, monetary policy appears ineffectual

Long-term trend lines through unemployment and CPI curves question the assertion of NAIRU, and the inflation augmented Phillips curve

Whilst managing the "reserve army of unemployed" part time employment has boomed.

The growth in part time employment helps explain the decline in contributions to GDP of Household Consumption Expenditure, and Compensation of Employees

V Conclusions

- Political ideological claims of poor labour productivity and excessive government expenditure are the cause of Australia's economic malaise do not withstand analysis.

- Maldistribution of income must be addressed

- A review of statistical methodology underwriting Australian economic policy would seem important for development of sound economic debate.

- There is an urgent need for an informed debate over applied economic philosophy.

- All policy arms must return to Government control and allow voters the opportunity to vote on prevailing economic management

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon