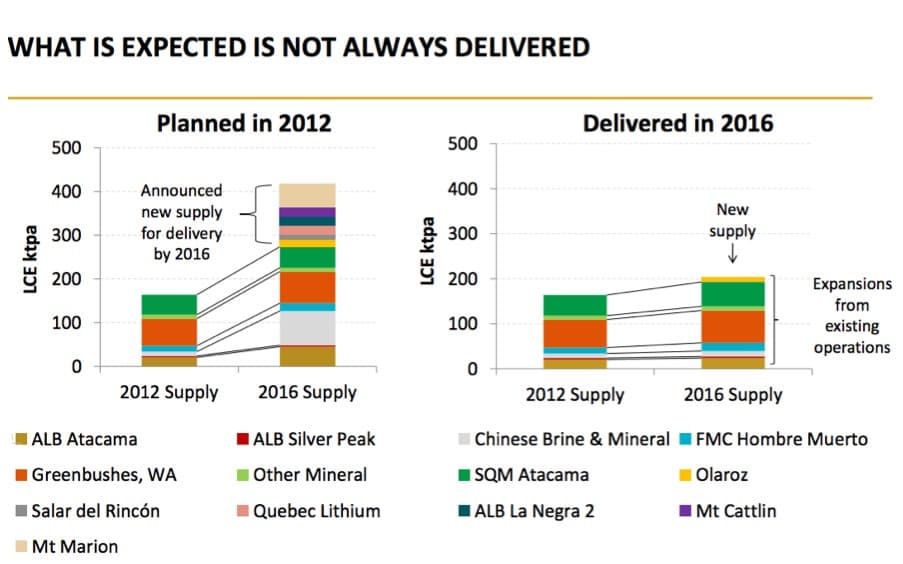

The screenshot below from Orocobre's investor slide presentation is a sobering reminder to this reality.

IMG URL: https://d32r1sh890xpii.cloudfront.net/tinymce/2019-01/1548715289-a41.jpg

Source: Mining.com

Advertisement

In terms of feedstock supply, SQM and Albemarle had laid out plans for increased production rates. But as is often the case with brine evaporation, the process has been hindered by seemingly endless production delays. SQM hit technical obstacles at its new brine conversion facilities that delayed its target capacity of 70,000 tpa LCE by end of 2018 while Albemarle continues to struggle to achieve full capacity at La Negra II.

The situation has not been much better in China—the ultimate lynchpin to the lithium bear thesis. Many Chinese brine producers in the Qinghai region had outlined plans to triple or quadruple capacities over the coming 3-4 years. A visit by Benchmark Minerals to these operations, however, has painted a dire picture—the technical challenges related to high magnesium concentrations in the region are nowhere near being comprehensively overcome. Across Qinghai's 10 producers, only an additional 5,000-10,000 tonnes of lithium product found its way to the market, majority of which failed to reach technical grade specifications. This, in effect, means that much of what came online from the region was either reprocessed thus adding to costs or converted to lithium hydroxide in a bid to meet growing demand for nickel-rich cathode technologies.

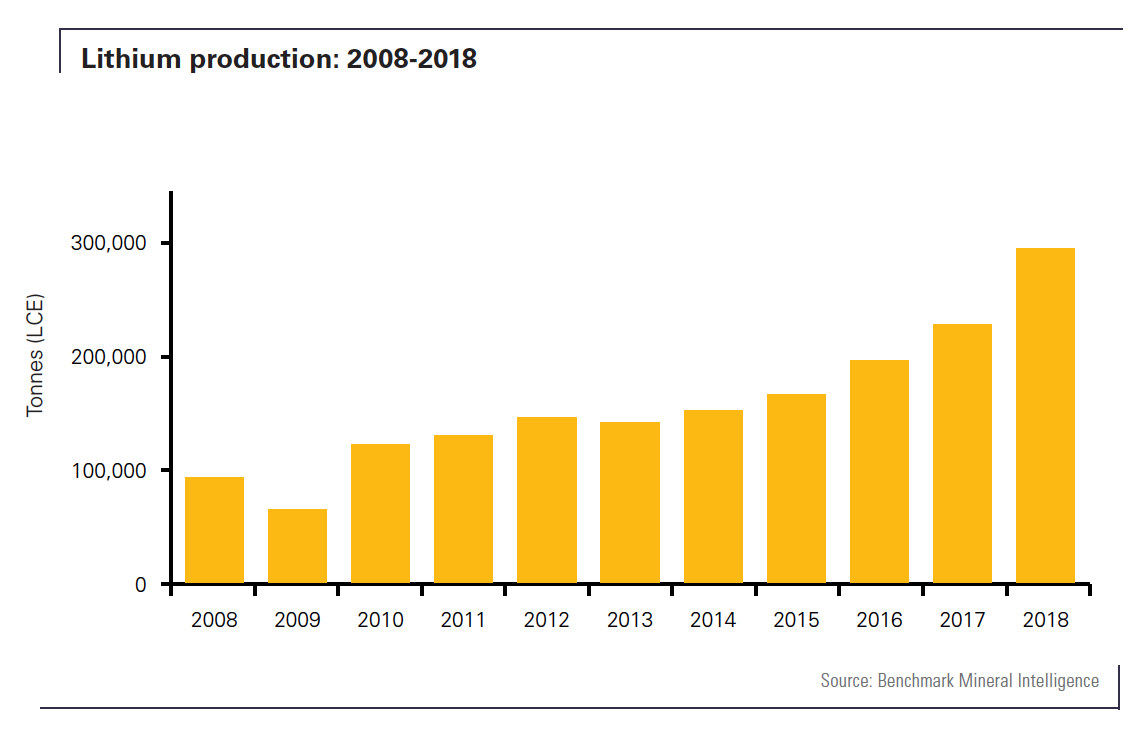

Although tight credit in China forced some lithium buyers to destock and contributed to the glut, the predicted huge oversupply failed to materialize. Around mid-September, analysts at CRU estimated lithium surplus for 2018 at a relatively mild 22,000 tonnes against a demand of 277,000 tonnes.'

IMG URL: https://d32r1sh890xpii.cloudfront.net/tinymce/2019-01/1548715350-a5.png

Source: Benchmark Minerals

2019: A Transition Year

Advertisement

So far, there is no clear data or evidence that that the lithium demand narrative is about to slowdown, let alone reverse. On the contrary, certain emerging trends in the industry suggest just the opposite.

The biggest near-term driver for lithium demand is the NCM trend. The shift towards cathodes that use huge amounts of lithium hydroxide is already underway, something that is expected to trigger a huge NCM (nickel-cobalt-manganese) ramp up. Benchmark Minerals estimates that 44 percent of mega-and-giga-factories will use lithium as a raw material by 2028 translating into 534,000 tonnes of additional demand.

That projection seems to resonate with Elon Musk's ambitious target to build 20 gigafactories across the globe over the next decade. Miller sees 2019 as the tipping point where demand will eventually outstrip supply starting 2020.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

8 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon