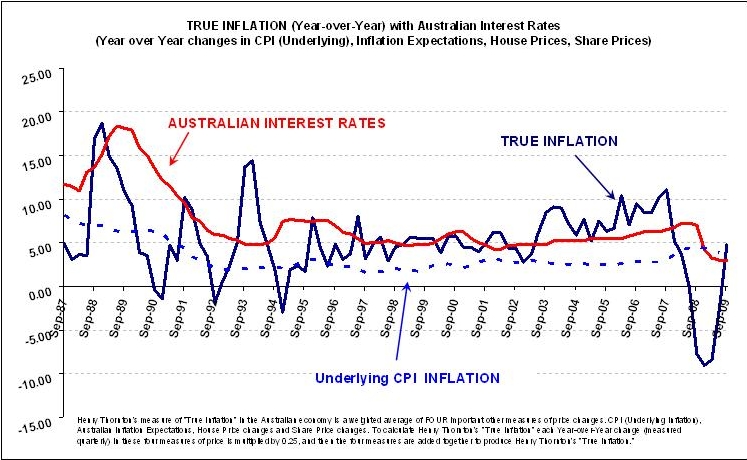

For much of the period since the late 1990s, True Inflation and Underlying CPI inflation showed reasonable similarity of movement - both rising, with True Inflation rising faster on average but with greater volatility. But at the end of the recent boom there was a major divergence. Asset prices - especially share prices - and cash rates also fell sharply, although with a distinct lag.

Now we all know that correlation does not mean causation. Someone wishing to criticise Henry's line of thinking might say that the sharemarket crash was a symptom of the general economic panic and it was the latter fact that led the Reserve Bank to cut interest rates so sharply. A defender of using share price data as a guide to monetary policy action might say that share prices anticipate economic fluctuations, but either answer leads one back to the discredited "check list" and most people (not Henry!) would say that way lies madness.

Henry's current thinking relies far more on economic theory. The logic is seen most clearly in a series of simple propositions:

Advertisement

- Inflation is always and everywhere a monetary phenomenon (Friedman);

- In normal circumstances, asset prices and goods and services prices will move in similar ways, and simple rules for monetary policy will produce reasonable results;

- However, in an increasingly complex world, inflation of just what (and when) depends on circumstances in particular markets. (Globalisation is a massive cause of complexity even with floating exchange rates);

- If goods and service markets have little inflation, excess money will raise asset prices;

- Conversely, if asset markets are depressed, goods and service inflation will be where excess money shows up more quickly and more certainly;

- If there is a general state of depression, excess money will pool more or less uselessly and monetary policy expansion will belike "pushing on a string" (Keynes).

Economic theory has not yet convincingly integrated markets for goods and services and assets - with "money" as a special case - as a vital part of the economic infrastructure and as a popular buffer stock for individuals and firms.

Henry is confident that when such a theory is ultimately worked out and tested, the six propositions set out above will be consequences of the theory.

Today or early next month, the Reserve Bank will raise the cash rate either by 25 or 50 basis points. Henry's inclination would be to wait another month and then hike more boldly by 50 basis points - provided the local economic data still indicate recovery and provided there is no major global economic setback.

And provided True Inflation is still rising.

Advertisement

Henry Thornton's measure of "True Inflation" in the Australian economy is a weighted average of FOUR important other measures of price changes. CPI (Underlying Inflation), Australian Inflation Expectations, House Price changes and Share Price changes. To calculate Henry Thornton's "True Inflation" each Year-over-Year change (measured quarterly) in these four measures of price is multiplied by 0.25, and then the four measures are added together to produce Henry Thornton's "True Inflation".

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

3 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon