In recent weeks, I have spent much time looking at the extremely difficult issues confronting European economies. Here we see real crisis. Here we see major economies facing the strife caused by major slumps in their terms of trade. Important resources are difficult to get. Their economies and their populations are faced by genuine hardship made worse by the approach of winter.

How different it is to look at the Australian economy painted by these budget papers. This is a rich and prosperous economy in the midst of a major commodities boom. This is an economy benefiting from a major rise in its terms of trade, precisely the reverse of the terms of trade slump suffered in Europe. The Treasurer's greatest hardship seems to be the problem of distributing the benefits of Australia's strong terms of trade.

Advertisement

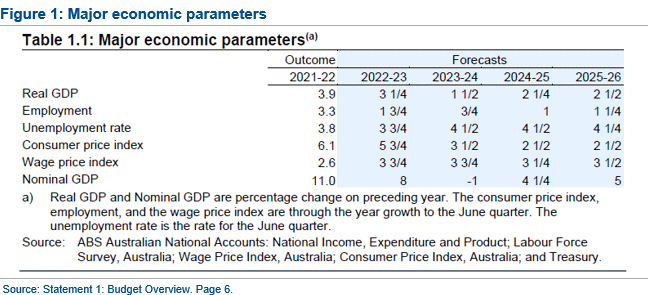

In Figure 1 above, we see the major economic parameters provided to us in Budget Paper No 1, page 6. Growth in the financial year just past was a very strong 3.9%. Growth in the financial year we are in now is 3.25%. Even when growth slows in 2023/2024, it is still a positive 1.5%. No recession here. Growth then recovers in 2024/2025 to 2.25% and again in 2025/2026 to 2.5%.

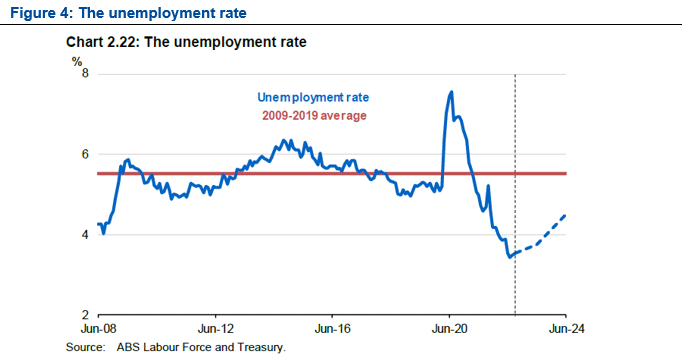

Unemployment does rise as we move towards 2023/2024 but it peaks at 4.5% in 2024/2025. Australian policy makers have been trying to get unemployment below 4.5% for most of the past two decades. It is hardly a problem if this is the peak level to which unemployment may now rise.

The CPI is a problem in Australia but not a problem of the scale that faces European economies. The CPI is about to peak at the end of calendar 2022 and then begin to decline. The budget papers suggest by mid 2023, CPI inflation will fall in Australia to 5.75%. It will fall to 3.5% a year later. By 2023/2024, inflation will be back safely in the RBA target range of 2-3%.

Inflation may be falling, but wage growth finally catches up with inflation in 2023/2024 and then sprints ahead faster than inflation over following years. This means wages are expected to rise in real terms. Living standards are expected to improve.

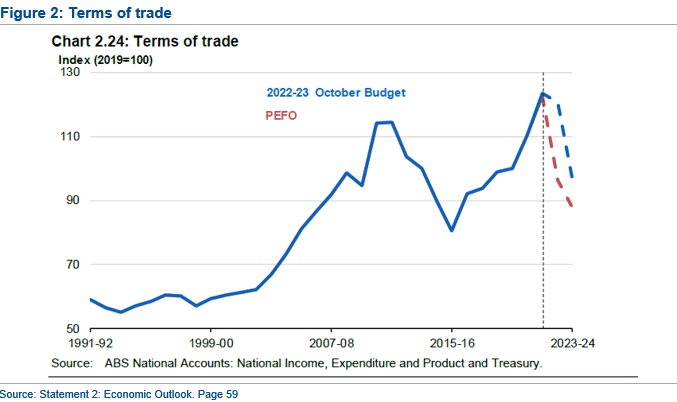

The miracle that drives this prosperity within the Australian economy is captured by the terms of trade. We see this in Figure 2, drawn from Statement 2, page 59. Australia is receiving much higher prices for what it sells compared to what it buys. The terms of trade, as it currently stands on this chart, is the highest that has been recorded in Australian economic history. We see that the budget papers suggest these prices will fall in the future. Budget papers are notoriously conservative about future prices. We should note that even if the terms of trade did fall as rapidly as the budget papers suggest, they would still be much higher than they were in 2015/2016 and very much higher than they were in the 1990s.

Advertisement

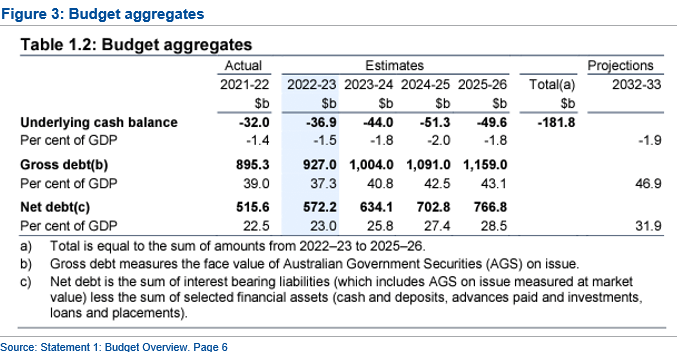

The beneficial circumstances that the Australian economy finds itself in are reflected in improvement in the budget balance. A budget deficit of $36.9 billion in 2022/2023 is only 1.5% of Australian GDP. Even as the outlook worsens in 2024/2025, the budget deficit only widens to 2% of GDP. For the same period, the US budget deficit looks like widening to near 4% of GDP. These are still very good numbers, and they are extremely good numbers in the situation of the expanded welfare programs contained in this budget.

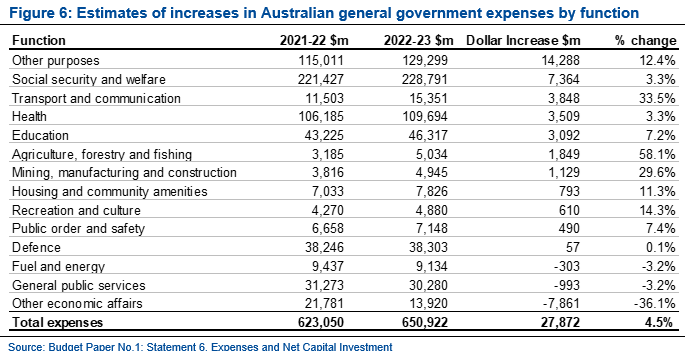

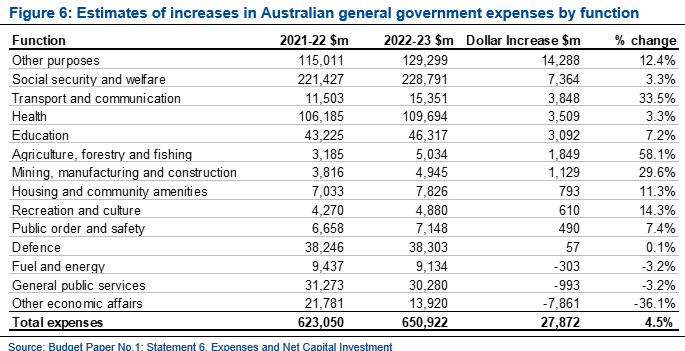

The areas of increases in spending are shown in Figure 6. This is drawn from Budget Paper No 1, Statement 6. The most interesting dollar increase is in transport and communication. This is an increase in spending of $3.848 billion. This represents an increase of 33.5%. This spending is primarily driven by "acting on climate change". The government provides $1.9 billion to the "Powering the Regions Fund". This provides dedicated support to energy transition of regional industries to net zero while harnessing the economic opportunities presented by decarbonisation.

In addition, the "Driving the Nation Fund" invests $500 million including the delivery of electric vehicle charging infrastructure, hydrogen highways for freight routes, and further investment in charging infrastructure. To make electric vehicles cheaper, there is $345 million devoted to an Electric Car Discount that will cut taxes by exempting eligible electric cars from fringe benefits tax and the 5% import tariff.

Even though unemployment rises over the next few years, it rises to levels which are far, far below the average levels of unemployment Australia has seen in the previous two decades.

The beneficial situation that Australia finds itself in, can also be seen in the budget outlays. These are shown in Figure 5. These are drawn from Budget Paper No 1, Statement 6.

Total outlays in the budget are $650.922 billion. Social security and welfare is the largest item with $228.8 billion or 35.1% of total spending.

Health spending is next at $109.694 billion or 16.9% of spending. Education spending comes next with $46.3 billion or 7.1% of total spending. Only then comes Defence with $38.303 billion or 5.9% of total spending.

What this Budget does

Australia is not a country in crisis. Australia is a rich and confident economy and its only suffering is the problem of distributing the benefits of an extremely healthy terms of trade. The government has responded to this happy position by providing cheaper childcare and more parent leave. They have tried to expand health care and make medicines cheaper. They have provided further support to aged care.

They are expanding places in TAFE and in universities. In addition to doing that, it is spending money on renewable energy.

To make sure they cover all their bases, they are providing more support to affordable housing.

Clearly this is an economy with plenty of resources.

Conclusion

There may be talk of hardship and difficulty. The major problem this budget faces however is the happy difficulty of distributing the benefits the economy and the government has received from the very high terms of trade and very high commodity prices that Australia is now receiving.

This provides this country with an unusual experience in a world where many countries are facing increasing difficulties and major hardship. We should be grateful that our problems are such little ones.

The beneficial outlook provided by the terms of trade has the result of maintaining unemployment at levels which are extremely low, in comparison to the previous two decades. We can see this in Figure 4 drawn from Budget Statement No 3, page 81.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon