Neoclassical heritage still has great influence-------. Its latter-day practitioners take refuge in building up more and more elaborate mathematical manipulations and get more and more annoyed at anyone asking them what it is they are supposed to be manipulating.Joan Robinson Economic Philosophy, p. 122

Chart 1

Advertisement

Compiled from RBA Statistical Tables online.

Monetary policy in Australia has come under criticism over recent months. As portrayed in the Chart 1, monetary policy appears impotent and unable to provide stability to an economy experiencing long term decline since 2007. Whilst, monetary policy has followed the CPI curve closely, the GDPr growth curve indicates the underlying economy has been in long term structural decline since the GFC in 2007. Economic dislocation over COVID shows that monetary policy offered no answers. All it could offer was to raise interest rates to address COVID inflationary pressures. Such use of monetary policy would have compounded COVID dislocation.

Post Covid, rising inflation resulted from a combination of income support programs and international supply dislocations. Being a blunt instrument, raising interest rates at a time when the underlying economy was experiencing its worst downturn since the Great Depression would have been counterproductive. This short discussion attempts to explain why monetary policy has become impotent and cannot meet the needs of the modern Australian economy.

The story begins with the election of the Labor Government in 1983 and adoption of Thatcherism based upon supply side economics. In December 1983, the newly elected Labor Treasurer deregulated the Australian Currency which then became the responsibility of the Reserve Bank of Australia. In 1985, monetary targeting was abandoned as monetary flows under the deregulated exchange rate destabilised the domestic demand for money function. In 1988, the RBA assumed the money supply endogenous which meant bank credit determined the domestic money supply. The following equation illustrates the domestic money supply.

Ms = BR + DCE

Advertisement

Ms = Money Supply

BR = Bank Reserves

DCE = Domestic Credit Expansion

Ms=Md in equilibrium i.e

In February 1990, the RBA announced the Cash Rate would become the official monetary policy instrument. The transmission mechanism for monetary policy then became the domestic overnight bank rate for interbank transactions which ultimately determines the supply price of domestic credit. In the equation above, the Cash Rate determines the price of bank credit to manage domestic credit creation .Consequently, the demand for bank credit becomes supply side determined.

In 1993, the RBA announced it would target inflationary expectations within a proposed 2% - 3% target range over a set period of time. The level of inflation was to be maintained at the equilibrium aggregate output level at which the actual rate of unemployment equalled the Non- Accelerating Inflation Rate of Unemployment or NAIRU. This measure of unemployment is sometimes referred to as the natural rate of unemployment NRU. However, there is a technical difference. NRU refers to an econometric model in which all markets clear under pure competition. NAIRU however, assumes some market imperfection; but, markets still clear. Originally the terms were used to distinguish between employment in the USA and employment within the European economic system.

The real problem with monetary policy lies not in its definitions of the labour market; but, in its underlying economic philosophy. The terms NAIRU and inflation targeting are directly identifiable with Friedman's inflation-augmented Phillips curve. Consequently, monetarism is clearly a dominant economic philosophy underwriting Australian monetary policy. The other economic philosophy which underwrites econometric modelling is neoclassical general equilibrium theory. Combined, these two economic philosophies underwrite both the New Neoclassical Synthesis and the New Keynesian Synthesis. The difference between the two synthesis revolves around a New Keynesian Synthesis additional assumption of monopolistic competition in its DSGE model.

Significant change in monetary policy emerged with the announcement that the RBA recognised the money supply being endogenous in 1988. Whilst this was consistent with global monetarism, the assumption of an endogenous money supply officially moved applied monetary policy from post War demand management to supply management of the monetary policy arm.

Supply side monetary policy dates back the 1920's and R.G. Hawtrey's monetary trade cycle theory. It is a theory from the forgotten economic philosophies of Classical, Neoclassical, Monetarism, and Austrian economics which had nothing to offer during the dislocation of the Great Depression. In 1936 Keynes released his General Theory of Employment, Interest and Money in which monetary policy is a demand side policy arm.

In February 1990, the RBA announced that the Cash Rate would be the official policy instrument. This announcement identified the supply side monetary policy instrument that would influence the price of bank credit. From that point onwards, if a demand side problem arose, then monetary policy had to firstly adjust the supply side price of credit consistent with monetary policy stance. Then the policy stance must work its way through the transmission mechanism of the banking system to influence the demand for credit. By influencing the price of credit to industry, aggregate demand response influences the demand for labour and hence the unemployment rate. This of course is a convoluted application of early nineteenth century Say's Law of Markets interpreted by Professor Pigou in 1926

As monetary policy is concerned with inflation measured in a basket of goods, an important question becomes what happens to prices not measured in the CPI basket of goods particularly in asset markets?

Negative gearing provides an attractive policy option for two obvious groups: high income earners and lowly encumbered middle-income groups. As interest rates rise, these groups can utilise negative gearing taxation advantage to minimise tax imposts whilst building an asset wealth portfolio. The DCE component of the domestic money supply increases to meet the rising demand for bank credit to purchase assets. Asset inflation then becomes the unrecognised outcome of supply side monetary policy. In a modern densely populated urbanised economy, home ownership for rental income becomes a prime asset target.

The flow on from asset accrual affects living standards of low-income groups as rentals rise to offset mortgage repayments of asset owners. Low income groups face financial pressure as disposable incomes must manage increases in home mortgages; and or, rising rental payments. The current crisis of homelessness can be attributed to supply side monetary policy generating asset inflation in the residential home market forcing low-income groups into tents and cars for shelter.

Asset inflation destroys the social fabric of society by structuring a wealth-based class system. The favoured group of high incomes build wealth whilst the remainder low-income groups endure declining living standards as monetary policy does its work. In the real world, supply side monetary policy directed to bringing actual unemployment equal to NAIRU is devoid of any semblance of morality as it implies enlightened self-interest always operates in the public interest. Consequently, the economy divides into a two-class system comprising an asset wealthy class and a lower income underclass. The impact of asset inflation on the social fabric must be profound as it highlights that enlightened self-interest does not always serve the public interest.

Resentment within the lower income strata would be expected to increase social discontent and fuel a rising crime rate. Moreover, youth resentment would be expected to be high generating youth rebellion and rising crime levels. Resentment of a two-class system would be expected to fuel activism in other social areas of society as the underclass seeks a political voice to express discontent with a failing economic system.

2 Empirical Analysis

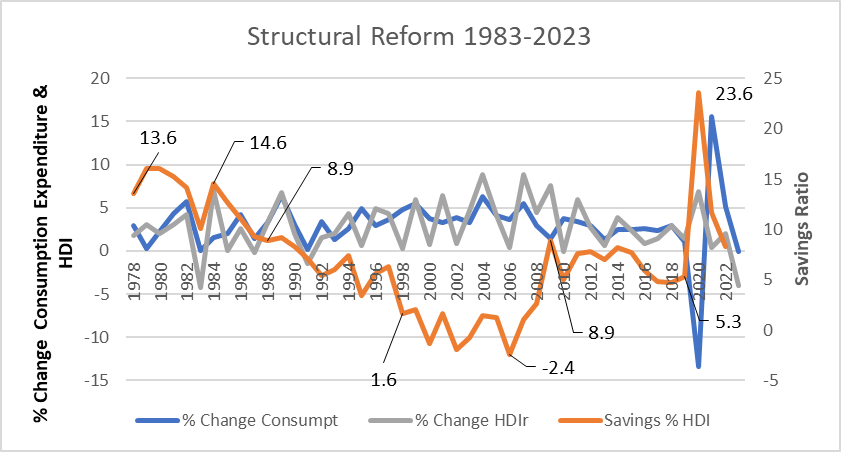

Chart 2 below provides empirical evidence of the failure of supply side economics. The transition to supply side monetary policy is readily identifiable post 1988 when the savings ratio collapses to support Household disposable income and consumption. The other two curves empirically identify what happened to Household Disposable Income as a percentage of GDP and the percentage change in consumption expenditure as a percentage of GDP.

Chart 2

Compiled from RBA statistical tables online.

Supply side monetary policy began in 1988 when the RBA announced it was assuming an endogenous money supply. In February 1990, supply side monetary policy became operational with the announcement that the Cash rate would be the monetary policy instrument.

Look closely at the observed variables. The behaviour of the Savings curve holds the key. In 1984 the savings ratio was 14.6% of household disposable income.in 1988 when monetary policy moved to supply management of bank credit, the savings ration had fallen to 8.9%. It bottoms out in 2006 at-2.4%. the GFC in 2007 forced a change in household behaviour and the savings ration begins to rise to peak at 8.9% in 2009. By 2019 the Savings Ratio stood at 5.3%. The combination of household support programs and uncertainty lifts the household savings ratio to a peak of 23.6% in 2020. By 2023, the savings ratio had collapsed to 2.8%.

Percentage change in Household Disposable Income curve is 7.1% in 1984. The curve falls to 3.3% in 1988 and continues to bott om out at 0.4% in 2006. By 2010, the rate of change in HDI curve falls to 0.1%. By 2018, percentage change in household disposable income stood at 2.9%. The impact of income support programs are clearly visible in the rate of change in household income rising to 6.7% in 2020. However, by 2023, household income contracts -2.6%; and the RBA wants to raise interest rates!

The other important curve is the percentage change in consumption. In 1984, consumption expenditure was growing at the rate of 1.6%. By 1988, growth in consumption expenditure had risen to 3.3%. By 2006 expenditure of consumption rose 3.6%; but the onset of the GFC induced a reduction in consumption growth to 1.4%. Just prior to Covid in 2018, growth in consumption expenditure had risen 5%. However, COVID changed consumer behaviour. In 2020, consumption expenditure contracted -13.4%. Given household support programs, consumption expenditure recovered by 15.6% in 2021 to settle at .7% in 3023.

Monetary response to the COVID pandemic and international supply dislocation from both COVID and armed conflict indicates that supply side monetary policy once again has nothing to offer in terms of economic management. Media coverage over Christmas 2023 of unprecedented numbers of people seeking help and assistance from various charities should sharpen the contemporary debate and bring focus upon the morality of not only contemporary monetary policy but also macroeconomic policy in general.

Contemporary public debate focuses upon environmental and other social policy issues whilst ignoring the plight of a growing percentage of low to middle income groups struggling to provide for themselves and their families. The growing number of homeless people living in tents and cars this Christmas does not reflect well on the dominance of social policy activism in the public debate. The morality of contemporary economic management that talks about abstract balance sheets of homeowners and businesses should be the focus of public concern and anger.

Conclusions

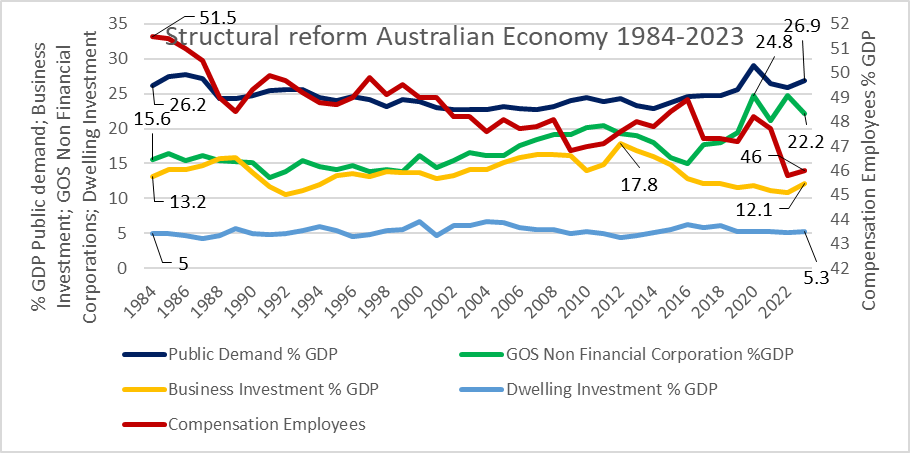

Supply side economics was introduced into Australia as Thatcherism by the Hawke Government in 1983. The objective was to join an international return to the economics of the Classical era free market economics. Successive governments of all persuasions have continued supply side economic principles without questioning impacts upon different groups in society. Chart 3 shows empirically the outcome of supply side reforms of the Australian economy.

Chart 3

Compiled from RBA statistical tables online

The change in sectoral contributions to GDPr are indisputable. Compensation of employees has fallen from 51.5% in 1984 to 46% in 2023.Gross operating surplus of non-financial corporations has risen from 15.6% in 1984 to peak at 24.8% in 2020. Government demand has remained relatively constant; but the income support programs during COVID are there exposed for all to see peaking in 2020. Business investment has declined from a peak of 17.8% in 2012to 12.1% in 2023. Meanwhile dwelling investment remains relatively constant from 1984 to 2023.

When Chart 3 is understood, it becomes clear that structural reform has been substantial. Media commentary from all levels seem out of touch with reality. Political commentary from all quarters appears little more than ill-informed ideology.

Applied economic policy becomes the explanation of long-term structural decline in the economy. As the RBA has been responsible for two major arms of macroeconomic policy since 1993 i.e external balance and applied monetary policy, the competence of that institution becomes the focus of attention.

Legitimate criticism of the RBA revolves around its move to supply side monetary policy based upon the economic philosophies of monetarism and general equilibrium theory. This discussion has demonstrated the short comings of supply side monetary policy which leads to the conclusion that supply side theory is nothing more than a failed economic ideology from the past.

Monetary policy division of the economy into a high-income low-income class system is unforgivable in the twenty first century. There needs to be a major economic summit to chart a way forward that will restructure the Australian economy into a more moral economic system. In the meantime, the Australian Government should reclaim its Constitutional right to control both external and internal balance. The RBA needs to return to its original role of administering monetary policy on a day-by-day basis.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon