For decades we’ve lived with a range of accepted truisms around city planning, urban development and infrastructure planning. Then along came a virus. Some suggest the long-term impacts of the current pandemic will turn fundamentals on their head. Others – myself included – are more sanguine. But changes there will be and, as Bowie sang, we need to face them.

This article tries to sum up some thoughts of my own and distil a good amount of reading over recent weeks. Nothing here is a given, but simply offered to encourage us to think carefully about what lies ahead. The first thing to keep in mind is what Indeed.com’s global Chief Economist Jed Kolko pointed out to me a few weeks ago: "Many of the post-pandemic predictions are really just statements of how the prediction-maker has always wanted the world to change. The virus doesn't kill cognitive biases!" I will try avoid that trap.

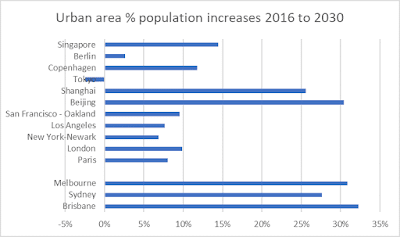

Australia’s population growth has been driven by direct overseas migration, and much of that has concentrated itself into three capitals, each of which was predicted to grow by close to a third in the 2016 to 2030 period. That rate of growth was ahead of many world cities. Would we have managed, without falling further behind on infrastructure? Growth has taken a short term hit thanks to closed borders. It remains to be seen if those growth rates will slow over the longer term. A slower rate of growth may not be a bad thing: it could allow us to catch up with infrastructure, hence improving quality of life, rather than being in constant lag mode. This in turn could support property values by making places more desirable – as opposed to just crowded. Remember, some of the most highly prized property markets around the world are actually in low growth areas. It is their desirability, environment and placemaking qualities that makes them so.

If growth is to slow, would that change a wide range of urban policy settings, with the dial turning from volume to quality?

Housing:

Predictions that housing demand will change quickly from inner city apartments to suburban housing are I think wrong. For starters, inner city apartment demand for much of recent history was driven mostly by speculators who had no intention of actually living in the one-bedroom, low cost apartment they were buying off the plan. That frenetic level of speculator activity created a false impression about the extent of real demand for inner city apartments. There are now more two and three bedroom inner city units being designed which are more likely to meet with owner occupier needs. But being larger, they will also be more expensive.

Suburban housing has tended to dominate urban settlement in Australia and while the pandemic may remind us that the burbs may not be so bad a place for a lockdown, those who live there now do so by choice, and because 8 in 10 of us actually work in suburban locations. The same applies to inner city apartment dwellers who choose where to live for work or other reasons. There may be some changes in preference if more people seek out suburban work locations (as opposed to densely populated inner-city ones) but I can’t see wholesale change here.

Neither can I see prices collapsing in the long term. The cost of new supply – land plus building costs plus taxes – tends to be fixed. Unless there is a major change in those supply side drivers, any movements in house prices will reflect shorter term economic circumstances (more owners needing to sell than buyers able to buy).

Finally, the argument that housing design will change to better facilitate home offices for work from home needs to be kept in context. This may happen on some new product but as this only affects new supply (and renovations to existing supply) we aren’t likely to see a wholesale change of our housing stock to accommodate work from home (which only works for some occupations anyway). There is also speculation that home isolation will mean a move to larger balconies in townhouses and apartments, as we appreciate the importance of space more. You could counter that this was always the case, but larger balconies and home offices mean larger floorspaces and townhouses and apartments are expensive to begin with. This prediction, if it eventuates, will simply make new product significantly more expensive. Will there be a sufficiently large market to pay?

Work from home?

No doubt the future will see more people working from home, either on occasion or routinely, than in the past. Some companies may direct that this change happens in pursuit of cost savings, and some individuals will request it for lifestyle or other reasons. But for the vast majority, my thoughts are that once a return to the workplace is allowed, many will return with enthusiasm. Productivity, creative engagement and the social value of work are genuine positives for that proportion of the workforce who do work in offices (and for whom work from home is possible). As this article in Bloomberg wryly observed, the whole work from home thing has soured quickly for many:

“Many mapped out plans to fill time they would’ve spent commuting to take up new hobbies, like learning a foreign language, baking or getting into the best shape of their lives. It looked like the beginnings of a telecommuting revolution… A month and a half later, people are overworked, stressed, and eager to get back to the office. “

Offices:

The office market could be in for some changes but these may take time. Markets like this will tend to be quite ‘sticky’ because of things like long term leases and fixed fitouts, which make quick adaptation difficult. However, it does seem likely that things like an 8 square metre per person benchmark - which was becoming common - could reverse and the trend head in the direction of more space per person.

Imagine a company of 100 staff ready to lease new premises. Where once they would have needed 800m2 they may soon be thinking more like 1500m2 (15 or even 20 square metres per person were more typical in the 1990s through to early 2000s). Will they actually lease that 1500m2 or instead reduce their workforce for those premises to around 53 people for the 800m2 tenancy and instead send staff for whom a CBD location is non-essential to suburban collaboration hubs, or have some of them work from home?

Less density of workers in expensive CBD offices makes them more expensive, per worker. Suburban business centres may benefit from this. How this change plays out will have a long-term impact on office space demand.

Retail:

Hard hit even in the lead up to the spread of the Coronavirus by flat wage growth and online competition, shopping centres and retailers have been frontline victims of the viral shutdown. As we emerge from our burrows into a post viral world, industry consensus is that there are big changes for this sector going forward. Tenants may have taught themselves that the value of paying to be close to centre-generated foot traffic can be traded off against more aggressive online strategies with a neighbourhood shop front presence. And a proportion of consumers may equally have adapted to sourcing their immediate retail needs more locally, rather than travelling to major centres. There are potential lasting changes too in the types of consumption habits of consumers.

Major mall owners have survived multiple predictions of the end of bricks and mortar retail in the past, and I have no doubt they will innovate and survive again – but as in the past, it will likely mean significant changes to tenancy profiles and to the nature of the centre itself. Typically very well located, with public and private transport connections, these assets will always find a market. My money is on more health, education and community service functions increasingly making their presence felt.

For the suburban strip or neighbourhood centre though, the changes in retail could be a positive – provided they can provide a high standard of amenity (placemaking appeal) and convenience (eg ample parking) and affordable rentals. Given that many have received little government investment in their improvement for decades (governments were too preoccupied with the inner cities) and given that many landowners have likewise invested little in some of their assets, many centres may miss their opportunity for renewal. How governments and private owners might work together to avoid that happening will be interesting.

Public transport:

What happens with public transport in the future will be fascinating. Having already faced flat or falling mode shares, will a post-viral world see more commuters recoil at the idea of joining fellow travellers in crowded trains or buses, coughing and sneezing in close proximity?

How could this affect demand, and will public transport providers respond with less passenger density (as some airlines already seem to be proposing)? And will this in turn mean even higher costs for PT given lower passenger density? And will more people drive instead, leading to a spike in congestion? Or will the whole idea of commuting en-masse to centralised workplaces served by public transport start to pale in favour of local commutes – including by walking or cycling - to suburban business hubs for collaboration and the social aspects of work? This is city changing stuff. Watch with interest for the short term response once the economy opens up again, and for long term changes.

Health:

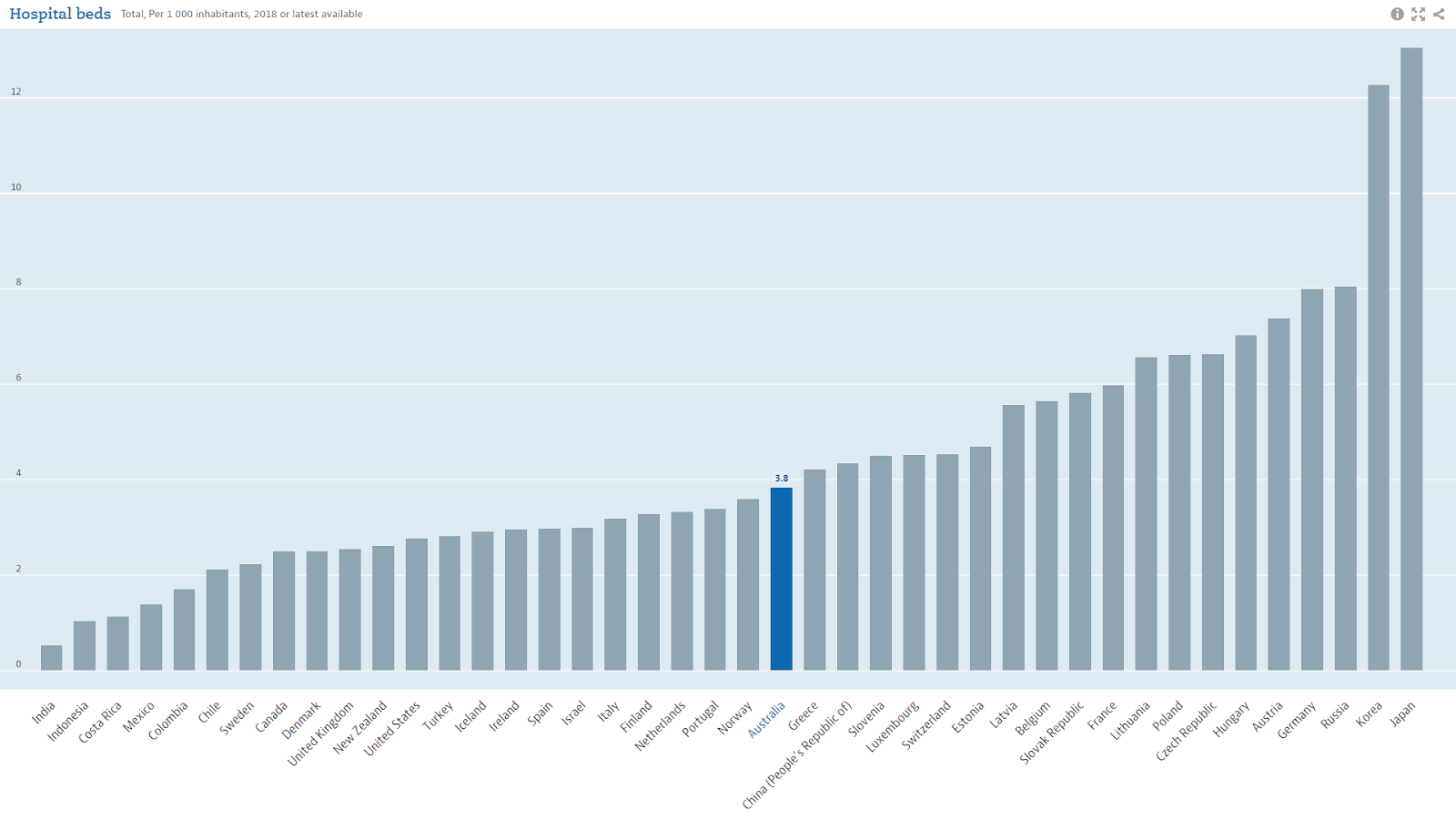

Health was already predicted to the fastest growing industry in Australia prior to the pandemic. I can only see this accelerating. Health services are typically not centralised so this growth is likely to benefit suburban and regional centres – not just in the capital value of the infrastructure but also the jobs that come with it. Australia’s investment in health is good by world standards but not (I was surprised to learn) world leading. The graph below shows the number of hospital beds per 1000 of population, as just one metric. Will we move to lift this level of provision? How will we fund it if we do? (And from the graph, you can see in part why the UK and USA have struggled, and why India is so worried).

Education:

Education – especially tertiary – became one of our leading export industries in recent years. It was also a ‘clean’ industry and ticked a lot of boxes in terms of international relationships. There is no question that education sectors heavily reliant on foreign fee-paying students have hit a virtual brick wall – the question really is to what extent this will recover and how long it might take if it does?

Failure to quickly recover could jeopardise billions of dollars in proposed capital expansion and improvement plans, plus put pressure on fees for domestic students. It would also mean we would need to find a replacement source of foreign income. More coal anyone?

Manufacturing and industry:

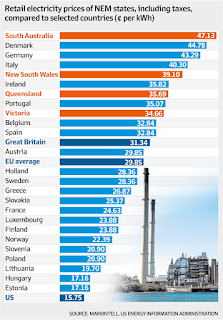

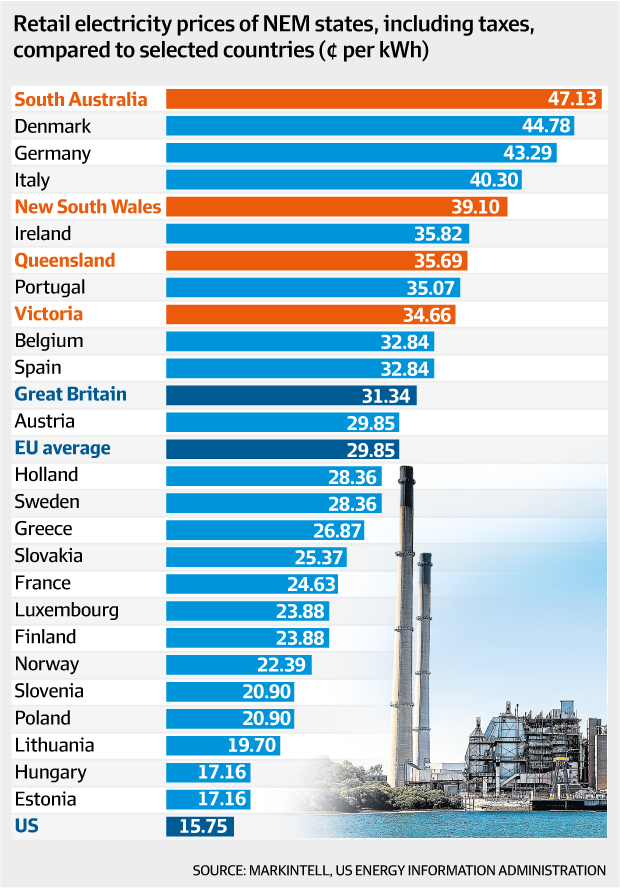

A possible beneficiary of changed international trade arrangements could be the local manufacturing and industrial sector. Employing 20% of Australian workers, this sector has been in slow decline over the long term but can rapidly retool to replace a wide range of imported products. Skilled and affordable labour isn’t the issue it once was – the issue now is the high cost of energy. Australia’s energy costs have hurtled ahead of inflation to become some of the most expensive in the world. Given we have a small domestic market and international markets are a long way away, lower prices for longer is what this sector needs from the energy market, and a subsidised and expensive renewables market just isn’t ready to provide that yet. Again, more coal anymore? Or nuclear? Hmmm.

Finally, to end with something from a mate who was once head of planning for Brisbane City Council, ran his own business, later becoming a key part of the ULI growth story into Europe and Asia and who now teaches planning and real estate development at Texas A&M University – Professor Geoffrey Booth. As Geoff said to me in a recent note, changes from this pandemic are inevitable because our patterns of human interaction will change:

Never forget that all real estate is place and it is people that create the enduring value of real estate – take out the people and there is no market, no demand, and no one to buy it or pay in one way or another to use it, and as a consequence, you the real estate developer, left with no raison d'être, starves to death. There will be a world after Covid-19 but as our patterns of repeat visitation have been severely disrupted, as a consequence, the real estate market will be forever changed.

If only we knew how, and where, and when this will happen.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon