The "Inquiry into Price Gouging and Unfair Pricing Practices" is the latest ship to be launched in the Australian Council of Trade Union's (ACTU) armada of misdirection to shift the blame for inflation from the real culprits-the Reserve Bank of Australia (RBA), and state and federal governments in combination with Labor unions-to business.

It is probably no coincidence that it was released about the time the crossbench was waving through the government's new, back-to-the-70s, "Closing the Loopholes" industrial relations bill.

It's cleverly done, superficial, and will easily slot into most journalists' needs for a compelling narrative of heroes (trade unions), villains (business), and victims (the rest of us)-but it happens to be mostly wrong.

Advertisement

Particularly clever is the use of Alan Fels, the first chairman of the Australian Competition and Consumer Commission (ACCC), as the inquiry head-it gives the exercise superficial credibility that it doesn't deserve.

The inquiry's title assumes its finding-when you are investigating price gouging, then you will find price gouging.

Undoubtedly, this is why there is no objective definition of what price gouging is when you search the document.

In fact, there are two subjective definitions.

Price gouging is "excessive" prices, or "prices that significantly exceed levels that would occur if there was competition."

What is "excessive"? Are there many, or any, situations in corporate Australia where there is no competition? How do you tell what prices would be with competition?

Advertisement

None of this is explored or given any concrete definition. The term is just flung around when convenient and is meant to have an emotional resonance.

The Cambridge dictionary definition gives the game away.

Gouging is "to charge someone too much money for something, in a way that is dishonest or unfair" [my emphasis]. It also comes with a profoundly physical image of viciousness, as when you "gouge out an eye."

The report also has multiple definitions of what "inflation" is.

First, it confuses inflation with price rises. Inflation is not price rises, although price rises can be a symptom of inflation.

Inflation is conventionally understood to be caused by too much money chasing too few goods leading to an erosion of the value of the currency while the value of the goods stays the same.

Mr. Fels more or less adheres to this definition of inflation in his analysis of the rise in prices immediately after we re-opened after COVID-19.

Most commonly, inflation is caused by governments issuing too much credit either through printing money or borrowing.

Some of this occurred during and post-COVID as we massively expanded the size of government expenditure without increasing taxes, but it also coincided with a decline in the amount of goods available due to the disruption of the economy.

A pedestrian moves along an almost empty George Street in the Sydney CBD, Australia, on June 28, 2021. (Lisa Maree Williams/Getty Images)

So there was an increase in credit, inflationary in itself, with a decline in the number of goods, leading to a more accentuated inflation than would occur if each had happened on its own.

So Mr. Fels' analysis agrees with the conventional definition-until it doesn't.

He introduces the idea that after the post-COVID bounce, corporate profits drove inflation.

He claims profit margins expanded and ignores the possibility that perhaps input costs continued to increase, as a result of inflation built into the system, and the exogenous shock of war in Ukraine, which drove energy prices sky high.

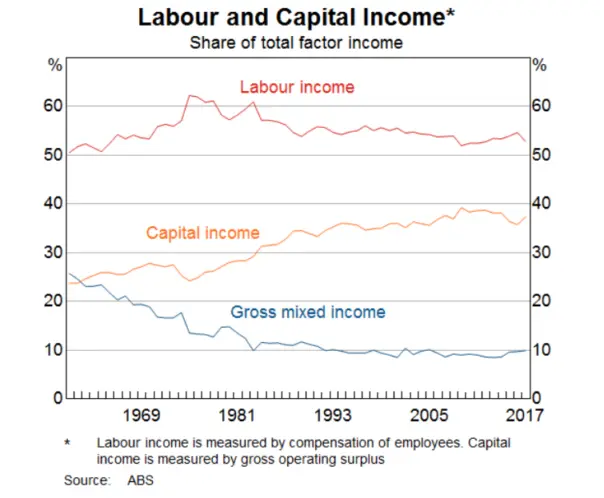

The justification for claiming corporate profits is the villain is contained in figures showing a decline in the share of the economy of labour. This can be seen in the graph below from the RBA March 2019 bulletin "The Labour and Capital Shares of Income in Australia."

(Reserve Bank of Australia)

Labour flatlines from the start of the graph, while capital income increases, although the greatest decline is in gross mixed income, which is a close proxy for small businesses.

However, all is not what it seems.

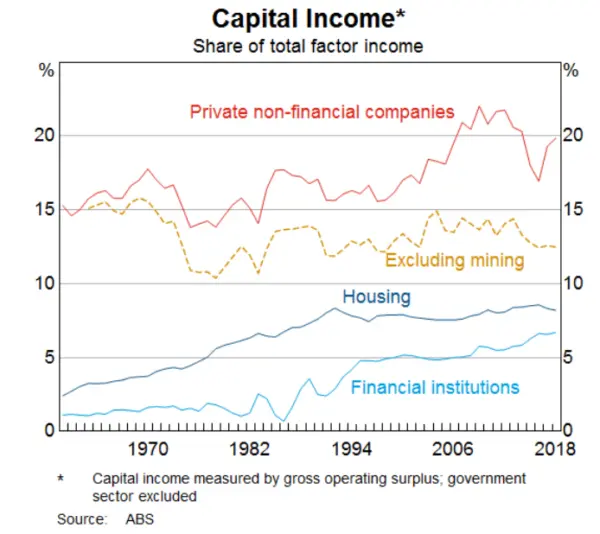

Capital income is not just corporate profits in the form of dividends but includes an amount for the rental income imputed to house owners. It also captures income from the mining sector.

Just excluding mining makes a huge difference as you can see in the graph below.

(Reserve Bank of Australia)

Or in this break-up of the contributions to capital income.

(Reserve Bank of Australia)

So when you strip out mining and the housing boom, there has been little change between the shares of labour and capital, contradicting the claim that corporate profits have suddenly accelerated.

And if their profits haven't accelerated, where is the justification for suggesting they are fuelling inflation?

Mr. Fels does localise his criticism to a number of industries, but again, where is his evidence of "gouging"?

And if there is an increase in prices, is it because of a deliberate corporate decision to increase profit margins, or has there been an increase in the underlying cost of doing business?

In other words, are businesses just passing on costs, or are they creating them by expanding margins?

What about energy costs?

Energy is singled out, in particular energy generators and suppliers like AGL. He's right to single out energy as it is present throughout the economic cycle.

But its cost is being driven by two factors.

One is the "energy transition" which is replacing reliable fossil-fuel-generated baseload power with unreliable wind and solar, and the other is external factors like the Ukraine war and energy policy in OPEC and the United States.

The price of energy is extremely cheap when renewables are available, often selling at literally giveaway prices of around -$50 a MWh. It can also be extraordinarily expensive with a top price capped at $15,500 (US$10,000).

Expensive electricity is a design feature of the way the government has slanted the electricity market and won't be fixed by Mr. Fels' policy of switching to a capacity market.

It's true AGL did post a massive half-year profit, but then it's only last year they posted a $1.2 billion loss, and then another $2.058 billion loss two years before that.

Energy is a volatile business.

Likewise, he complains about network charges, but what the price networks can charge is actually determined by a government regulator-how could that be price gouging?

Corporate profits have actually remained steady

Mr. Fels also picks on supermarkets, again without any proper analysis.

Ten years ago, Woolworths made a net profit before abnormals of $2.45 billion with a net profit margin of 4 percent. Last year, it was $1.652 billion with a net profit margin of 2.6 percent.

Rather than "price gouging" it has been giving increasingly better value for money over the last decade.

At margins like that, if Woollies dropped its prices by around 4 percent, it would no longer be a viable business, and that drop would be a one-off.

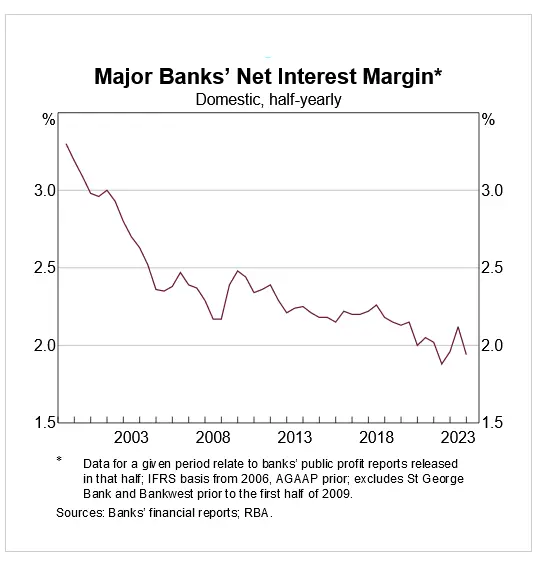

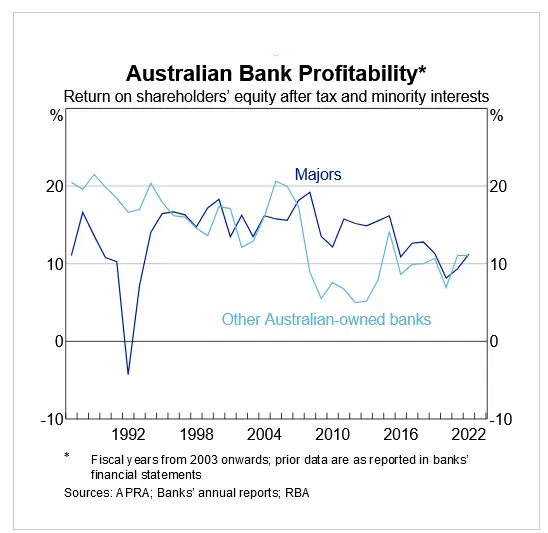

Mr. Fels also blames the banks.

Again, this charge does not hold up.

The return on equity of the major Australian banks has declined by around half since 2009, while their interest rate margin has declined by about a third since 2000.

(Reserve Bank of Australia)

(Reserve Bank of Australia)

Qantas is another target, but if you take the net of the whole of CEO Alan Joyce's tenure, it comes to about zero with losses equalling profits, and this was achieved by gross underinvestment in new airplanes.

Do I like paying Qantas' prices? No. Do I think they are providing Qantas shareholders "excessive" profits? Again, No.

Red tape forcing aged care and childcare providers to charge more

Then there is childcare, which he at one point says has declined in price, but apparently price "gouging" is an issue because centres in richer areas charge more than those in poorer ones.

I guess they will, and it might have something to do with higher real estate prices, and having to pay more to the staff so they can afford to live within a commute of the centre. And maybe rich parents expect higher standards and are happy to pay for them.

He also expresses concern in passing about aged care, but it should be noted that both aged care and childcare are heavily regulated by the government to the extent that the federal government even mandated an increase in aged care staff numbers at the same time as it successfully advocated for an increase in staff salaries.

If costs are going up, then government action, not profiteering, has a lot to do with it.

If we want real competition, why not look at union movements?

It's ironic that one of the underlying themes of the report is the need for a competitive market.

I agree, and don't by any means believe that we have perfect competition.

But Mr. Fels is writing this report for the union movement, the one sector of the economy allowed to engage in what would, in any other sector, be cartel behaviour, and where the rules are deliberately rigged to try to exclude new entrants.

Why didn't Mr. Fels look at whether union fees are value for money, or whether there is gouging going on there? After all, competitor unions like the Red Union offer comparable services at half to two-thirds the cost.

He might also have asked about some of the accommodations the federal government has made to the union movement, such as abolishing the Australian Building and Construction Authority, which policed the building industry, particularly the questionable behaviour of the CFMEU.

Or policies that mandate the use of CFMEU members on building sites, resulting in a 30 percent increase in costs.

Members of Victoria Police stand outside the CFMEU Office in Melbourne, Australia, on Sept. 21, 2021. (Darrian Traynor/Getty Images)

When a chippy working on a new school building earns more than the principal who will eventually run the campus, there is definitely price gouging, even on Mr. Fels sloppy definitions. (Although there is some karma in the fact that the chippy on his annual salary of $150,000 has just been dudded of his Stage III tax cut).

There are some good recommendations in the report. The remaining import tariffs on automobiles should go, and governments shouldn't be allowed to "needlessly restrict competition" (which should include a thorough review of the union cartels).

Some recommendations come completely out of the blue without any discussion, and are union-friendly.

One of them is the proposal to, if not abolish the secondary boycott rule, restrict it so it is only illegal if it lessens competition. This would of course make it legal again for unions to target suppliers of companies, so as to bring the company to its knees.

Then there is the abolition of non-compete clauses in employment contracts which appears to be completely unrelated to "gouging."

Providing cover if things go really badly

It looks to me like Australia is facing a rerun of the 70s when dramatically higher energy prices sparked a surge in inflation, fanned by government expenditure, borrowings, and expansive monetary policy. Wages were raised in an attempt to keep up, leading to "wage push" inflation as well as "stagflation" (inflation without growth).

Many of the same features are repeating, resulting in prices going up and wage increases accelerating to meet them.

(Reserve Bank of Australia)

The union movement is moving pre-emptively to deflect any blame from them, knowing that wage rises without productivity increases are unsustainable.

They're not going to blame their friends in government so it has to be big business. And who doesn't love to hate big business?

And Allan has gone along for the ride. I wonder if they put his position up for tender in a proper competitive process, or whether, like a medical specialist (he thinks they price gouge too) he just named his fee?

It's important the rest of us aren't taken for a ride. Productivity and fiscal and monetary discipline are the answer to today's problems, not blame shifting.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon