Today I am going to look at the outlook for the US economy for the next few years. Let us start with US inflation. You must remember that a year ago the US economy was going into lockup. At that time people stopped driving their cars. As they stopped driving their cars, there was a collapse in the demand for petroleum. The oil prices went into negative territory for the first time on record. Since that time, you’ve seen a recovery of the automotive sector and you’ve also seen a recovery of the aircraft sector. People are traveling again.

Most of the price increases in the last year are in the petroleum sector and in the energy sector. The ones that are outside that group were still automotive. There are things like car hire or the price of used cars. All these prices are accelerating at a very rapid pace. All of this was a result of the recovery of travel. People were driving to work, and people were driving to other places around the US. People were flying around the US. That is what is driving the increase in US inflation. We note that the US monthly CPI rose by 0.6% in May, down from the 0.8% rise in April. That sort of recovery can be very intense for a short period of time, but it soon tapers off. That is the pattern we see in the US economy when we look at our output forecast for this year, next year, and a few years after that.

The Federal Reserve already expects that GDP growth in the US economy this year will be 7.0%. In the first quarter, growth was 6.4% annualised. Usually that’s revised upwards. We expect it to be revised upwards to around 6.7%.

Advertisement

In the second quarter, the Atlanta Fed tells us the US economy is growing at a 10.3% annual rate. This means it will grow by about 2.6% for the quarter. That is incredibly powerful. When we look at what is driving that very, very rapid growth, it is the same thing that drove prices. People are getting into their cars again and driving! Aircraft are now flying around the United States. There is a dramatic increase not just in traveling expenditure. The demand for aircraft for example is rebooting itself again in the US economy.

For this year we now expect growth in the US economy of 7.0%. The biggest surge of that is increase in aircraft manufacture which should grow by about 60% this year, drops away to 40% next year (still huge numbers), but then 10% the year after that, and 2% the year after that. The manufacture of transportation equipment, car manufacturing, demand for new motor vehicles and trucks up 20% this year, 10% next year, and 10 % the year after that, but nothing the year after that. Again, it’s the recovery of domestic transportation within the US economy.

As a result of this you get a big surge in the Mining and Petroleum sector (which is basically the petroleum sector). That grows by about 20% this year and the next year in the US economy and nothing the year after that and the year after that. What you’ve got is a total growth outlook of the US economy of 7.0% this year, we think 4.7% next year, and then it drops back to 2% the year after that and the year after that. However, all this growth is in the dramatic recovery from the shut down last year, and a bit more driven by the enormous increase in domestic demand.

In the short term, a rapid recovery in growth drives a short-term surge in producer prices. This year it looks like year on year growth increased producer prices about 6%. This is big and bigger than anything for the last ten years. Then this acceleration in producer prices drops away. This inflation of producer prices drops away to 2% next year.

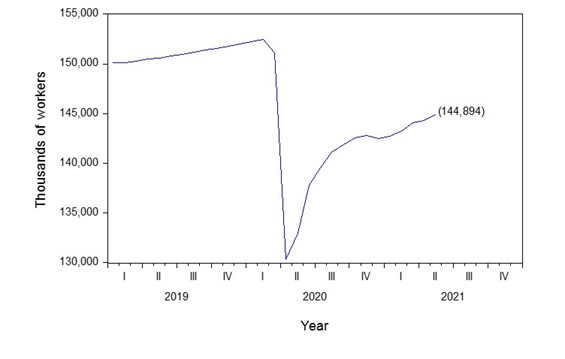

US unemployment is still high and it takes a while to get down. By the time you get to 2023 you get very low US unemployment of 3.5%. In the US economy, this is very much full employment, so you start to get wages growth. That is when the Fed probably starts to put up interest rates again. This is 2023-2024 when this happens. Not this year and it’s not next year.

Figure 1: Us Payroll Employment

Advertisement

As GDP growth slows down, producer price growth does as well. Still, there is very strong GDP growth in the US, 7.0% this year and 4.7% next year. This is the strongest growth for decades. That generates very powerful growth in the Australian economy because we usually grow in line with the US, or maybe just a bit behind. This year and next year will give us a very strong outlook, both in the US economy and indeed flow on effects in the Australian economy. The good times will roll for the next couple of years.

What we can see is this is a very powerful period for the US economy both this year and next year and hence will be a very powerful period for the Australian economy this year and next year. Still, inflation forecasts in the next two to three years are still much lower than the media would have you believe.

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

3 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon