On 26 September, the Federal Reserve finished a two-day meeting. At the end of that, they released a statement in which they increased Fed Funds rate by 25 basis points. The upper end of the limit of the Fed Funds rate rose to 225 basis points.

What that really leads you to is what the Fed calls "the effective Fed Funds rate". The effective Fed Funds rate is usually around about 7 basis points lower than the top level so we will wind up with a Fed Funds rate moving from about 193 basis points to 218 basis points.

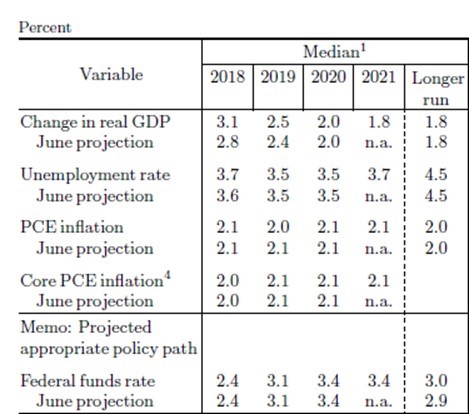

I was most interested in the Summary of Economic Projections which is taken from the estimates of all of the Fed Presidents of the individual Reserve Banks like the St Louis Fed and the Dallas Fed, in addition to the members of the Open Market Committee of the Federal Reserve.

Advertisement

Figure 1: Summary of Economic Projection

This is where you get the best estimate of what the Fed actually thinks. We see the outlook contained in the Summary of Economic Projection, in Table 1. Here we see the Fed Outlook for the September meeting together with the Fed Outlook at the June meeting.

The most remarkable change to me was the upgrading of growth estimate for the US economy this year from 2.8% to 3.1%. My own estimate that I have been showing for the last month is 2.9%. This is the first time that I can remember in the last four years that the Fed's estimate growth has been higher than my own. Hey, somebody is more optimistic than I am about the US economy.

The Fed slightly increased their estimate for next year from 2.4% growth to 2.5% growth, but growth slows to 2% year after 1.8% after that. That's what economists call a "soft landing" in which GDP growth slows but unemployment goes up. Still, you don't actually have a recession. Another phrase that many US business economists use is for that is a "growth recession". Over the years I've tended to refer to that "growth recession" myself.

Because growth is higher in their estimate, unemployment is lower. The Fed now sees unemployment falling next year to 3.5% and 3.5% the year after. The other thing that declines is inflation. In the June estimates they thought that headline inflation (this is PCE inflation or personal consumption deflator), for next year would be 2.1%% and now they've moved that down from 2.1% in June to 2% now. The reason is because oil prices will stabilise where they are and that inflation effects from the kick in oil price won't be present in a year's time, so what we get with this are "base effects".

Advertisement

The European Central Bank says the same thing and that contributes to their estimate of slightly lower inflation. We disagree with that. We think the oil price will be significant higher next year and the year after. For that reason, this headline inflation number is going be higher than the Fed thinks. Their core inflation estimates don't change at all. They think the core inflation this year will be 2.1%, next year 2.1%, the year after that 2.1%. Since their inflation target is 2% that is a pretty good result for them.

The one thing that was really interesting that the Fed didn't change was their future guidance for where the Fed funds rate is going. Exactly as at the previous meeting, they thought that would be four rate hikes this year. This means we have got one more coming in December. They thought there would be three rate hikes next year, which is exactly what they thought in June. When those three rate hikes happen, I guess it will be the first three quarters of next year and one rate hike the year after. This brings the Fed funds rate to a final peak of 3.4%.

A couple of really interesting questions were asked of Chairman Powell from the media that was present. One was "these are amazing figures; how can you be confident that the inflation will be so low in the future? Nothing like this has happened since the 1960's?" Powell suggested that's the way the data is moving. The data was the best since the 1960's. Powell thought that there is a higher labour force participation than was anticipated.

This article ws first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

6 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon