Chart 3

Compiled from RBA statistical tables online

Advertisement

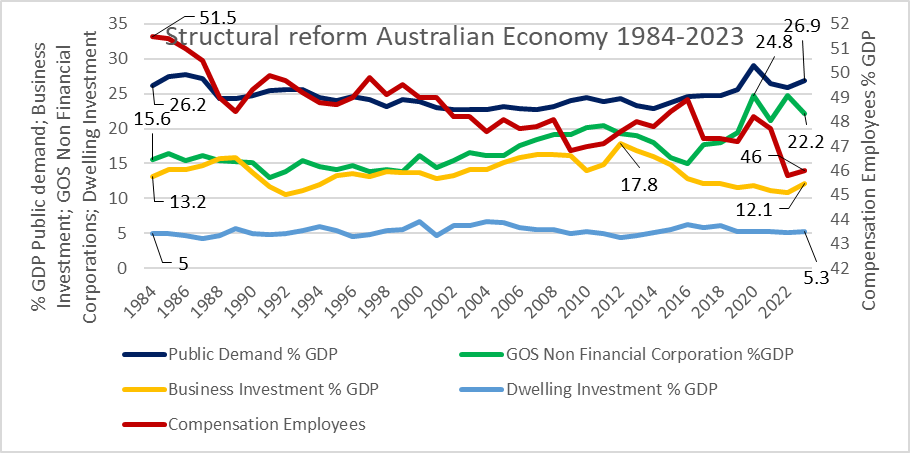

The change in sectoral contributions to GDPr are indisputable. Compensation of employees has fallen from 51.5% in 1984 to 46% in 2023.Gross operating surplus of non-financial corporations has risen from 15.6% in 1984 to peak at 24.8% in 2020. Government demand has remained relatively constant; but the income support programs during COVID are there exposed for all to see peaking in 2020. Business investment has declined from a peak of 17.8% in 2012to 12.1% in 2023. Meanwhile dwelling investment remains relatively constant from 1984 to 2023.

When Chart 3 is understood, it becomes clear that structural reform has been substantial. Media commentary from all levels seem out of touch with reality. Political commentary from all quarters appears little more than ill-informed ideology.

Applied economic policy becomes the explanation of long-term structural decline in the economy. As the RBA has been responsible for two major arms of macroeconomic policy since 1993 i.e external balance and applied monetary policy, the competence of that institution becomes the focus of attention.

Legitimate criticism of the RBA revolves around its move to supply side monetary policy based upon the economic philosophies of monetarism and general equilibrium theory. This discussion has demonstrated the short comings of supply side monetary policy which leads to the conclusion that supply side theory is nothing more than a failed economic ideology from the past.

Monetary policy division of the economy into a high-income low-income class system is unforgivable in the twenty first century. There needs to be a major economic summit to chart a way forward that will restructure the Australian economy into a more moral economic system. In the meantime, the Australian Government should reclaim its Constitutional right to control both external and internal balance. The RBA needs to return to its original role of administering monetary policy on a day-by-day basis.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

3 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon