In the Statement of Monetary Policy, released on 7 May, the RBA provided a detailed outlook on where it expects inflation, unemployment and interestingly, the cash rate, to be.

The RBA expects that core inflation, shown as the "trimmed mean", should fall from 4.2% in December 2023 to 3.4% in December 2024, then to 3.1% in June 2025, 2.8% in December 2025, and approach its long-term target for inflation by reaching 2.6% in June 2026.

At the same time, the RBA expects that unemployment will rise from 3.9% in December 2023 to 4.2% in December 2024, and then 4.3% in December 2025. Interestingly, it expects this level of 4.3% to be the peak. Unemployment, it thinks, will remain at 4.3% in December 2025 and June 2026. The RBA believes that not only is this level of unemployment of 4.3% enough to bring down inflation, but the data also suggests that it might be enough to bring down the cash rate. The RBA's outlook shows the cash rate will stay where it is near 4.4% in December 2024, then decline to 4.2% in June 2025, 3.9% in December 2025, and finally reach 3.8% in June 2026. This suggests a cut of seventy-five basis points between December 2024 and June 2026.

Advertisement

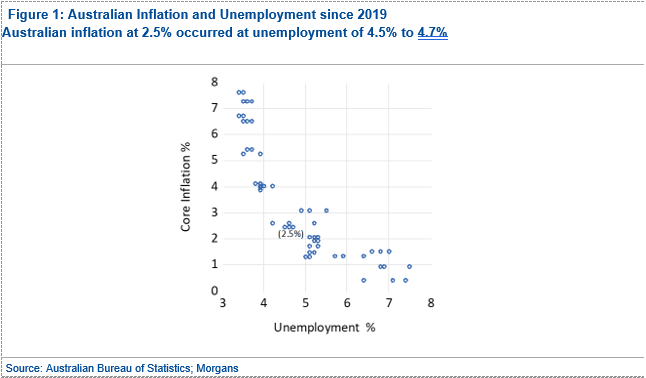

We think that this reduction in inflation will be difficult to achieve based on the historical relationship between Australian unemployment and inflation. In Figure 1 we show the relationship between Australian core CPI and unemployment for the period since 2019. Readers with an economic background will immediately recognise this as a short-term Phillips Curve.

We can see from Figure 1 the trade-off between core inflation and unemployment since 2019. Interestingly, we find that the RBA inflation target of 2.5% was achieved for a brief 3-month period in July, August and September 2021. Unemployment in each of these months was 4.5%, 4.7% and 4.6% respectively. The average of these numbers is 4.6%. We think this level of 4.6% is the lowest level that unemployment must rise to if the RBA is to achieve its inflation target of 2.5%.

The longer-term data suggests an even higher number. Economists speak of this data as describing a long-term Phillip Curve. To do this, we look at the data, beginning in January 2005. Since January 2005, the median unemployment level in Australia is 5.2% and the median core CPI level has been 2.4%. This aligns with the RBA inflation target of 2.5%. This long-term Phillips Curve implies that to reach the RBA's inflation target of 2.5%, the unemployment level must rise to as much as 5.2%. We summarise both the long-term and short-term relationship by stating that the data suggests Australian unemployment must rise to a level between 4.6% and 5.2% for the RBA to be certain of achieving its inflation target of 2.5%. Both of these figures are higher than the peak level of unemployment shown in the RBA Statement of Monetary Policy of 4.3%.

Conclusion

The data suggests that based on the relationship between unemployment and core inflation in Australia since 2005, both the long and short-term data suggests that unemployment is likely to exceed a level of 4.3% before inflation falls to the RBA target of 2.5%.

Advertisement

This implies that the RBA is likely to be stuck with the cash rate at the current level of 4.35% for quite a while. We believe inflation will remain harder to beat than the RBA suggests. RBA rate cuts will have to wait for some time to come.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

In Hong Kong, research is issued and distributed by Morgans (Hong Kong) Limited, which is licensed and regulated by the Securities and Futures Commission. Hong Kong recipients of this information that have any matters arising relating to dealing in securities or provision of advice on securities, or any other matter arising from this information, should contact Morgans (Hong Kong) Limited at hkresearch@morgans.com.au

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon