A man should look for what is, and not for what he thinks should be. Albert Einstein

In Saturday's Sydney Morning Herald and The Age, "PM Must spend to kick-start slowing economy, says RBA", the Philip Lowe, the Reserve Bank Governor called for a major new spending program on infrastructure including rail, bridges and roads across Australia, in direct opposition to the views of the Federal Government. He argued that more public spending, outside metro Sydney and Melbourne (where there is limited capacity), has the potential to maintain and improve infrastructure, while pouring the government's gravy far and wide.

The Governor added that the US-China trade dispute could harm employment because of the uncertainty it generates in the business community, but if the dispute is resolved soon, it may lead to a speedy turnaround in the world economy, presumably in Australia too. The turnaround would be seen clearly in a retreat from business' underinvestment.

Advertisement

By splashing the Governor's views on the front page of the papers as well as promoting him via a flattering profile in their respective Good Weekend magazines, Nine Entertainment must believe that either the RBA is advancing sound economic policy or very controversial policy. Sadly nowhere in the promotion was there mention of the RBA's failed attempts to jump start the economy by shaving interest rates.

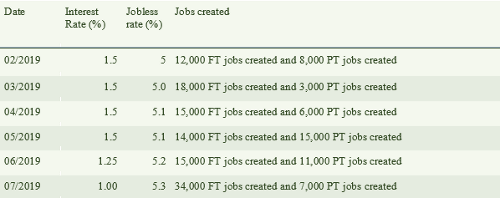

Over the last few months the RBA has lowered interest rates with the aim of raising demand by consumers; increasing investment by firms and lowering the number of those lining up at Centrelink for unemployment benefits. The table below shows just how unsuccessful the RBA has been:

Source: ABS trend estimates

As can be seen, while the cash rate has marched south, the jobless figures flown north. In five months 50bps were trimmed from the cash rate only to see the unemployment rate escalate from 5% to 5.3%, Not the intended result I'd wager.

The RBA's response to this unwelcome development has been to double down. Reviewing developments to date, in July explained that the latest cut of 25bp was an "easing of monetary policy [to] support employment growth and provide greater confidence that inflation will be consistent with the medium-term target".It went on: " In most advanced economies, inflation remains subdued, unemployment rates are low and wages growth has picked up".

Advertisement

In the year to 30/03/19 the RBA noted that "the main domestic uncertainty continues to be the outlook for consumption". And lamented that "unemployment is stuck above 5%". For some months now the RBA has aggitated and is now openly calling for higher wages for those in jobs and as a lure to get them to spend more and as an incentive to attract those not in jobs, into jobs.

There is no doubt that the RBA is clear about the outcome it seeks: for consumers to increase their level of demand by spending more of their wages more often. The RBA also wants businesses to soak up some of their "spare capacity" by hiring more staff, which would result put a dent in the unemployment figures.

So just what is "spare capacity"? This refers to those industries which operate below the maximum sustainable level of production - because they have underutilised land, labour and/orcapital. Theargument goes thatunused labour could be hired to mop us that spare capacity if only businesses would open their wallets a bit more (and encourage more folk into the workforce or those already working to work more.

Businesses or the economy operate with spare capacity when:

- Demand from consumers overall is low;

- Investment by businesses falls;

- Negative seasonal variations in demand don't reset themselves; and

- Productivity improvements mean that more is being produced with less inputs.

Improvements in productivity mean capacity increases for a given level of demand (but this is not the case in Australia where labour productivity fell by 1.4% in the year to 30/06/19). As for businesses not investing, the fact is that investment fell by 0.5% in the 3 months to 30/06/19. Presumably even with such a fall, there still is underutilised infrastructure gathering dust.

While the RBA has looked at various nutrients that could grow the economy, it has ignored one in particular. One that is introduced to students in ECON 100 and whose behaviour, in a free market, is understood by young and old, those learned in economics as well as those educated in the school of life.

That nutrient is the elephant in the room. His name is "minimum wage".

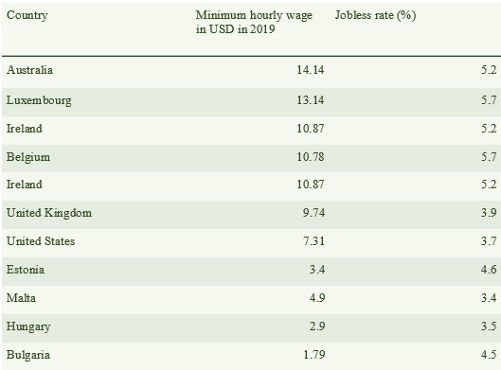

Before lamenting the relatively high jobless rates the Australian economy suffer, the RBA should admit that our minumum wage is responsible for a good many Australians parking their derrièreson the unemployment benches. Australia tops the pops when it comes to paying the highest minimum wage in the world. It can be clearly seen that the more generous the minimum wage, generally the higher the jobless rate is for a respective country.

The RBA is now arguing for a switch in economic policy to Keynesian spend and keep on spending, after realising that flogging the monetarist horse has not ponied up the expected economic results in terms of the number of jobless Australians.

Acutely aware that historic low interest rates have not enticed the business sector to invest in large infrastructure projects, the RBA now wants the public sector to carry this burden. Not content with the amount of infrastructure spending the Morrison Government is already wedded to, the RBA wants to put a rocket under the Prime Minister to turbo charge infrastructure spending, something the Prime Minister, sensibly, is resisting.

The RBA is right in its diagnosis of the economy's ills. It is right to worry about low demand and high unemployment (relative to other countries). It is also appropriately concerned about businesses not investing enough. But it is wrong in its prescription for the Federal Government, or for that matter any state or territory government, to attempt to fix this crisis by spending billions (which would have budgetary consequences) and to burden taxpayers with the superfluous risk of major infrastructure projects.

What the RBA should do is create an environment attractive enough for businesses to undertake these projects. It could do so by making it more appealing for companies to hire more and more labour. As more and more of the unemployed are hired, the numbers lining up for benefits would begin to thin.

The RBA's board is unelected. It can propose policies so out-there, that many politicians world regard as "courageous". It must propose such policies when the need arises. And the need has arisen. It cannot remain shackled to policies that may have worked in the past. It must think out of the box.

It can start by admitting that its current interest rate policy isn't working and neither will money printing, politely termed "Quantitative Easing", which has been floated in the media in recent weeks.

If the Governor's objective is higher levels of domestic demand, lower levels of unemployment and greater levels of business investment, it could do all of this by advocating publically and vigorously for a cut in the minimum wage. A cut deep enough to stimulate a steep rise in hiring, which would not only give the jobless a better image of themselves but would make available, to the private sector, the keenly priced labour required for the infrastructure projects the RBA talks about. And soon enough, those newly minted workers will have dollars to spend.

The fruits of such a policy include: the required infrastructure works will be undertaken, risks inherent in such infrastructure works will be carried solely by the private sector and the Commonwealth Budget will improve over time as less is spent on unemployment benefits as more and more jobless move into the workforce.

Simply put Governor: qui audet adipiscitur.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon