It’s (almost) official - the Reserve Bank "is still undecided as to whether it will lift interest rates next week, according to one of the world's most prominent global economists".

This is the line being peddled by said economist, David Hale. The story was told last week on Lateline, and reported in this newspaper.

Henry wonders what it takes to get a briefing from the RBA. We offer ourself as "one of the world's most prominent virtual economists", and we promise not to spill the beans on Lateline.

Advertisement

The Reserve Bank board meets today, and our task is to provide advice that will help its members make up their minds. We also suggest that the independent members of the board question officials about the practice of providing private briefings to economists from the private sector.

We infer (not having the benefit of any private briefings) there are at least two views among the staff of the Reserve. The natural, conservative, view is to do nothing if at all possible - very likely the view of governor Glenn Stevens.

Then there is the view of chief economist Malcolm Edey, who recently spoke in more radical terms. Henry's translation: let's make sure inflation is properly under control.

"The Bank's inflation forecast, as presented in the Statement on Monetary Policy in early February, was that underlying inflation would decline slightly over the next two years to around 2 per cent. This outlook is still higher than ideal: it implies that inflation is more likely to be too high than too low in the period we can foresee.

"Information that has become available since that forecast was made suggests that some of the factors pushing up underlying inflation last year remain in place. The December quarter national accounts recorded relatively strong growth in demand and output. We also have some additional data on wages, which showed that growth in the Wage Price Index remained around 4 per cent in annual terms at the end of last year.

"This needs to be interpreted carefully, because the September quarter outcome, and hence also the annual figure, were artificially held down by a change to the timing of last year's minimum wage decision. The outcome for the December quarter, which was unaffected by that, was a quarterly increase of 1.1 per cent, which was at the top end of its historical range.

Advertisement

"In summary then, the recent round of data has pointed to relatively strong outcomes for demand, output and wages growth in the December quarter. As always, the Bank will be giving careful consideration to these developments, along with other incoming data, as it continues to review inflation prospects month by month."

Henry guesses that deputy governor Ric Battellino is a hawk. This is his natural bent, and conforms to the traditional role for the deputy governor, especially one whose age makes it likely he will never be governor. He will emphasise the continued strong growth of credit on top of other bullish local economic data.

Private members of the board have a natural tendency to dovishness on monetary policy. This is because their business interests will prosper (at least in the short term) more with easier rather than tighter monetary policy.

Naturally this is not always the case - mining men are usually hardliners, and I would expect Hugh Morgan to be among the hawks at today's meeting.

Geopolitical pressures mean that the price of oil has lurched upwards by around $US16 a barrel since the low point of $US50.50 on January 19. This will be used both by hawks and doves - the hawks because price rises will increase oil price inflation and at some stage this will spill into other prices (including wages) and the doves because higher fuel prices will dampen household and business spending. And they will make the case this is equivalent in its effects to monetary tightening.

The doves will also point to weaker economic news from the US economy and rises in the value of the Aussie dollar.

As to the US economy, last week US Fed chairman Ben Bernanke explained his views to Congress - the appropriate but indirect way to communicate with market participants, incidentally. He made the point that the state of US growth and inflation is bedevilled at present by more uncertainty than usual. He was, however, at pains to point out that the Fed retains its vigilance against inflation.

Is the rising Aussie dollar a reason for holding back on interest rate hikes? In the 1980s RBA governor RA (Rob) Johnston used to argue that a rising exchange rate was effectively a "tightening of monetary conditions". This led the Reserve to go easy on monetary policy at some vital times, and this in turn led to an overheated boom, rising inflation, eventual large interest rate hikes and then the "recession we had to have".

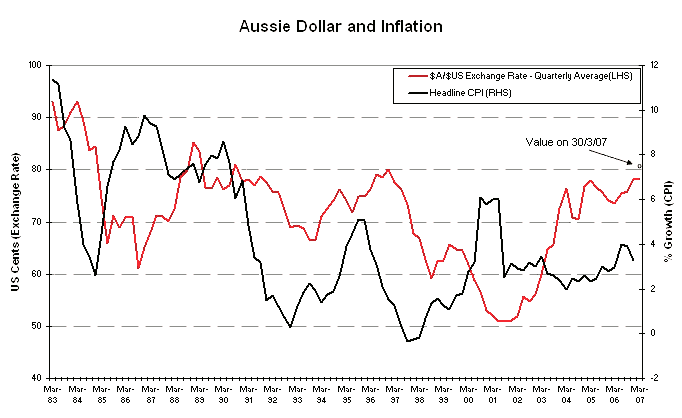

For this reason the Reserve nowadays tries not to be deflected by the state of the currency. But this matter is not just based on memories of burnt fingers. Consider the graph above.

If a strong dollar reduced CPI inflation, one would expect a negative correlation.

A rising dollar certainly helps contain inflation, but there is a lot of research that says this effect is small and hard to detect. There is no obvious negative correlation between CPI inflation and the value of the Aussie dollar.

Instead, there is a lagged positive correlation. This suggests that the main causation runs from inflation to the currency.

This is because high inflation makes the RBA raise interest rates and this (ceteris paribus) puts the currency up, and vice versa.

Positive correlation with a lag is the right interpretation of this graph. The only exception is at GST time, when (I assert) market participants for a time expected the coalition would lose the GST election and marked the dollar down despite high headline inflation.

We have disposed of the two main arguments of the doves. There are strong arguments for the hawks. The Reserve should raise cash rates tomorrow by 25 basis points.

If they do not, inflationary pressures will continue to build in the Australian economy.

First published in The Australian and on Henry Thornton's website on April 3, 2007

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon