There are, arguably, three great crises today:

I say arguably, because people do dispute them. Against climate scientists warning of Global Warming stands an army of sceptics; against geologists warning that oil production will peak stand those arguing we will always find more oil.

Advertisement

The economic crisis is disputed too, but in three crucially different ways.

Firstly, no-one disputes its existence, since it has already happened. The dispute is over whether it is behind us (so that Europe's woes are a new phenomenon), or continuing. Secondly, whereas in the first two crises, the ordained experts warn of crises while non-experts dispute their claims, in economics, rebel economists warned of the crisis long before it happened (Bezemer 2009) while leading academic (Blanchard 2008) and professional economists (Bernanke 2004; Council of Europe 2007) foresaw a prosperous future.

Thirdly, if the first two crises do in fact occur, they will happen because the world ignored the advice of the experts, by allowing carbon dioxide levels to rise, and depleting oil reserves exponentially despite now almost ancient warnings of impending catastrophes (Keeling 1958; Hubbert 1956). The economic crisis, however, occurred because the world followed the advice of the experts: politicians deregulated financial markets, aspired to run budget surpluses, and devised treaties like Maastricht on the advice of economists that the economy would perform better as a result.

Instead, we're embroiled in an intractable downturn, and politicians have passed laws that wind back some of the deregulation that economists championed. Yet the economists who failed to see this crisis coming now express bewilderment as to "why this slower pace of growth is persisting" (Bernanke June 22nd 2011).

This bizarre state of affairs should alert the public to a profound paradox: the economists who dominate the profession are not experts on the economy at all. Instead, they are believers in a false model of the economy that has held sway despite two great economic crises-the Great Depression and our current predicament-because its arguments are superficially appealing, and compelling to those who learn them when they are impressionable young students.

This is why I wrote Debunking Economics- the first edition of which was published in 2001, the second of which has just been released (it is currently one of the top selling economics books in the UK). In it I explain the logical and empirical flaws in the "Neoclassical" approach, some of which have been known since the 1920s. Collectively, they utterly invalidate Neoclassical economics, yet before this crisis, it was so dominant that most economists thought that it was "economics"-that there was no alternative method to analyse the economy.

Advertisement

Not only are there numerous alternatives, but those emanating from Fisher, Keynes (who has been almost criminally misinterpreted by Neoclassical economists), Minsky and some Austrian economists (including not just Hayek but also Schumpeter) enabled non-Neoclassical economists like myself, Peter Schiff, Ann Pettifor, Michael Hudson and others to predict that this crisis would occur, and that it would dwarf any downturn since WWII.

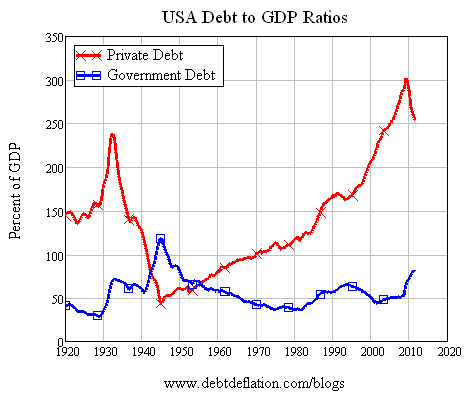

My economic model extends Minsky's "Financial Instability Hypothesis", and it generates chaotic dynamics that led me to warn against seeing an extended period of economic tranquillity "as anything other than a lull before the storm" (Keen 1995). In 2005, I became convinced that the rate of growth of private debt was unsustainable, so that a huge economic crisis would erupt simply when its growth rate slowed, as it did in 2008.

Figure : US Debt to GDP Ratio from 1920 till now

Now that private debt is falling relative to GDP, deleveraging by the private sector dominates half-hearted government stimulus packages, so that high unemployment persists years after the recession was formally declared to be over by the NBER. The crisis will continue until private debt levels are drastically reduced from today's Ponzi-driven heights, while in the meantime, second-order effects of the dynamics of debt will dominate asset markets as well as economic activity.

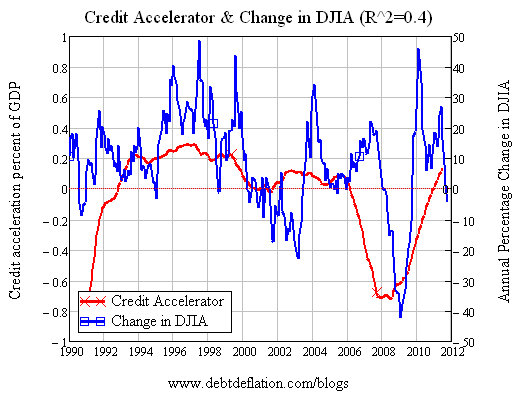

Figure : Credit Accelerator and Change in the DJIA

To escape from this crisis, we need not only to focus on its real cause - excessive private lending that funded Ponzi bubbles in asset markets - but also to escape from the Neoclassical mindset "which ramify, for those brought up [on it], into every corner of our minds" (Keynes 1936). That intellectual liberation is the objective of Debunking Economics.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

10 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon