Global financial markets are keenly interested in China's short-term economic direction and policy choices. American policy should look farther. If China chooses to try to stimulate its economy in the second half of the year, even if successful, it will only exacerbate a more pressing long-term challenge.

This challenge in part takes the form of too much money. While attention is focused on when the People's Republic of China (PRC) might catch the U.S. in terms of GDP, it has already passed the U.S. on some measures of its monetary base. Such high liquidity typically precedes periods of stagnation or even outright economic contraction. It is one of the surer reasons for anticipating that China's true economic growth might slow sharply, a possibility that has clear implications for American policy.

Moreover, excess Chinese liquidity has already had an impact in the U.S. The two economies are linked by Beijing's chosen balance-of-payments rules, which tie the yuan to the dollar and compel the PRC to hold excess reserves in American bonds. The U.S. has its own money supply management challenges, and communication between the two countries' monetary authorities will be valuable.

Advertisement

Not for All the Money in China

There are many different ways to measure the supply of money. There are also pronounced differences in national monetary systems, which cause natural differences among economies. For a large economy, the PRC is immature financially, so that more capital stays within the banking system. This is a well-recognized long-term problem.

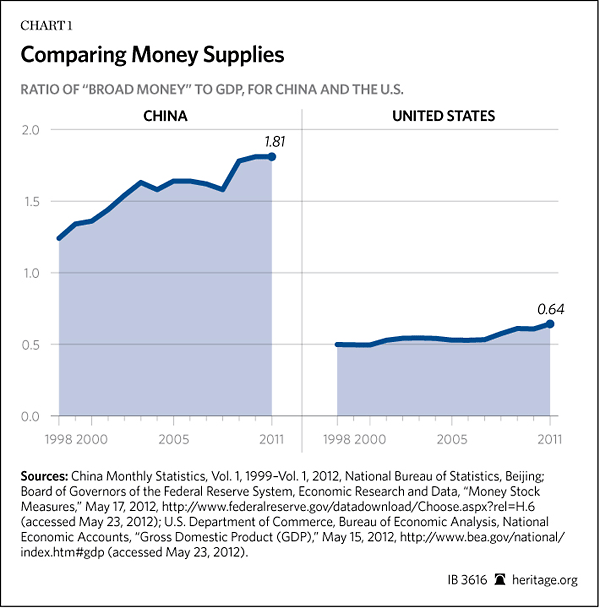

One manifestation of the problem is a comparatively high ratio of broad money M2 (currency in circulation plus demand and time deposits) to GDP. China is well above the global average on this measure, while a somewhat similar economy in Brazil is well below. Nearly all of the countries that have higher M2/GDP ratios than China are in Europe, which, in light of recent developments, is not reassuring.

More importantly, the ratio for the PRC is not only high but has been rising steadily. Since the financial crisis, a number of countries have rising liquidity, including the U.S. However, those countries with both high and clearly rising liquidity (Spain, for example) are a small and unhealthy bunch. This is not good company for China to be keeping.

The U.S. is only one point of comparison, but it is an instructive one. In 1998, China's M2was 70 percent smaller than America's. In 2011, it was 40 percent larger. While Chinese GDP expanded greatly in that period, it was still only half of American GDP at the end of last year. Yet the PRC had $3.8 trillion more in broad money supply sloshing around.

Advertisement

Measurements of leveraging show roughly similar problems. China's dependence on bank loans for financing intensified with the lending explosion in 2009. In 1998, loan volume was 102 percent of GDP. By 2008, it had only inched higher to 106 percent of GDP. Just three years later, though, it had jumped to 123 percent of GDP. More comprehensive measures of credit show still higher figures and steeper climbs.

What Happens Next?

There is plenty of discussion at present about short-term weakness in the Chinese economy and whether additional stimulus is the right response. The longer term is clear: On its present policy path, the effective stimulus Beijing can apply through monetary policy will continue to decline.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

4 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon