An objection might be that governments would be unable to find people able to run failed banks, vehicle companies or property developments. I suggest this would be the least of governments' problems, as there are many competent older people who would welcome the chance to earn a modest salary (perhaps also a modest bonus for stellar performance) in return for reintroducing conservative old-fashioned management practices in newly or part-nationalised companies.

There is a point specific to the Australian banking sector. Much is made of the relatively sound position of Australia's banks. The truth is that they funded housing loans with overseas borrowing. When the global credit markets froze, Australia's banks were in real trouble. They were bailed out by the government lending them its AAA rating.

If a wealthy entrepreneur had provided the bailout (as Kerry Packer did for Westpac in the previous crisis) he would have taken a large slice of equity in return. Why should Australia's taxpayers not get equity for the bank bailout in this crisis?

Advertisement

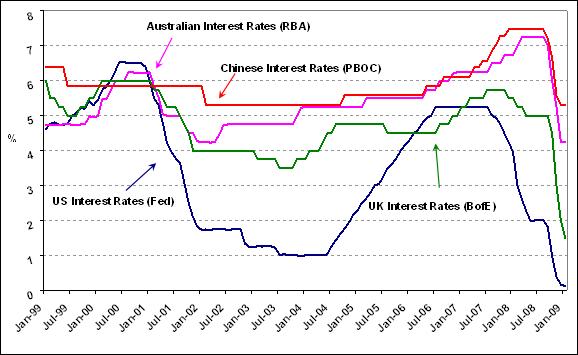

I return now to a discussion of monetary policy. Henry has for several years said that US cash rates were too low in the early years of this century, and this view has gradually become more widespread. The result of US cash rates at 1 per cent in 2003-04 was a series of asset bubbles and the build-up of consumer inflation globally.

Now US cash rates are again close to zero, and the US Fed is again flooding the world economy with liquidity. It will be impossible to withdraw liquidity when global recovery gets under way, and there will be another bout of asset inflation, leading inexorably to consumer inflation and eventual monetary tightening too little too late, overshooting and another episode of global slowdown.

Other nations cannot avoid this stop-start instability. In theory, a flexible exchange rate enables any particular nation to avoid being carried along for the ride, and this is especially the case when the most important global currency - the US dollar - is generating the global instability.

The growth of money and credit in Australia has declined substantially. But liabilities of the Reserve Bank have exploded in the past quarter to be an alarming 73 per cent above the level of 12 months ago. This deserves serious attention and explanation.

I have the following suggestions for Rudd and Swan and for the Reserve Bank's Glenn Stevens.

Rudd and Swan, by all means implement more fiscal expansion. The more you can focus on policies that boost productivity and contribute to Australia's competitiveness, the better it will be for our economy and therefore our battlers. This means policies that encourage households to save and to work, and that stimulate productivity.

Advertisement

Glenn Stevens, try to avoid too much easing of monetary policy. Australia can to some extent stand aloof from the rush to reduce interest rates to a point that makes another burst of inflation inevitable. You are best placed to judge that point, but your aim should be to facilitate real growth of, say, 4 per cent with inflation of 2 per cent. A modest undershoot of cash rates consistent with that growth is sensible now, but please remember the adjective.

And Henry implores Australia's powerbrokers to devise a fair and effective back-up system of corporate recapitalisation where market solutions fail and injection of taxpayers' funds is necessary to promote and preserve employment. In particular, there should be no taxpayer-funded corporate bailout without the government taking equity.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

2 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon