The RBA released its Statement for Monetary Policy on 10 November 2023. Under the RBA new order of business, this statement has increased emphasis similar to the Summary of Economic Projections released every quarter by the Federal Reserve.

Special attention must therefore be paid to Table 5.1: Output Growth and Inflation forecasts. This shows the current forecasts compared to those three months ago.

We see that GDP growth for December 2023 is 0.5% higher than expected three months ago. CPI inflation for December 2023 is 0.25% higher than expected. By June 2024, it will be 0.5% higher than expected. Central bankers treat the short rate as a real rate - so higher inflation means a higher Australian cash rate. A prudent wager would be that the real cash rate should rise by a total of 0.5% over the two RBA meetings in November and December.

Advertisement

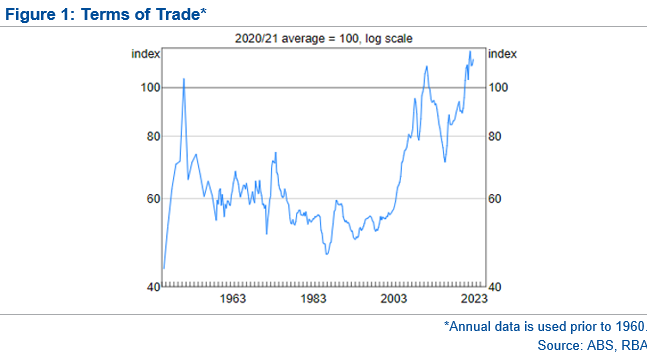

The economy is growing stronger than expected. A quick glance at the terms of trade drawn from the RBA chart book could tell us why. The Australian terms of trade, calculated by dividing export prices by import prices, are still higher than during the resource boom earlier this century. This is still providing enormous economic stimulus to the Australian economy. Truly, we remain the lucky country.

There is another issue towards the end of the document. This is in a section called Box B: "Has the Economic Outlook Evolved as Forecast a Year Ago?" We see that "Population growth has been stronger than anticipated, driven by a large increase in net overseas migration following the re-opening of the border."

They go on, "but the net effect on the unemployment rate and on aggregate inflation has been relatively small because the increase in population has added to both supply and demand in the economy." This statement is only true if we are talking about supply and demand in the labour market.

When we talk about total demand in the Australian economy, we must remember that once a permanent migrant worker with a full-time job qualifies for a housing mortgage, that worker adds many times their annual compensation to total demand.

We think the opportunity for further upside surprises to RBA on growth and inflation are excellent. Those surprises will be courtesy of "the lucky country."

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

In Hong Kong, research is issued and distributed by Morgans (Hong Kong) Limited, which is licensed and regulated by the Securities and Futures Commission. Hong Kong recipients of this information that have any matters arising relating to dealing in securities or provision of advice on securities, or any other matter arising from this information, should contact Morgans (Hong Kong) Limited at hkresearch@morgans.com.au.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

8 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon