In the last election Howard’s promise that interest rates would always be lower under the Liberals than Labor may have been crucial to him holding mortgage belt seats.

My colleague John Black found no statistical relationship between the swings that actually occurred and average mortgage sizes, but he found a relationship in other seats. His theory was that the interest rate issue didn’t so much affect those who were buying houses, as it affected people, like their parents, who worried about the home buyers. Our questions aimed to test these hypotheses.

We also wanted to know how real "mortgage stress" is. Are those who spend more than 30 per cent of their income on mortgages rich enough to afford it, gearing into investments, or desperately hanging on to a toe-hold in the housing market?

Advertisement

Last, we wanted to know whether voters blame Howard for high interest rates and whether nervousness about them made him more or less attractive to voters.

Our sample swings to the left, and compared to the average is older, slightly richer and more likely to own a home, and 27 per cent of those with mortgages were making payments putting them in "housing stress". Despite being more affluent than average they gave us valuable leads on these questions.

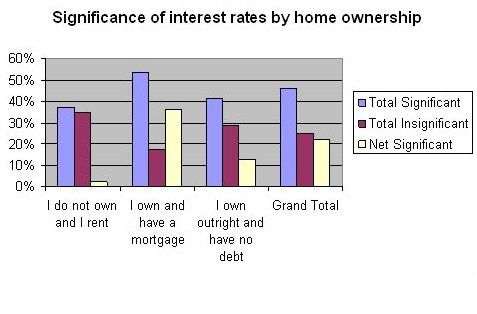

Interest rates were a significant issue for all groups, except for those renting. Just more than a third of renters thought it was a significant issue, and about the same percentage thought it wasn’t. For those with a mortgage the figures were 54 per cent and 17 per cent, while for those who owned outright they were 41 per cent and 29 per cent.

If you were paying more than 30 per cent of your family income in rent, then the figures were 65 per cent significant, 11 per cent insignificant. Safe to say that even if these respondents have bought boats, holiday homes and investments they’re still worried about the holding costs.

There wasn’t much altruism evident. When we coded qualitative responses from swingers, 23 per cent of them came up with a variant of "I’m alright Jack" while 21 per cent said "I’m suffering", or words to that effect. Eleven per cent were primarily worried about the effects on people other than themselves. These were mostly aged between 55 and 64, the age when you are most likely to have offspring buying a house. Another 6 per cent actually saw a personal benefit in higher interest rates, and were also generally older, so were probably net lenders.

A problem for Howard is that 11 per cent of swingers volunteered that governments had no effect on interest rates, and a further 6 per cent said it was a significant issue because he had lied about them last election. "… I believe the Liberal Party will again lie and claim they'll keep interest rates low, or lower, or at record lows (pick this week's lie)."

Advertisement

We also looked at those in mortgage stress and the personal impact was overwhelming - 47 per cent were personally suffering. But only 8 per cent nominated coalition lies. It seems that while mortgages are hurting, the government isn’t necessarily being blamed.

So, who is more likely to keep interest rates lower? The answer to this was fascinating. 80 per cent of Coalition voters nominated the government, but Labor voters had no confidence in their own side with only 13 per cent nominating them as the best. The apparent discrepancy is made up by those who believe neither side has an edge with 69 per cent of Labor voters calling it a draw, compared to only 15 per cent of Coalition voters.

A closer look at swinging voters makes this better for the government. Those voters who have crossed to Labor believe that Labor is better able to handle interest rates than the Coalition, by 21 per cent to 7 per cent, but those who are unsure, or moving from Labor to Coalition more strongly nominate the Coalition over Labor. So, while "Neither", a neutral position, is the answer for 50 per cent of swingers, a quarter tend in the government’s direction as a result of interest rates.

The reason for this is clear looking at the qual. The Liberal Party enjoys a good record in voters’ eyes of keeping interest rates low, while the Labor Party doesn’t. Those who favour Labor to keep rates lower rely on abstracts like the parties’ policies. They also point to recent rate rises under Howard.

We’ve also analysed these responses with the Leximancer software. As the attached map shows, "Howard" is a negative for the Liberals on the issue, but "Rudd" isn’t even present, strange given his presidential approach. "Labor" is negative for the opposition and is associated with the Liberals being best to lower interest rates. The debate is dominated by perceptions of risk and looking for the party least likely to make rates higher, rather than likely to make them lower. IR is also absent as a concept, suggesting both that job insecurity is not an issue with interest rates, and also that the Liberal Party has not been successful in linking IR reform with a better economy.

All in all, this is not a strong hand for Howard, but it is an even weaker hand for Rudd. In the no-holdem game of political poker, if I were Howard I might be prepared to play this game to the end, particularly given the number of dud alternatives hands there are lying around.

Click for full image

First published in What the people want on September 23, 2007.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon