At the end of World War II, Ben Chifley saw a vision of a powerful Australian economy recovering from years of pain. His vision was enacted first by his government and then for many years by the governments of Robert Menzies. Not since Chifley, has there been a vision of Australian national recovery on a scale such as now contemplated by Scott Morrison and Josh Frydenberg.

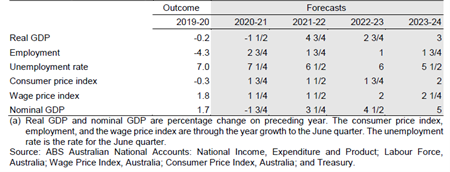

Figure 1: Major economic parameters

Advertisement

SOURCE: Budget Paper No 1: 2020-21, Table 2: Page 1-8

The Treasurer expects that Australian GDP will fall by 3.75% in calendar 2020 and rise by 4.25% in calendar 2021. This compares to our most recent estimates of a fall of 3.5% in calendar 2020, followed by a rise of 4.0% in calendar 2021. Our outlook and that of the Australian government, are consistent with that of the Federal Reserve for the US economy.

These growth rates on a financial year basis translate into a decline of 1.5% in 2020-21 and growth of 4.75% in 2021-22. The government expects this will be followed by growth of 2.75% in 2022-23. This is followed by a growth of 3.0% in 2023-24.

Unemployment rises to 7.25% in mid 2021, before declining to 6.5% in mid 2022, then 6.0% in mid 2023, and 5.5% in mid 2024. We said last week that the RBA would continue quantitative easing until unemployment fell to 4.5%. This would now appear to not occur until some time after 2024. We see that nowhere in the outlook until mid 2024 does Australian inflation rise to the RBA target of between 2% and 3%.

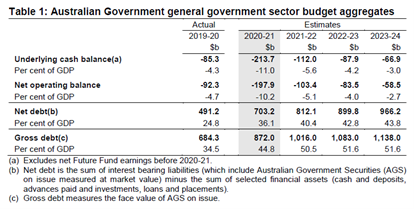

In Figure 2 below, we see the Australian General Government sector aggregates. A powerful program of recovery is supported by a powerful program of fiscal stimulus not seen since World War II. A deficit of 4.3% of GDP is followed by a deficit of 11% of GDP in 2020-21. This then declines in 2021-22 to 5.6% of GDP. It then eases in 2022-23 to 4.2% of GDP. It then declines further in 2023-24 to 2.7% of GDP.

The result is that Australian Government net debt to GDP rises from 24.8% of GDP in 2019/2020 to 43.8% of GDP in 2023-24. Although these debt levels are very high numbers in Australian terms, they are far below what will be experienced by the United States and the United Kingdom.

Advertisement

Figure 2: Budget aggregates

SOURCE: Budget Paper No 1: 2020-21 Table 1: 3-6

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

6 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon