In the beginning of the year, we started to show what we called our 'Nowcast' of the Australian economy. We were looking at swings in the level of employment in Australia and also the number of hours worked. When you get into recessions, you seem to be able to get a better reading of what's happening in the Australian economy by looking at those employment numbers first before looking at other variables. As soon as all the employment numbers are out for a quarter, we can make a reasonable estimate of what is going to happen in the GDP number.

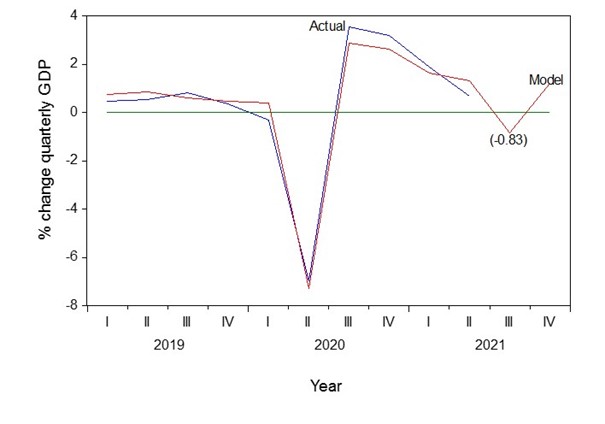

Figure 1: Australian GDP

Advertisement

Source: Morgans

In the September quarter, Australian employment fell. It fell because of shutdowns in the two largest employment states New South Wales and Victoria. Hours worked also fell, but they fell in a different pattern to employment.

It's one of the great things about the Australian economy that we have on average the highest immigration rate in the OECD. That gives us high growth in the workforce. That's important. That allows our GDP to grow more rapidly than most other countries in the OECD.

Employment in July really hadn't come off at all. In Australia there were 13.16 million people employed in July, it's an enormously large number. Employment then fell in August to 13.02 million jobs. It fell again in September to 12.88 million jobs. Then we also look at the number of hours worked. Hours worked started off at 1.78 billion hours worked in July (so somebody out there is counting every hour you do at work, or at least estimating it), and it fell very sharply in August to 1.71 billion hours. In September it seemed to pick up again. Perhaps working from home or some areas of the economy opened up, particularly in states that weren't shut down. The number of hours worked rose slightly in September to 1.73 billion. By the time you got to September growth was picking up.

Now there's been some very pessimistic estimates of what that did to GDP. Still we must remember that the amount of capital in the economy is rising relative to the number of people in jobs. Output doesn't actually have to go down as much as the number of employed people or even the number of hours worked. The difference between output and employment is productivity.

We look at the period of the pandemic since the middle of 2019. We can see our model in Figure 1. We can see that this model based on hours worked and employment generates a pretty good explanation of what happens in GDP growth. At the end of 2020, GDP rises as employment growth goes up. We think that with the fall of employment last quarter and the fall in hours worked, the GDP will come in about minus 0.83 of a percent. That's a bit better than what we estimated after the August numbers. The reason our estimate has improved is we've had that little improvement in hours worked.

Advertisement

Where does that take us for the full period? Many commentators expect not much of a recovery in the final quarter of this year. We think we will have a pretty good recovery in the final quarter of this year, and you can already see that in terms of job ads in New South Wales. So I think that after that negative 0.8 of a percent for GDP in the third quarter we will recover about 1.2% for GDP in the fourth quarter. Now that's not equal to the strongest recovery in previous quarters, but equal to about the second strongest recovery in previous quarters. What that does is that it gives us growth for the full year 2021 of 3.5%. In 2022, GDP growth slows as we go forward to 1 percent increase in growth in the first quarter of next year, then cuts down to 0.9% growth.

I think in the middle of the year I was estimating that with strong US growth we're to get about 5.3% growth in Australia. We've lost about 2% growth for the year as a result of the shutdowns. Still, growth is above the average of what it would normally be in the Australian economy. That year on year growth actually accelerates for the next few quarters. When we get to the third quarter of next year, growth for the full year to the third quarter of 2022 is 5%. That is really strong.

Now there are some major banks out there that are estimating growth of 7% for the full year, next year. I don't get as good a number as that for next year because I think we have a faster bounce in the final quarter of this year. That's really the difference between those two views.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

2 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon