and next year the deficit is expected to be:

2025 7.05%.

The cause of higher levels of inflation under the Biden/Harris administration appears to be a continuous high level of fiscal stimulus, which is much, much higher than the long-term historical level of US stimulus. Significant high points of Biden/Harris fiscal stimulus were:

Advertisement

- The American Rescue Plan Act of 2021 of $US1.9 trillion

- The American Jobs Plan of March 2021 of $US2.3 trillion

- The American Families Plan of A$US1.8 trillion

- The Inflation Reduction Act of $AUS520 billion

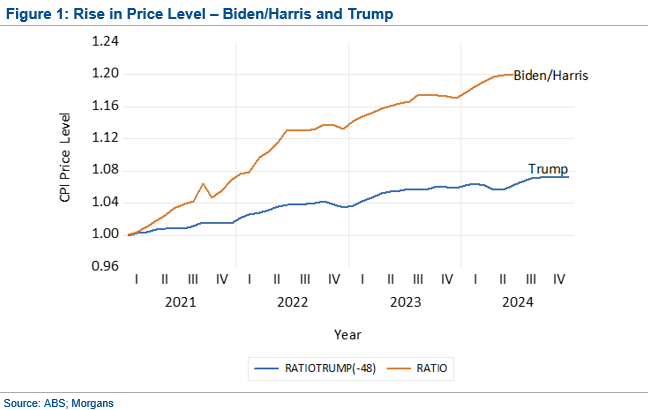

We think that what is most important for ordinary citizens is the cumulative effect of this inflation. This total increase in the cost of living can be shown as the rise in the price level. We can compare the rise in the price level during the Trump administration and the Biden/Harris administration in Figure 1.

Source: ABS; Morgans

Over the four years of the Trump Administration from January 2017 to December 2020, the price level rose by 8.4%. Over the three and a half years of the Biden/Harris administration so far reported from January 2021 to June 2024, the price level rose by 19.9%. By December 2024, we can expect that the price can rise by 22.2%. This will be 13.8% higher than the rise during the Trump administration. For those on fixed incomes or in small businesses, this rise in prices of more than 20.0% is a major fall in REAL income.

Back in 1935 when Maynard Keynes published "General Theory", he forecast that running big budget deficits would increase the price level. This increase in the price level he said would reduce real wages. These lower real wages would increase employment. Now all these years later Biden/Harris have demonstrated that this is true.

Advertisement

As an economist, I appreciate that Biden/Harris have demonstrated that Keynes hypothesis is true. Whether American citizens are equally appreciative is something we may be about to learn in November.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

In Hong Kong, research is issued and distributed by Morgans (Hong Kong) Limited, which is licensed and regulated by the Securities and Futures Commission. Hong Kong recipients of this information that have any matters arising relating to dealing in securities or provision of advice on securities, or any other matter arising from this information, should contact Morgans (Hong Kong) Limited at hkresearch@morgans.com.au

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

2 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon