In this issue, we look at the updated International Energy Agency (IEA) oil report for October 2023. We examine why current oil demand is stronger and we update our models to tell us what may happen in the future.

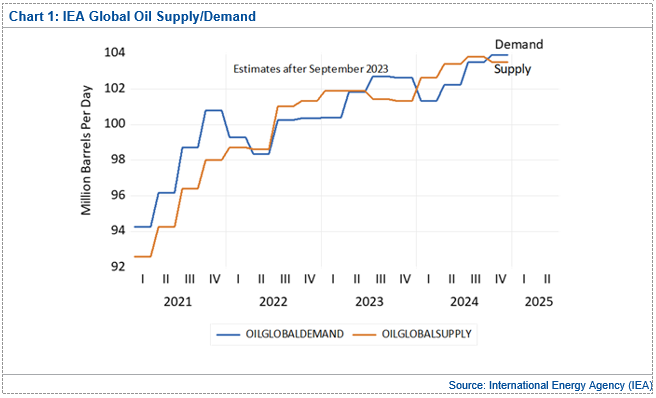

In Chart 1 below, we see the IEA estimate of global quarterly oil demand and global quarterly oil supply since the beginning of 2021.

Advertisement

What is most immediately evident is the demand recovery that was seen as the world reopened from the pandemic. In calendar 2021, global oil demand increased from 94.3 million barrels a day in the first quarter, to 100.8 million barrels a day in the fourth quarter. Supply raced to keep up but was always behind. Supply rose from 92.6 million barrels a day in the first quarter of 2021, to 98.6 million barrels a day in the fourth quarter. World demand exceeded world supply in every single quarter. As a result, stocks levels fell and prices rocketed.

It was this rapid recovery in demand which had already generated the condition for a rocketing oil price before Russian tanks crossed the border into Ukraine in early 2022. It was this recovery in demand as the result of reopening after the pandemic that generated high oil prices and not the war in Ukraine.

In 2022 demand fell and supply modestly rose. By Q2 2022, global demand had fallen to 98.4 million barrels a day and supply had risen slightly to 98.6 million barrels a day. By Q1 2023, global demand had risen to 100.4 million barrels a day. It had been stable near that level for the previous three quarters. The reason for the softness in demand was the renewed shutdown in China. Although demand stabilized, supply rose because of greater production in the US and Canada. By Q1 2023, global supply had risen to 101.9 million barrels a day. This was an excess supply of 1.5 million barrels a day. As result of this, stock levels rose and prices fell. The result was a low in oil prices in mid 2023.

That period of oversupply has now been followed by a period of tightness. Two things have happened. Firstly, the IEA October report tells us that there has been "buoyant demand growth in China, India and Brazil." (China was 77% of this increase). This had led to an increase in demand in Q3 2023 to 102.7 million barrels a day. The IEA expects this to stabilise at 102.6 million barrels a day in Q4 2023. At the same time, a reduction in output by OPEC Plus nations has stabilized supply at 101.4 million barrels a day in Q3 2023 and an expected 101.3 million barrels a day in Q4 2023. This means that a shortfall of 1.3 million barrels a day in Q3 2023 is followed by a shortfall of 1.3 million barrels a day in Q4 2023.

The IEA tells us that a result of this shortfall "global observed inventories tumbled by 63.9 million barrels in August 2023. They say that OECD industry stocks fell in August to a level 105.3 million barrels below the five-year average.

Advertisement

In Chart 2 above, we see our model of the Brent oil price based on quarterly data for Brent plus the quarterly estimates of the IEA contained in their oil report. Our model explains 71% of quarterly variation of the Brent oil price. Our model estimates for Brent, based on the excess supply in Q2 2023, suggested an equilibrium price in Q3 2023 of $US82.06 per barrel. This rises to $US99.44 per barrel in Q4 2023 and $US114.62 per barrel in Q1 2024. This then stabilizes at $US114.02 per barrel in Q2 2024, before falling to $US87.58 in Q3 2024. In short, the current period of tight supply looks like it is about to generate higher oil prices during the coming European winter. These prices decline as temperatures improve.

Conclusion

Our model of the Brent oil price, based on survey data, suggests that the $US price of Brent should rise to $US114 a barrel in early 2024. Europeans may find that winter warmth is again a costly expense as they move into the new year.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

In Hong Kong, research is issued and distributed by Morgans (Hong Kong) Limited, which is licensed and regulated by the Securities and Futures Commission. Hong Kong recipients of this information that have any matters arising relating to dealing in securities or provision of advice on securities, or any other matter arising from this information, should contact Morgans (Hong Kong) Limited at hkresearch@morgans.com.au

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

3 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon