There is much anxious discussion today about the low economic growth rates, or 'secular stagnation', besetting the global economy. As many have noted, this has played a crucial role in the rise of anti-establishment 'populist' parties across the globe. But are mainstream economic theories – i.e. neo-classical, Keynesian, etc. – adequate for explaining the phenomena, or is a new 'biophysical' approach needed?

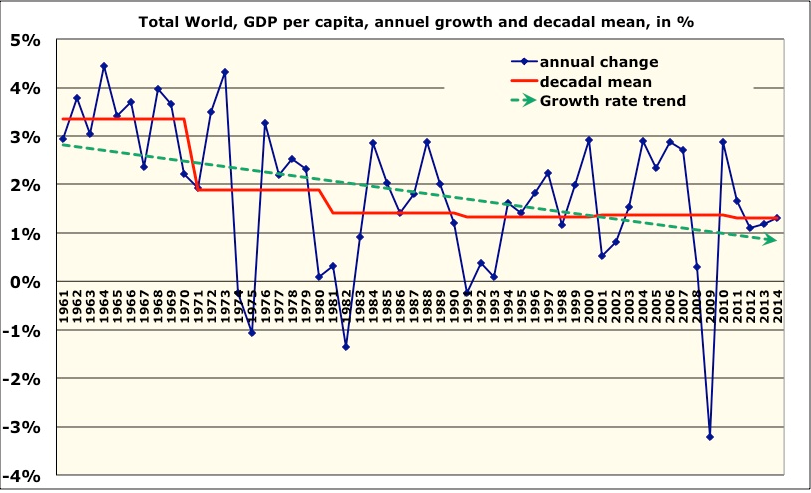

While most analysts have focused on the slowdown in GDP growth rates over the last decade, one can notice a declining trend beginning as far back as the 1960s. Jean-Marc Jancovici shows that in the 1960s world GDP per capita was increasing at +3.5 % per year, however, in the 1970s the rate declined to +2% on average across the decade, and for the last three decades it has been about +1.5%.

Advertisement

Source: World Bank, 2015

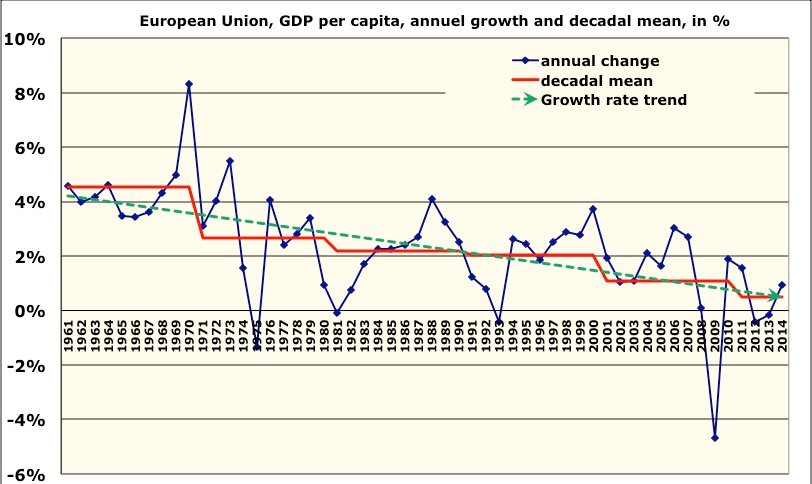

This global trend, of course, hides major regional variation – in Asia, for example, growth in per capita income has accelerated over the same period. The reason for the overall declining trend, is largely a consequence of the OECD countries (i.e. advanced industrial) which, until recently concentrated a large share of global GDP, but which have collectively experienced a much steeper decline in per capita income growth than elsewhere.

Source: World Bank 2015

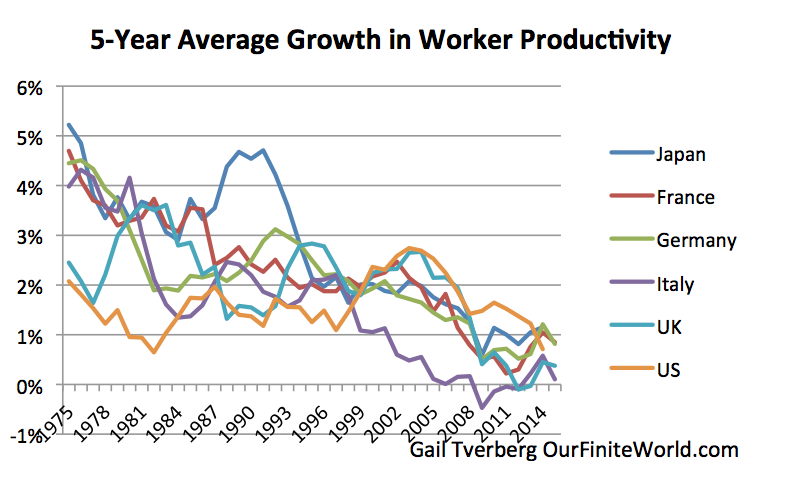

The decline in OECD income growth is strongly related to a parallel decline in labor productivity over the same period, which is not surprising given productivity improvement has long been understood a key driver of growth.

Advertisement

This declining rate of growth is more surprising given, much of it has been driven by spiraling rates of public and private debt. Beginning in the mid-1980s, the global debt to GDP ratio has increased dramatically to the point now where the global economy is saddled with an estimated $152 trillion worth of debt, which is equivalent to 225% of global GDP. And how have governments responded? Largely via monetary policies such as negative interest rates, which make credit (and thus debt) easier to attain in a desperate effort to restore historical growth rates – but so far to little avail.

These trends have sparked a wide-ranging debate among economists. Explanations have varied according to those that put more emphasis on supply-side against demand-side factors. On the supply side the slowdown in productivity has been attributed to diminishing returns from new technical innovations, whereas on the demand side, the problem is believed to lie in the decline in aggregate demand due to a build-up in the rate of saving. This demand side diagnosis is usually followed by a call for more active fiscal policy, or a redistribution of income towards lower income groups with a higher propensity to consume.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

18 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon