Home buyers and businesses are suffering sticker shock as the Reserve Bank of Australia (RBA) lifted the official cash rate from 0.1 percent to 3.35 percent in the course of the nine months since April 2022. But they should probably be thinking of rates of this level as the "new normal."

Assuming lenders pass the whole rate increase, payments on the average floating rate home loan of $599,992 (US$416,000) have increased by $19,499.74 per annum.

If the mortgage is being paid by a couple, each earning average income, then repayments go from 28 percent of before-tax income, to 39 percent. On an after-tax basis, this is 35 percent to 49 percent.

Advertisement

This is obviously unsustainable for a lot of homeowners.

Punters are not happy. The ANZ-Roy Morgan consumer confidence index bounced slightly in January and hit 86.8. It is slightly higher than at the end of last year but still amongst the lowest levels measured by the index.

It has only ever been lower once-at the beginning of the pandemic-and was slightly higher even at the depths of the global financial crisis.

House prices have also declined by around 8.4 percent, the largest decline on record.

Government ministers are showing signs of panic, with Assistant Treasurer Stephen Jones claiming: "if this is not the last, it's near the last of the rate rises."

But what does the governor of the Reserve Bank have in mind?

Advertisement

Australia is facing a similar situation to what they encountered in 1973, the second year of the Whitlam government, with the "Arab oil crisis" forcing-up energy costs against an expanding economy driven by massively increased government largesse.

The world, and Australia more than most, entered into a period of "stagflation" where economies languished, but prices rose rapidly. It was driven partly by supply-side constraints and in part by expectations where unions pressed for higher wages. And anticipating higher wages and inputs, businesses pre-emptively raised prices.

The economic dog chased its tail for almost a decade until 1982, with the biggest winners being highly-geared speculators.

RBA Governor Philip Lowe was 12 in 1973 and in university in 1982, so his formative years as an economist were dominated by the crisis and the solution - tight money supply and micro-economic reform.

That makes it hard to understand how he missed the current crisis, stating as late as May 2021 that he didn't expect rates to rise before 2024 despite the massive inflationary pressures being baked in by the COVID measures.

It also makes it likely that he will go harder than anyone currently thinks on interest rates because one of the lessons that were taken from the stagflation era was that interest rates were not raised early enough or quickly enough.

Having erred once, it's more likely that the governor will overreact on interest rates. Furthermore, his term ends in September and is unlikely to be renewed, so the next seven months will ultimately define his legacy and reputation.

The market consensus is for another 0.5 percent rise in rates to 3.85 percent. However, some predictions, such as one from Morgan Financial, are for cash rates to rise to as much as 4.85 percent.

Morgan's chief economist, Michael Knox, has an enviable record of forecasting and bases this figure on the current unemployment rate of 3.85 percent.

In Morgan's note on Feb. 7, the RBA board is quoted as saying: "The unemployment rate has been steady at around 3.5 percent over recent months, the lowest rate since 1974."

Morgans infers from this that the RBA sees the unemployment rate as inflationary and will act accordingly.

So government and consumers may be surprised at how high rates go. They may also be surprised at how long rates stay up.

What if a "peak" is actually more like a "plateau"?

If the strategy of the government and consumers is to use reserves to survive until we get to the other side, they may be surprised by how long they have to "hold their breath," and this will have ultimately catastrophic effects on consumer confidence.

The treasurer doesn't expect a recession, but I wouldn't be so sure.

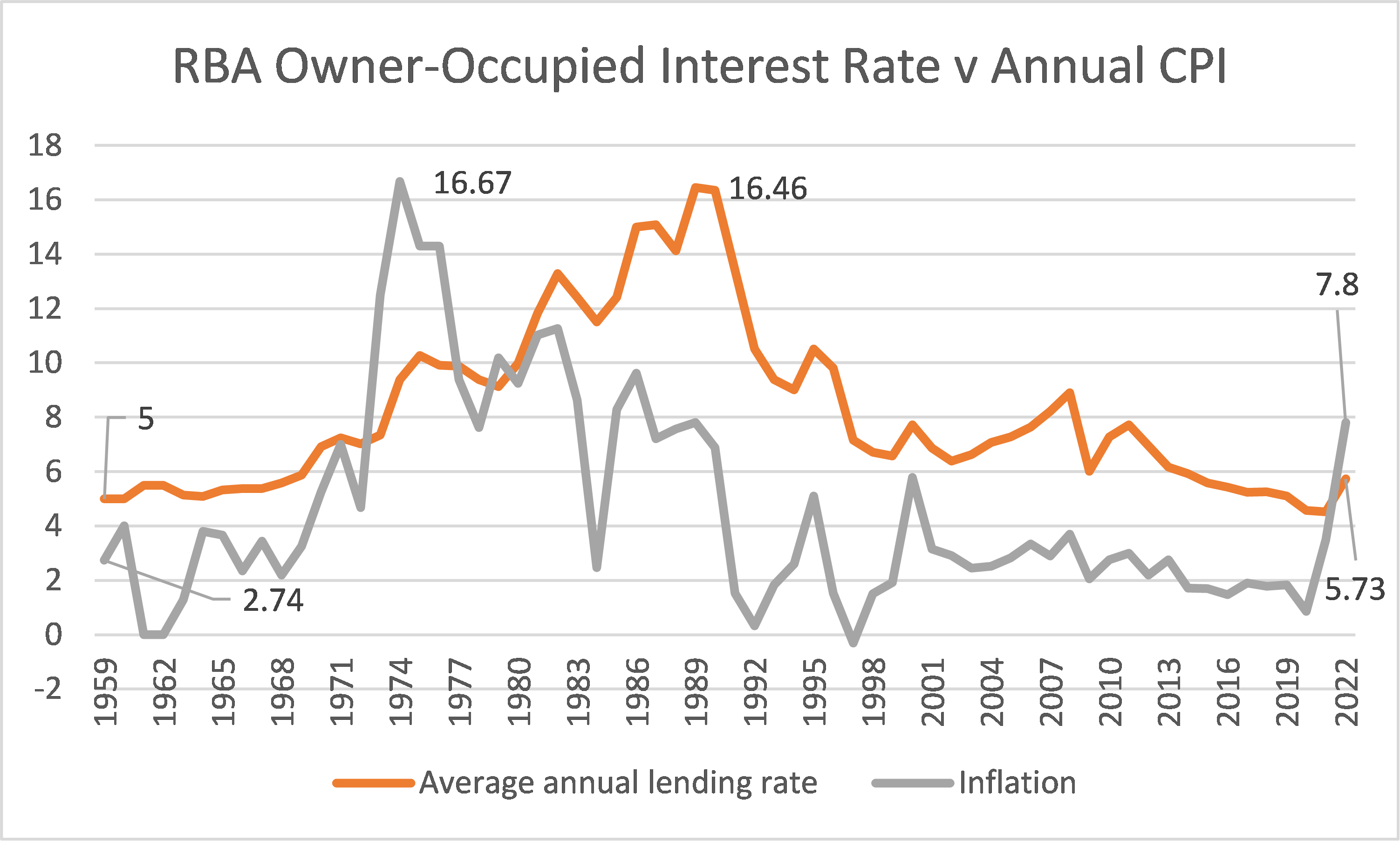

(Courtesy of Graham Young, compiled from data from the Australian Bureau of Statistics)

The graph below shows home lending rates since 1959 against inflation rates.

It shows that lending rates are almost always higher than inflation, with the exception of the 1973 to 1980 situation when inflation ran right out of control… and now.

For periods of stability and containment, interest rates are well-clear of inflation and less volatile than inflation.

The late 70s rise in rates also persisted well past a decline in inflation through to the early 90s.

That gives one clue as to where they may be heading now.

The other is given by the RBA governor, who notes he wants inflation in a band between 2 and 3 per cent. Over the period 1959 to 2022, the average gap between inflation and interest rates was 3.522 percent. That implies a long-term housing lending rate of around 6.5 percent.

The pain for the government and households is set to persist for quite some time yet.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon