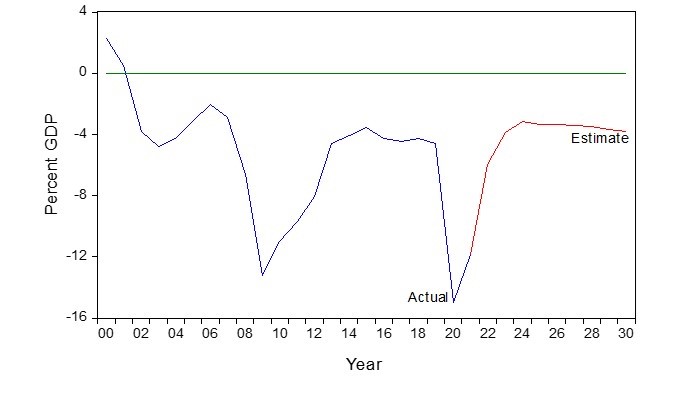

Last year in July, when the US decided to dramatically expand its US budget deficit to levels that were even larger than after the GFC, I forecast that by now we would have an enormous commodities boom and that the result of that would also be upward pressure on the Australian dollar.

Well, we certainly have an enormous commodities boom. The Aussie dollar did rally initially, up until the beginning of this year, and has come off a bit since then. However, what our US budget deficit model tells us is that we are going to see dramatically higher commodity prices still, for the next two to three years. That should put upward pressure on the Aussie dollar.

Figure 1: US Federal Budget Balance – 2020 to 2030

Advertisement

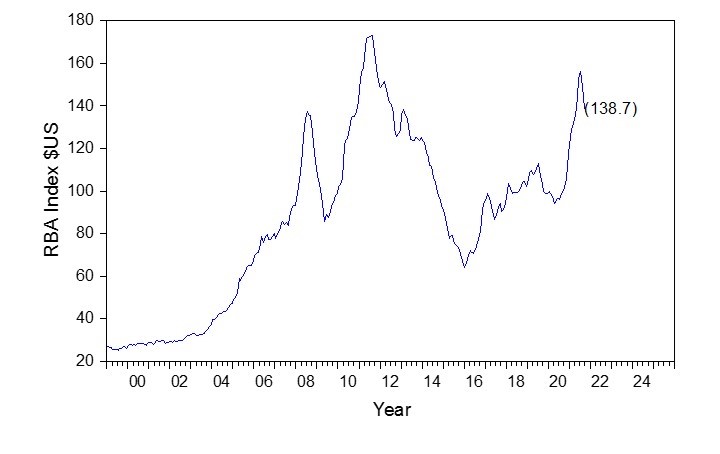

Perhaps the best way of looking at this and updating your view on this personally, is to look at the RBA website. There is a chart that is updated by the RBA at the beginning of every month. They show the RBA index of export commodity prices in SDR (the IMF currency basket exchange rate) terms. I believe that the rationale in showing the SDR terms is that it probably shows the terms of trade effect.

What we are trying to estimate is the effect on currency. For this, we prefer this index in $US terms. This is shown in Figure 2. What you can see is a dramatic increase in commodity prices over the last year to a level that is 38.7% higher, on average, than the level in 2019 and 2020. It is still not as high as the peak levels of the resources boom.

Figure 2: RBA Index of Commodity Prices in $US

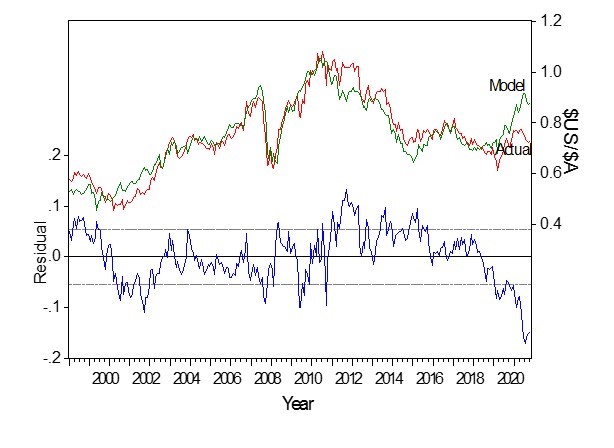

This isthe fundamental thing. We are stepping back to what is the conventional view of the Aussie dollar. It is a commodity model, and it's driven by commodity prices and relative interest rates. The argument could be, for example, one of the reasons the Aussie dollar isn't strong is because the RBA is entering into the market for short and long-term bonds, and interest rates are lower than they would otherwise be.

Advertisement

Of course, that is absolutely true and that is why we include the current levels of interest rates, both US and Australian,into our model. What you can see,is that we can build a model based on the Aussie dollar moving up and down with those export commodity prices and also Australian and US interest rates. That model then explains 87% of the monthly variation. This model is shown in Figure 3.

Figure 3: Model of $US/$A

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon