Henry and his fellow senior Australians have been privileged to live through several major episodes of economic reform. The first was sparked by the float of the dollar in 1983. This changed the rules of the economic policy game - more power to the Reserve Bank, less power to Treasury. Following the float, economic reality intruded as never before into the Cabinet room.

Related policy changes, including the deregulation of finance, Labor's "accord" with the ACTU and the adoption by the Hawke-Keating Labor government of disciplined fiscal policy were partly, perhaps largely, a consequence of that fateful decision to float the Australian dollar.

John Howard's Coalition Government continued the process, at first cautiously, even nervously. It made the Reserve Bank responsible for achieving inflation targets - taking politics out of the setting of interest rates. It began cautiously to deregulate labour markets, introduced the GST and began to reduce rates of income tax. Together this set of changes amounted to another serious economic reform package.

Advertisement

Internationally, the rise of China, its flood of cheap manufactures and insatiable demand for commodities, has provided benefits to most Australians of massive proportions. China has kept inflation low - making the newly "independent" Reserve Bank look good, and boosting consumers' buying power.

China has greatly increased demand for Australia's commodity exports. China has massively boosted Australia's terms of trade but - and this is a vital "but"- this has not led to a wage explosion or a grossly overheated economy. This is largely a consequence of past economic reforms, reinforced by the latest economic reform package. The latest burst of economic reform is that based on the Howard Coalition Government's WorkChoices Legislation.

There are various shreds of evidence that WorkChoices is a major reform. Most obvious are the vociferous objections of organised labour. If WorkChoices were not severely affecting union power, union leaders would not be fighting it so powerfully. More evidence comes from the new policy's unpopularity in published opinion polls. Change is often unpopular, with the losers - in this case organised labour - complaining loudly while the winners quietly take the credit for their own presumed sagacity and business acumen.

The economic effects of WorkChoices have been masked by unreliable economic data. Statistics on even such a concept as total employment and total unemployment have been biased and inaccurate, as we have argued. Official wage and labour cost data, we suspect, do not fully take into account the loss of traditional benefits - "Union Rorts" might be a fairer description - such as long tea breaks, double or triple time after hours or on weekends, unrecorded sick days and other forms of working to rule or in some cases against the apparent rules.

The many business persons to whom Henry talks almost universally report liberation from irrational and outmoded work practices and a freeing from impediments to improved productivity. Overall effects are hard to quantify but are palpable in the workplace.

Despite the poor quality of official government (ABS) data on employment and unemployment, one obvious effect of WorkChoices is the surge of employment revealed in the past year. The magnitude of jobs gained has surprised everyone, sure evidence that something big has changed. More (indirect) evidence is the subdued overall growth of wages despite major areas of the Australian economy operating at or even beyond any traditional definition of full employment.

Advertisement

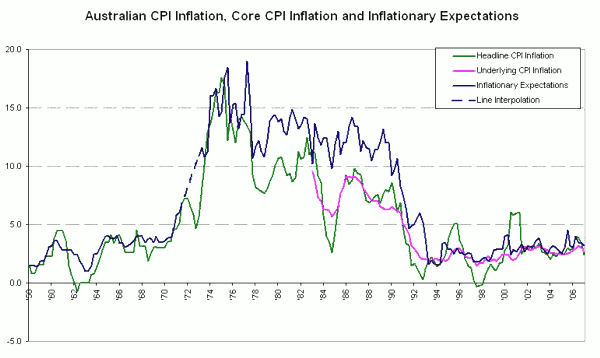

Now the latest evidence is the surprisingly low inflation numbers in recent quarters. In the December 2006 quarter, "headline" inflation was -0.1 per cent against the average economist's expectation of 0.2 per cent. In the March quarter of 2007, the outcome was an increase of 0.1 per cent against an average expectation of 0.6 per cent. Or using the Reserve Bank's measure of "underlying" inflation, the run of quarterly increases is from 0.9 per cent in the June quarter 2007, to 0.75 per cent in September, 0.5 per cent in December and 0.5 per cent in the March quarter of 2007.

Sources: CPI Inflation, ABS; Underlying CPI inflation - "weighted median", Reserve Bank of Australia; Inflationary Expectations, Melbourne Institute and Henry Thornton.com

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

12 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon