The board of the Reserve Bank meets today just as the various football codes prepare for their respective final series.

Henry expects no news from the Bank tomorrow as it waits both for more international news - especially about the state of the US economy - and about the effects of rate hikes in May and August on the Australian economy.

The Bank's retiring Governor will be able to watch the footy finals with a mind unclouded by the need to ponder how many rate hikes will be needed here, a question his successor, Glenn Stevens, will be grappling with for the foreseeable future.

Advertisement

With credit growth still too high for comfort, unemployment at record lows and the housing market recovering in the southeast of Australia and out of control in the west, we expect that at least two more rate hikes will be needed, and quite possibly more.

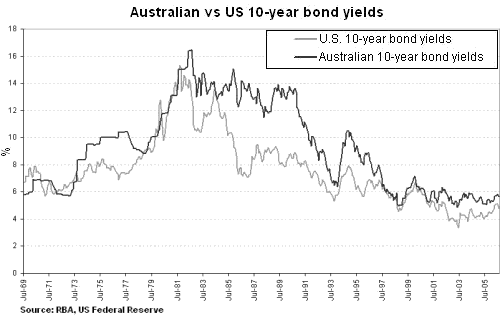

The graph shows US and Australian bond yields. The traditional premium demanded of Australian yields was largely eliminated in recent years. But the main point of the graph is the recent rise in yields as global interest rates rise, although we acknowledge the very recent, and (we think) temporary, reduction.

The big economic news in the past month - leading to that temporary bond yield decline - has been signs of a slowing US economy and related easing of concerns about inflation. The US Fed led the way on August 8 with a pause in its hitherto relentless series of rate hikes.

Since their most recent peak in late June, yields on long bonds in the US have fallen more than 50 basis points from 5.25 per cent. China has also continued to tighten monetary policy and this seems to have weakened admittedly overly buoyant expectations in Japan and other Asian economies. Interest rates have also been raised in the past few months in Canada, Britain, Euroland, Thailand, Korea and Malaysia.

Weak economic data, particularly housing data, has validated the Fed's pause. Solid employment news on Friday night, however, has somewhat relieved current anxieties and one cannot be confident that there are no more US rate hikes to come.

Advertisement

Signs of slowing in the US economy and tightening of monetary policy elsewhere have gone with a substantial decline in the price of oil. From its peak on July 14 at almost $US78 per barrel, the price of oil has declined to $US70. This is partly due to perceptions of weakening demand, but also because of some lessening of geopolitical tension.

Henry was gobsmacked when the Hezbollah leader announced on global TV that if he had known how Israel would react, he would not have kidnapped their soldiers. This has been variously interpreted as acknowledgment that Israel won the war, to a saner analysis that there were only losers in this conflict.

This was a battle by proxy between the United States and Hezbollah's supporters and sponsors Iran and Syria.

The massive damage inflicted by both sides will have reminded the interested parties that massive damage would be the only certain outcome of any wider conflict. But Iran has said it will pursue its nuclear program despite the United Nation's request that it stop. So the recent lessening of geopolitical tension may be only temporary, and Iran's big implicit threat is to close the Straits of Homuz and therefore cut off most of the flow of oil to the West.

Oil would quickly rocket upwards in price from levels that are already far too high for comfort.

No central bank can set monetary policy for fear of every contingency. But the high price of oil, and the plausible threat that it could go much higher, is a fact to be taken into account and will impose some caution.

A more general reason for caution is the increased uncertainty about US economic growth, based especially on various bits of negative news about the US housing markets.

What of the local economic news?

Commodity prices remain high and the nation is in the midst of a mining boom of enormous importance. In the past month, Henry's impression is that many more people are recognising that this boom may run for a substantial time, ultimately reversing a century of declining terms of trade. It is worth recalling that in the late 19th century Australia was the world's richest nation, and that such a situation could come again.

As the Prime minister has said, Australia has the opportunity to become an "energy superpower" but the strains involved in managing this should not be underestimated.

The dual economy, with powerful booms in the mining states and near-recession in the traditional manufacturing heartland in the southeast corner, may become semi-permanent.

Inflation was worrying in the June quarter, and the Reserve has acknowledged that underlying inflation is now expected to be close to the top of its 2 to 3 per cent target range for the next year or so. Credit growth is still too fast for comfort - total credit provided to the private sector by financial intermediaries rose by 1.2 per cent over July 2006, following a rise of 1.1 per cent over June. For the year to July, total credit rose by 14.8 per cent, noticeably higher for business than for households.

Unemployment is at a multiple decade low of 4.8 per cent.

Although this is not the full story (as there is still a lot of hidden unemployment) skilled labour is undeniably in short supply and wages pressure is building gradually. Even house prices are showing signs of revival in the southeast corner, and are positively out of control in the frontier resource economy of the wild west.

Henry is encouraged by signs that Treasury, as well as political government and the Reserve, is now aware of the dangers inherent in the current and likely future situation.

Monetary policy cannot provide the full control mechanism for the potential "energy superpower". Knowledgable observers will be keenly awaiting the Government's response in the next budget. We note that fiscal action before then should not be ruled out.

But the Reserve will be well aware that loss of control over inflation would throw away hard-won credibility and that restoring credibility would be costly.

First published in The Australian on September 5, 2006 and on Henry Thornton's website.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon