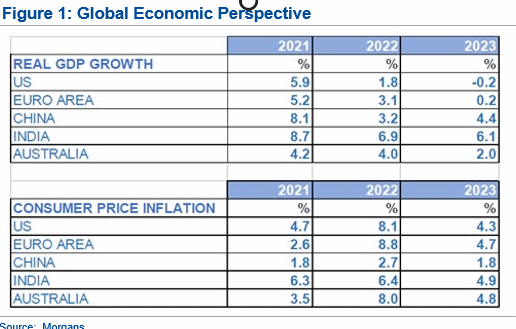

The world economy seems to be entering a shallow slowdown as we move into 2023. We think that after 1.8% growth in 2022, the US will record a slightly negative -0.2% GDP growth in 2023. The reason for this slowdown is continuing rate increases by the Federal Reserve.

The Euro Area, after 3.1% growth in 2022, should decline to only 0.2% growth in 2023. Germany and Italy should both suffer negative GDP number in 2023. The United Kingdom, which is no longer in the European Union, should also suffer a small negative GDP number.

Advertisement

The Chinese economy, which has struggled through 2022 with much of its economy in COVID shutdown, should grow by only 3.2% in 2022. COVID is not China's only problem. The slowing growth rate of an aging workforce means that the structural growth rate that China can produce in terms of its national income, is slowing. By the end of this decade, the Chinese workforce should actually begin to decline. This means that Chinese growth will be determined entirely by productivity growth. China will enter a period of slow Japanese-like growth rates.

The economy that replaces China as the major world growth economy will be India. The growth of the Indian workforce will continue to be strong for decades ahead. After 6.9% growth in 2022, the Indian economy should grow by 6.1% in 2023. These high Indian growth rates are sustainable through this decade and the next. This year, India moved from being the world's sixth largest economy, to being the fifth largest economy. By 2050, India could become the world's largest economy.

After 4% growth in 2022, the Australian economy should grow by 2.0% in 2023. The Australian economy will continue to grow solidly, even as other major developed economies slow towards zero. Australian growth, while other countries are in recession, is supported by our bipartisan skilled immigration program.

The reason that Central Banks are increasing interest rates to slow the world economy, is the problem of high inflation. This inflation was not caused by Central Banks. This inflation was caused by the enormous expansions of fiscal deficits in 2020 at the beginning of the pandemic. Politicians, particularly those in the US, seemed unsatisfied by merely filling the need to support their economies during the pandemic shutdown. They also found the need to fill the pockets of their political supporters with generous programs.

The result of this was a dramatic expansion of budget deficits, especially in the United States. The US budget deficit in 2020 rose to 15.9% of US GDP. This budget deficit was the largest budget deficit since WWII. This was followed by a further budget deficit in 2021 of 11.1% of GDP. Unfortunately, the US economy did not have enough excess capacity to grow as rapidly as this demand suggested. The excess stimulus then spilled directly into high inflation. This is the high inflation that has burdened the whole of the world economy through 2022.

Inflation should peak in the US at 8.1% in 2022 before falling to 4.3% in 2023. Inflation in the Euro Area should peak at 8.8% in 2022, before falling to 4.7% in 2023. Australian inflation should peak at 8.0% in 2022 before falling to 4.8% in 2023. All of these countries expect inflation to fall to 3% or lower by the end of 2024.

Advertisement

China, with a softening economy, should have inflation of only 2.7% in 2022, easing to 1.8% in 2023. Rapidly growth India, with a 4% inflation target, should have 6.4% inflation in 2022 and 4.9% in 2023. These inflation levels are not a problem within the context of the Indian economy.

Inflation and financial markets

Rising inflation has caused problems for financial markets because rising inflation leads to rising bond yields. Rising bond yields put downward pressure on stockmarket prices, even if earnings are stable. This is the circumstance which gave both the US and Australian stockmarkets a rough ride in calendar 2022. As we reach the end of 2022, the Australian market seems to be producing better earnings than the US market.

A decline in bond yields, which may turn out to be a counter-trend rally, has allowed a recovery in US and Australian equities since late September. Australian equities seem to be performing especially well because of superior earnings. These superior earnings seem based in the out-performance of the Australian resources sector.

Our model of the ASX200 at the end of November 2022 stood at 7370 points. As we reach the end of 2022, Australian commodity export prices, seem to have declined slightly but remain well above the peak levels achieved during the previous resources boom earlier in the century. It is likely that this out-performance of the Australian equities market, over the US equities market, can be maintained in 2023.

Staying the course

The problem we see is that Central Banks have yet to come to the end of their tightening cycle. It is entirely possible that bond markets have underestimated the willingness of Central Banks to move to higher ground. It is entirely possible that renewed increases in short rates will provoke a further sell-off in US and other treasury securities as we move into calendar 2023. This could generate further downward pressure on world equities in the first half of 2023. We will have to live through this difficult period to find what exactly Central Banks have in store.

Still, we may be confident that by the time we reach the middle of 2023, this process of Central Bank tightening will be completed. The outlook then is for falling inflation, inflation that is falling throughout calendar 2023 and 2024. This should then generate an extended rally in long term bonds. This rally in long term bonds should allow an equally long rally in US and Australian equities. It is really just a matter of staying the course until Central Banks are satisfied that they have completed their program.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon