Interest rates are unlikely to change today following the Reserve Bank's board meeting.

The board and the staff need to ponder the current state of the major economies and that of Australia's, and also forecasts and risks.

As well as global risks discussed below, there is the risk posed by Australia's labour market, where unemployed and underemployed resources are far larger than official statistics suggest.

Advertisement

Rate hikes anytime soon would exacerbate this issue.

A key question about the international economy is: could the current global economy, or important parts of it, be unstable?

In economics, it is usual to discuss one's expectation or "best guess" about future development and also to articulate potential risks.

For the past 18 months or so, the "best guess" was first of a nasty slowdown, morphing into a "Great Recession" as the International Monetary Fund called it in early March of this year.

The IMF warned on Tuesday that the world was gripped by a "Great Recession" that could throw millions back into poverty and spark civil unrest, as the US appealed for joint action by nations to tackle the crisis.

There has been "joint action" aplenty. Substantial monetary and fiscal expansion has been the rule everywhere, including in Australia.

Advertisement

For the past year, the most discussed risk has been that of the world's financial system tumbling down. This risk was underlined in September last year, when the US declined to save Lehman Brothers. Global credit markets were gripped by fear and bankers lost the trust in other bankers. For a substantial period, the world economy wobbled on its axis.

Other US (and British) banks were bailed out and gradually a measure of trust has been rebuilt among financiers.

Yet nagging concerns remain. European banks own a lot of the debt of bankrupt or severely stretched Eastern European nations, and there is no united European government to lead the bailouts should this become necessary.

In China, banks were exhorted to lend like drunken tavern keepers in the first half of 2009 and now are being told to sober up quickly. This injects a natural instability into the major developing economy in the world, whose health is vital to Australia.

Australia has injected substantial fiscal stimulus, mostly in the form of handouts to middle and lower-income taxpayers and spending on schools and houses that will have little, if any, positive effect in promoting productivity.

The Prime Minister's latest economic advice to the nation stresses the importance of promoting productivity, so perhaps there is some implicit recognition of mistakes made in panic when it seemed a nasty downturn was becoming a Great Recession.

Australia's monetary expansion was in nominal terms not so dramatic as that in other nations, where nominal cash rates have been close to or actually zero.

With continuing inflation of consumer prices in most nations, one can argue "real" rates of interest are effectively negative.

The latest measure of underlying consumer inflation of 3.9 per cent suggests for Australia not a very different picture of monetary policy of extreme ease.

Rarely has monetary and fiscal policies been eased so quickly by so much, never before except in major wars. Wars have almost always been accompanied or followed by major inflationary outbursts, which suggests a clear and present danger.

Put "inflation" with bank failure on the list of serious risks to recovery.

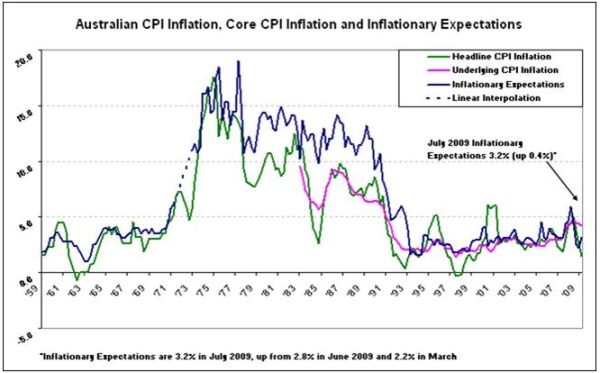

The graph shows a 50-year history of consumer inflation and household inflationary expectations. The great inflation of the 1970s is clearly evident, sparked by the actual war in Indochina and the unwinnable war on poverty of US "Great Society" spending. The long struggle to eliminate inflation during the 1980s and in the first half of the 1990s involved costly recessions and high rates of unemployment.

The inflation of the late 1990s and the early noughties was, however, most evident in asset prices. As we argued at the time, central banks were confused by their operational focus on consumer price inflation when that indicator was held down by China's emergence as a major producer of cheap manufactured goods.

Excessively easy monetary policy spilled instead into asset prices, which became in many markets asset bubbles.

The Great Recession is the more or less inevitable consequence of asset bubbles bursting following realisation of foolish and reckless over-borrowing and over-spending by households, over-lending by banks and over-complication of financial instruments (to the point that the financiers themselves lost touch with the risks they were running).

And, it must be added, lack of diligence by central banks allowing overheated bubble economies to develop with bank regulators allowing unsustainable practices to flourish.

(As just one recent example, it has emerged that US regulators were told more than once about the Bernard Madoff scam, but the fact that their investigations failed surprised even Madoff himself.)

To return to the graph of consumer inflation, note the gradual rise from the mid-1990s, as near to a new trend as the naked eyeball will detect.

Until very recently, it was widely assumed that the Great Recession would take care of inflation. Reserve Bank governor Glenn Stevens has recently showed renewed concern at the risks of inflation, and market participants have swung from the assumption of rate cuts to come to the view that the next move in cash rates will be upward.

This volatility of expectations is itself a sign of instability in the economic fabric.

But there is also the risk of "poverty and civil unrest" as unemployment and underemployment builds.

Australia is officially judged to be a nation where unemployment is likely to peak at about 8 per cent of the workforce. So far, official (ABS) unemployment has risen from a low point of 3.9 per cent to a "mere" 5.7 per cent.

The Reserve Bank has lifted its game under the leadership of Stevens. It responded briskly to the Great Recession with several 100-point cuts to cash rates from October last year.

It is showing signs of recognising the importance of asset inflation and deflation, though so far there is no attempt to tell us how this gets allowed for in operational decisions. And it has explicitly recognised the importance of inflationary expectations.

But people far closer to labour market realities than public officials with firm tenure have been arguing for some time that unemployment and underemployment is far greater than suggested by official ABS statistics.

In fact, the latest figures from Roy Morgan suggest the actual rate of unemployment is 7.6 per cent and there is a further 9 per cent of the workforce who would like to work longer hours if work were available.

This is a structural issue that requires careful analysis leading to policy reform by government.

But the Reserve Bank cannot and should not ignore it in its decisions about interest rates. It creates a third risk to recovery, with bank failure and inflation.

Even without further bank failures, the risk of rising inflation and the certainty of rising unemployment is an inherently destabilising combination.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon