The complicity of the government, its regulators and the Australian Stock Exchange (ASX) in facilitating insider trading was highlighted in a report by the BT Financial Group released on November 11. Directors in over 60 per cent of the largest 200 ASX companies failed to report their share trading as required.

In the era of Henry Thornton, share trading was carried out in coffee houses. Share buyers and sellers met face to face and so were known to each other before they traded.

Such “sunlight” share trading is not possible today. Insiders, like company directors, managers, investment bankers, advisers and others can now buy and sell shares anonymously through brokers. Before governments licenced the operations of stock exchanges, brokers made the rules for share trading to suit their own private interests.

Advertisement

The rules for trading shares anonymously were made by brokers. It allowed brokers to secretly take advantage of their clients by buying or selling ahead of their clients who had inside information. The law now requires financial advisers to know their clients so this places brokers in a privileged position of knowing if their clients have inside information.

The fact that covert share trading has been universally adopted throughout the world does not make it ethical or right. Nor does it make markets efficient in the sense of effectively informing market participants on how to efficiently allocate funds between competing opportunities. Neither does it allow market operations to be monitored on an effective or efficient basis.

Monitoring cannot be effective as insiders can hide their identity. Monitoring cannot be efficient as considerable resources are required in carrying out surveillance, investigation and taking legal action. Sunlight trading would introduce a self-enforcement regime as any person with inside information would need to disclose that they were insiders. The veracity of any claim by a share trader that they were not insiders would be exposed to all market players.

If an insider did not declare themselves, then the chances of someone, somewhere, at some time, discovering they were insiders would be considerable. Other traders would have a personal incentive to discover any duplicity and take legal action for restitution of any loss they might have suffered from non disclosure. Instead, with the current covert share trading regime, monitoring is carried out by a computer and or officials watching anonymous trades with no personal financial investment in the outcome of their work and very little exposure to the identify of market participants.

Not withstanding that, the ASX requires share trading being initiated on a covert basis by insiders and or brokers: officials of the ASX have the chutzpah to claim that they operate a fair and transparent market place. The BT report provides evidence that such statements represent false and misleading conduct.

The federal treasurer has expressed concerned over the secrecy of Swiss banks hiding insider trading by Australians. It is the treasurer not the Swiss banks that create the problem in allowing the ASX to keep secret the identity of those trading shares. A fundamental rule in business is to know with whom you are dealing. If the treasurer and the government wanted to protect a majority of their constituents they would require the ASX to adopt sunlight trading. Their failure to do so illustrates how captive they and their advisers are to minority insider interests.

Advertisement

It is hypocritical for Australian regulators to require companies to continuously disclose any price sensitive information yet not also to require continuous disclosure of who is trading shares. The identity of who is trading shares can also be price-sensitive information.

If large institutional investors object to sunlight trading because they believe that this would put them at a disadvantage, then they are proving the point that the identity of who is trading is price sensitive information.

If investors do not wish to reveal their identity then they should invest only in privately held assets. The privilege of investing publicly and obtaining liquidity should carry with it the obligation for participants to disclosure the identity of all those involved in the ownership and or control of the shares traded.

The ASX might be concerned that they would lose business with sunlight trading as companies would decide to list their shares on other exchanges. This might well be the case for those companies whose officers wish to take advantage of inside information. However, I would argue that the opposite result could occur with overseas companies seeking a listing in Australia, so they could protect their shareholders from insider traders and prevent their employees from unfairly taking advantage of outsiders. Sunlight trading by the ASX would make Australia a world leader in establishing ethical investing with a truly transparent market place with its integrity safeguarded on a market driven self-enforcing basis.

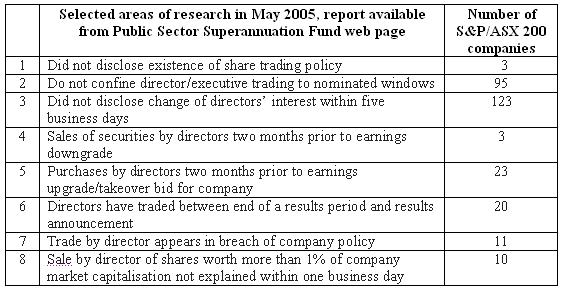

All the current rules and rituals of directors and officers trading shares could be eliminated. The current rules give false comfort and are expensive meaningless distractions. These rules provide the basis for the BT report as set out in the table below that was obtained from the website of the Public Sector Superannuation fund, a sponsor of the study.

Public Sector Superannuation Fund web page here.

Confining share trading to nominated trading “windows” as noted in row 2 in the table does not protect outsiders from insiders with superior information. Sunlight trading would allow directors and insiders to continuous trade at any time of the year to create a much more liquid and informed market. Similarly, disclosing director trading five days after the event as noted in row 3 of the table does not protect the uninformed counter party to the trade. There are many other insiders beside directors that the report did not investigate. All these other types of traders would need to disclose if they had privileged information to avoid the risk of being sued when the inside information was made public to allow insiders to be exposed to being identified.

A simple solution would be for the government to cancel the ASX operating licence and require all Australian shares to be traded on E-Bay. E-Bay not only requires disclosure by participants of themselves and what they know about the goods being offered but it also outlines their trading history. In addition E-Bay allows counter parties to rate their satisfaction in how the quality of the goods traded matched the description of the seller.

Sunlight trading not only provides far greater protection for investors and traders but creates a much fairer and efficient market. It avoids the cost of ineffectual monitoring of market activities. Its time that market ideologues walked the talk to privatise both monitoring and corrective action of insider trading.

His submission to the Australian Senate Inquiry into “The framework of the market supervision of Australia's stock exchanges” of February 5, 2001 is posted here. This article was first published on Henry Thornton on November 16, 2005.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon