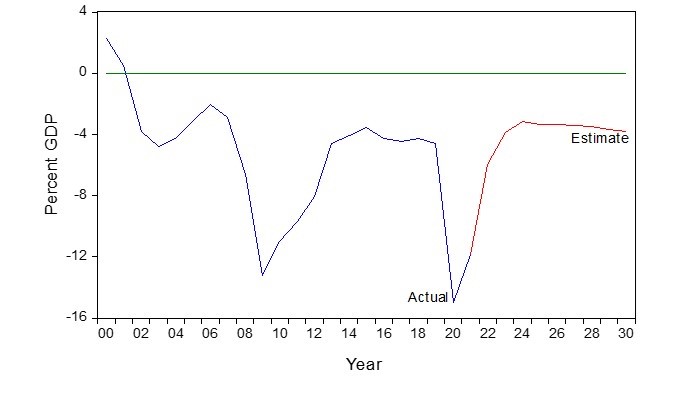

Last year in July, when the US decided to dramatically expand its US budget deficit to levels that were even larger than after the GFC, I forecast that by now we would have an enormous commodities boom and that the result of that would also be upward pressure on the Australian dollar.

Well, we certainly have an enormous commodities boom. The Aussie dollar did rally initially, up until the beginning of this year, and has come off a bit since then. However, what our US budget deficit model tells us is that we are going to see dramatically higher commodity prices still, for the next two to three years. That should put upward pressure on the Aussie dollar.

Figure 1: US Federal Budget Balance – 2020 to 2030

Advertisement

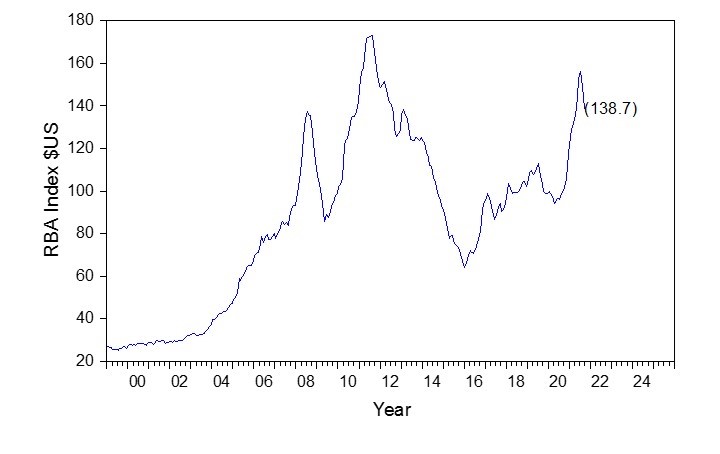

Perhaps the best way of looking at this and updating your view on this personally, is to look at the RBA website. There is a chart that is updated by the RBA at the beginning of every month. They show the RBA index of export commodity prices in SDR (the IMF currency basket exchange rate) terms. I believe that the rationale in showing the SDR terms is that it probably shows the terms of trade effect.

What we are trying to estimate is the effect on currency. For this, we prefer this index in $US terms. This is shown in Figure 2. What you can see is a dramatic increase in commodity prices over the last year to a level that is 38.7% higher, on average, than the level in 2019 and 2020. It is still not as high as the peak levels of the resources boom.

Figure 2: RBA Index of Commodity Prices in $US

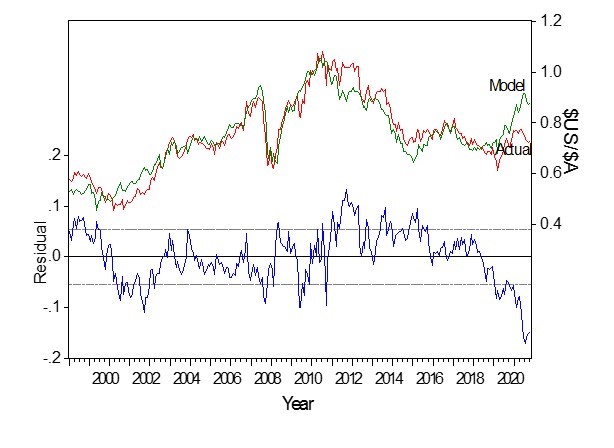

This isthe fundamental thing. We are stepping back to what is the conventional view of the Aussie dollar. It is a commodity model, and it's driven by commodity prices and relative interest rates. The argument could be, for example, one of the reasons the Aussie dollar isn't strong is because the RBA is entering into the market for short and long-term bonds, and interest rates are lower than they would otherwise be.

Advertisement

Of course, that is absolutely true and that is why we include the current levels of interest rates, both US and Australian,into our model. What you can see,is that we can build a model based on the Aussie dollar moving up and down with those export commodity prices and also Australian and US interest rates. That model then explains 87% of the monthly variation. This model is shown in Figure 3.

Figure 3: Model of $US/$A

It explains why the Aussie dollar was strong in the period immediately prior to the financial crisis. Commodity prices were stronger than you would expect from a US budget deficit-only model. What it says now,is that the Aussie dollar should be trending to a significantly higher price than it currently is.

Still, most investors are not really interested in trading the Aussie dollar. What they are trying to do is ensure against the risk of what might happen if the Australian dollar moves one way or another. Should they hedge various unit trusts or exchange traded trusts and exchange traded funds which they are holding.

Therefore, what we do, is calculate this not just in terms of price but also in terms of risk. The current fair value based on where commodity prices is a touch over US87c and that's US15c higher than where the Aussie dollar is currently trading. That's 2.8 standard errors away from fair value. The probability of a 2.8 standard event is that there are about 3 chances in 1,000 that the Aussie Dollar will go down from here. This suggests there's an overwhelming risk the Australian dollar will move higher.

The problem we face is that no two commodity cycles have been the same and the current cycle is dominated by Covid and how governments are responding. This is further complicated by the fact the Aussie dollar typically trades as part of a basket of non-US dollar assets, and the largest non-US dollar asset is the Euro. The Aussie dollar trades internationally not so much as the Aussie dollar itself but part of a group of non-US dollar assets. The dominant way of trading those is in terms of index funds of non-US dollar assets. The largest component of those index funds of non-US dollar assets is the Euro.

The Euro tends to lead other non-US dollar exchange rates. It tends to be the bellwether that leads index funds of non-US dollar assets. This is followed by things like the Yen, and the Pound Sterling, and further along, there are currencies like the Australian dollar. Following us, there are currencies like the South African rand and the New Zealand dollar. The biggest currencies in the index move first and the medium ones move next and the smallest currencies move last.

What we've had is a very slow response from the Euro in this cycle, as opposed to the previous cycle. The best explanation I can find of that is the vaccination lag for Covid between Europe and the United States. That is, in the United States, Covid vaccinations started on the 14th of December 2020 but it was not until the end of the week of the 28th of July 2021, that the European Union reached the same level of vaccinations achieved in the United States. The US, despite being the world's largest economy, is a net importer of capital, an importer of savings and the biggest source of savings is the European area. There is a great deal of excess savings ie a current account surplus in the Euro area, as opposed to current account deficit for the US.

For the Europeans, it has been better to continue to invest in the United States, than keep the money and invest in Europe and partly because of their vaccination lag. Pretty much from any time now, you should see more money being kept within the Euro area and invested domestically within the European economy. That should generate a surge in the Euro relative to the US dollar. However, now Europe has caught the US with its vaccination rollout. We expect the European economy to pick up and as a consequence return more of Europe's savings for investment in Europe.

When that happens that will lead the index of non-US dollar assets including the Aussie dollar in a northward direction. That is the best description I can provide of what's happening in terms of fundamentals and what's happening in markets.

A likely trigger of the beginning of the process is the announcement of a very strong growth number for the Euro Area for the September quarter. The next Euro Area GDP number will be announced on 30 October. This GDP announcement could be the trigger that lifts the Euro against the US dollar. We will have to wait and see.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon