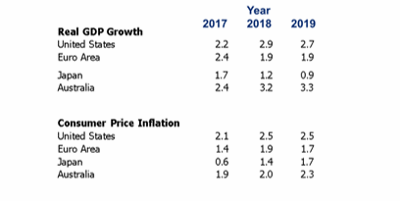

This time last year, almost nobody forecast that the US economy would be growing as strongly as it is. The expected result for this year was around 2.2% growth, falling to around 1.8% growth in 2019. This slowdown was expected to result from the gradual tightening of short term interest rates by the US Federal Reserve. Very few economists included a major surge in growth as a result of US tax cuts. Still, that major surge in growth is what has occurred.

Figure 1: Global Economic Perspective

SOURCE: Morgans

Advertisement

Instead of 2.2% growth in 2018, the US economy looks like achieving not less than 2.9% growth. Some estimates for the year, including the fourth quarter GDPNow, produced by the Federal Reserve Bank of Atlanta, suggests that GDP growth will finish this year at around 3%.

Tax cuts have increased growth in two ways. The first is that reduction in corporate taxes has allowed firms to retain more earnings to invest. The second is that cuts in personal income tax have provided workers with increased after tax earnings. This has generated an increase in labour force participation and allowed the unemployment rate to fall with no increase in inflation. Both of these effects are what economists call 'supply side effects'.

We think that these supply side effects from corporate and private tax cuts will have a long term positive effect on both US corporate investment and labour force participation for a number of US economic cycles. The result should not just be stronger than anticipated growth now, but an increase in the average growth rate of the US economy over at least the next few business cycles.

This means that US business cycles will be shorter, the average level of unemployment will be lower and real wage growth will be higher. This movement back to a stronger economy with lower inflation will generate a US economy which will be an entirely different experience than that which the US workforce has endured in recent memory.

The Euro Area

In the press conference, following the meeting of the Governing Council of the European Central Bank, the President of the ECB, Dr Mario Draghi, said that the European economy had had downside risks because of weakness of international trading partners. These downside risks appear to be receding. He estimated that growth this year in the Euro Area would be 1.9%. He thought that this might decline in 2019 to 1.7%. Our view is that growth will be a stronger than anticipated 1.9% in 2019.

Advertisement

The European Central Bank has brought an end to its program of quantitative easing at the end of December 2018. However, it still remains with a strongly expansive monetary policy. In spite of inflation now reaching the target level of around 2%, the European Central Bank deposit rate remains at -40 basis points. This means the Euro Area now has a policy short term interest rate which is -2.4% in real terms. Our view is that this provides the basis for better than anticipated expansion of the Euro Area in the year ahead.

Japan

Japan has already reached full employment. This means any growth in the Japanese economy is from increased productivity. Given this limitation, Japanese growth is surprisingly high. We think that Japanese output will grow by 1.2% in 2018. In 2019 Japanese growth should be 0.9%.

After a number of years of effort, Japan is also achieving a modest level of inflation. We think that CPI inflation in Japan will grow by 1.4% in calendar 2018. This should rise slightly to 1.7% in 2019. Japanese inflation is still below its targeted level of 2.0%. Although this inflation target has been in place since 2013, the target level of inflation has never yet been achieved. However, positive inflation in Japan is reducing real interest rates. This provides further support for growth in the Japanese economy.

Australia

In 2017, Australia produced a through the year growth of 2.4%. Although this was a healthy performance by the standard of other wealthy economies, it was below Australia's long term performance. An increase in the terms of trade during 2017 produced stronger growth in the Australian economy in 2018. We think that the Australian economy will grow by 3.2% in 2018. This growth should accelerate to 3.3% in 2019.

In spite of a better economic performance in 2018, inflation is likely to rise by only 2.0%. We think it will rise by 2.3% in 2019. This low level of inflation is brought about by Australian unemployment being above the natural rate of unemployment of 5%. This means that unemployment has not fallen to a level where a tightness in the labour market will generate upward pressure in real wages.

Only when real wages begin to increase will this put upward pressure on inflation. Only when this inflation rises toward the upper end of the RBA range of 2% to 3% will the RBA react by increasing interest rates. We are firmly of the belief that there will be no increases in Australian interest rates in calendar 2019.

Figure 2: Asian Economic Perspective

SOURCE: Morgans

China

Chinese economic growth in 2018 was marked by a dramatic acceleration in the manufacture of steel. Chinese steel production rose to an all time record high of 81.42 million tonnes per month in July 2018. This meant that production was up by slightly more than 20 million tonnes per month from the level of 61.1 million tonnes per month in February 2017. This increase was the biggest annual increase in absolute terms since the expansion of Chinese steel production in 2009 which served to lift the Chinese economy out of the global recession. The Chinese economy seems now to be driven by strong domestic factors. One of these is demand for infrastructure associated with the domestic building industry. The second is the demand for infrastructure with the Belt and Road Project.

Uncertainly has prevailed over the renegotiation of the Chinese trade position with the United States. However, at the close of 2018, it is apparent that the Chinese government and the US government are making considerable efforts to come to an agreement over

trade in early 2019. We think the initial agreement will include a reduction in Chinese import tariffs on motor vehicles. This will be a great and positive step forward. However, major issues on Chinese use of US intellectual property remain to be negotiated. We think these negotiations will keep both US and Chinese negotiators busy for a few more years to come.

India

In 2017 the Indian economy had recovered from a short term slump to produce growth for the year of 7.1%. We think that the Indian economy will grow by 7.3% in 2018. This growth will be followed by slightly stronger growth of 7.4% in 2019. It is notable that in 2017, 2018 and 2019 India will have grown faster than China in each of these three years.

The reason that India is now outperforming China and will continue to outperform China is because of faster growth in the Indian labour force. The Indian labour force is on average much younger than the Chinese labour force. Its growth can continue to outstrip that of China for decades to come. In the long run of history, India will have a much larger economy than even that of China.

Indian inflation was 3.6% in 2017, we believe this will rise to 5.1% in 2018 before falling to 3.9% in 2019. The inflation target maintained by the Reserve Bank of India is 4.0%. A rise above that level produces a rise in Indian interest rates which then puts downward pressure on Indian inflation in the following year. This stability of the inflation target will do much to support an increasing international market in Indian debt over coming years.

Indonesia

Australians don't look closely enough at the healthy economic performance of Australia's nearest neighbour. The Indonesian economy grew by 5.0% in 2017. We think it will grow by 5.1% in 2018 and 5.1% again in 2019. With this kind of sustained growth rate, Indonesia is expected to become a G20 economy in the decade of 2020s. Our nearest neighbour will become much more influential in coming years.

Indonesian inflation appears to have stabilized at the level not far below that of India. Indonesian inflation was 3.8% in 2017. We think Indonesia will have an inflation rate of 3.6% in 2018 and 4.0% in 2019.

Financial Markets

The closing months of 2018 have seen a sell off of US equities which has in turn generated a correction in the Australian equities market. We think the selloff in US equities has been the result of a slowdown in US earnings growth as the positive effect of corporate tax cuts begins to remove itself from the momentum in US earnings.

We think that the fair value for the S&P500 is now 2768 points. This is 166 points higher than the level of the S&P500 on 17 December of 2602 points. We believe that the S&P500 can sustain a rally back to fair value in the early months of 2019.

We think that fair value for the ASX200 is now 5962 points. This is 375 points higher than the level of the ASX200 on 17 December of 5587 points. This means that the ASX200 is some 375 points below fair value. We also believe that the ASX200 can sustain a rally back to fair value in the early months of 2019.

Conclusion

The world economy will continue to produce healthy growth in 2019. We are ending 2018 with equities markets that are undervalued both in the US and in Australia. 2019 has the capacity to produce a year both in the economy and in financial markets that is better than we expect.

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon