Recently I made a series of presentations in Sydney and Melbourne. As is my custom when I do these presentations, I try to say a few outrageous things.

What surprised me was that the forecast that I thought was most outrageous was the one that my fund manager audience thought was the most likely. This forecast was that US and Australian ten year bond yields would go to 4%.

The argument that bond yields, particularly US bond yields, will go to 4% is really easy to make.

Advertisement

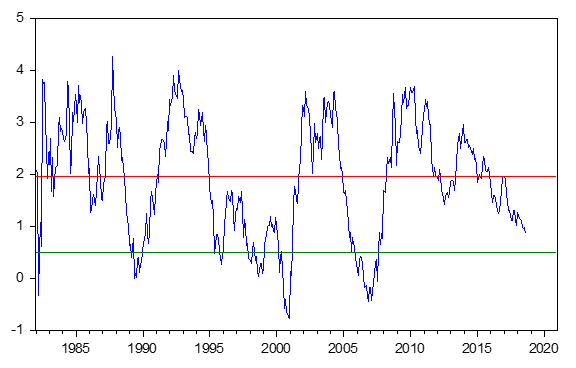

Figure 1: US Yield Curve (US 10 Year Bond Yields minus 90 Day Bill Yields)

In figure 1 above, we look at the US yield curve since January 1982. In the 35 plus years since that time, the US yield curve has varied in a wide arc, but over each business cycle, US 10 yield bond yields are an average of almost exactly 2.0 % higher than 90 day US treasury yields.

The actual numbers are that over that full period of 35 some years, US 10 year bond yields have been an average 1.91% above US 90 day treasury bill yields. The median of this difference is 1.97%. Let's say 2.0% is pretty close.

The Fed tells us that right now on 13 September, US 90 day treasury bills are trading at 2.11%. The "effective" Fed funds rate is 19 basis points lower at 1.92%. This means that if the US yield curve was right now at its average long term level, the 10 year bond yields would be the sum of 2.11% (90 day treasury bill yields) plus 1.91%(the average yield curve) leading to a total of 4.02%. This means that if the Fed funds rate were to stay exactly where it is now over the rest of the business cycle, then we would expect US 10 year bonds to rise to a yield of 4.02 % by the end of the business cycle.

But wait there's more!!

Advertisement

The Federal Reserve, in its Summary of Economic Projections released in June 2018, says that it expects that the Fed Funds rate for this business cycle to peak at 3.4% some time in 2020.

What would this mean for bond yields? Well we observe that right now US treasury yields right now are 19 basis points higher than the Fed Funds rate. By 2020 that would take US 90 day treasury yields to 3.4% plus 19 basis points or 3.59%. When we add the average long term yield curve of 1.91% to this, we get US ten yield bond yields at the end of the business cycle of 5.5%.

This means we can expect that if the Fed keeps tightening the way they think they will, then by the end of this business cycle the US ten year bond yield should rise to 5.5%.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

1 post so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon