The period from 2012 to 2015 was Australia's 'dog days'. Our 'dog days' were when declining commodity prices led to a decline in the terms of trade. This decline in the terms of trade led to low nominal GDP growth. Low nominal GDP growth put tax revenue under great pressure. This meant expenditure needed to be tightly controlled to stop the budget balance blowing out.

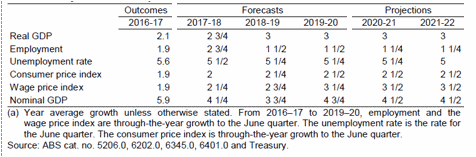

Figure 1: Major economic parameters

Advertisement

SOURCE: Budget Paper No 1, Table 2, Page 1-10

In Figure 1 above, we see the outlook for the Australian economy shown on Budget Paper No 1, Table 2, page 1-10. What is interesting here is the bottom line. That bottom line is nominal GDP. In previous commentary, we have noted that nominal GDP growth in our 'dog days' from 2012 to 2015 was really only around 2%. Nominal GDP is how wages are paid which meant that wage growth was pretty miserable. Nominal GDP is also how corporate profits are paid. This also meant that corporate profits were pretty miserable.

Nominal GDP (as shown in Figure 1) increased from around about the 2% figure in the previous three years to 5.9% in 2016-2017. This figure also shows that nominal GDP is expected to rise by 4.25% in 2017-2018. They expect it to increase by 3.75% in 2018-2019 and then 4.75% in 2019-2020. In the two years after that, nominal GDP continues to grow at 4.5%. The recovery in nominal GDP rescues Australia from its 'dog days'. Faster nominal GDP growth rescues us from the misery of that period. It also means that tax revenues are now rising at a pace where governments can fund things like individual tax cuts as long as they keep a steady line on budget expenditure.

We note from the Figure above that the government forecasts consumer price inflation to never rise above 2.5% and unemployment to never fall below 5%. Should that scenario actually occur, the Reserve Bank need not bother going to work again until sometime in late 2022.

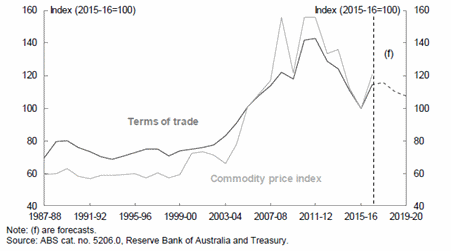

Figure 2: Commodity prices and the terms of trade

Advertisement

SOURCE: Budget Paper No 1, Chart 8, Page 2-24

In Figure 2, we see the reason that nominal GDP recovered. The real cause of our 'dog day' period was the decline in commodity prices and the decline in the Australian terms of trade from 2012 until 2015. It is this decline which inflicted low nominal GDP growth on the Australian economy.

Since the beginning of 2016, we have seen a sharp recovery in commodity prices. The RBA index of our export commodity prices has risen more than 20%. The terms of trade has had a similar but slightly smaller recovery. The Australian Treasury thinks that the terms of trade will drift down from now on. We have a whole lot of reasons including the expanding US budget deficit for thinking that Australian export commodity prices are going to be stable or continue to rise.

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

4 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon