The changing economy is an irresistible force, the impacts of which are being played out on many fronts. As jobs and the nature of work change under the relentless advance of technology, so too are decisions about where workplaces should be located. Central business districts – long the glamourous headquarter preference for leading professional service firms – are under increasing pressure from competing centres. Contrary to popular belief - and no doubt to the disappointment of inner urban boosters utterly fixated on the virtues of a downtown live/work/play lifestyle to the exclusion of all else - the non-central parts of our major metropolitan regions are the ones that are growing jobs at the fastest rate.

The reality of suburban dominance on housing and economic fronts is something I’ve been writing about for some years now and every time I consult fresh data, that reality is confirmed. In our major metropolitan areas, it is the suburban domain where more than 80% of jobs are and where nine out of ten people choose to live. This isn’t to deny the CBDs their premier role as the seats of government or as a central focus for community-wide cultural facilities, executive business offices and places for social interaction. But it does point to a possible imbalance in infrastructure priorities or policy attention – the bulk of which seems now to favour privileged inner city domains to the exclusion of economically larger suburban locations.

The latest labour force data from the Australian Bureau of Statistics paints the evidentiary picture. Taking in our three largest metropolitan areas, employment growth in the inner city areas over the last five years is not the dominant story some might have you believe.

Advertisement

The labour force data is by SA4 level, which broadly means for metro areas something much larger than a suburb but smaller than a city. It typically combines multiple suburbs into a population group of 300,000 to 400,000.

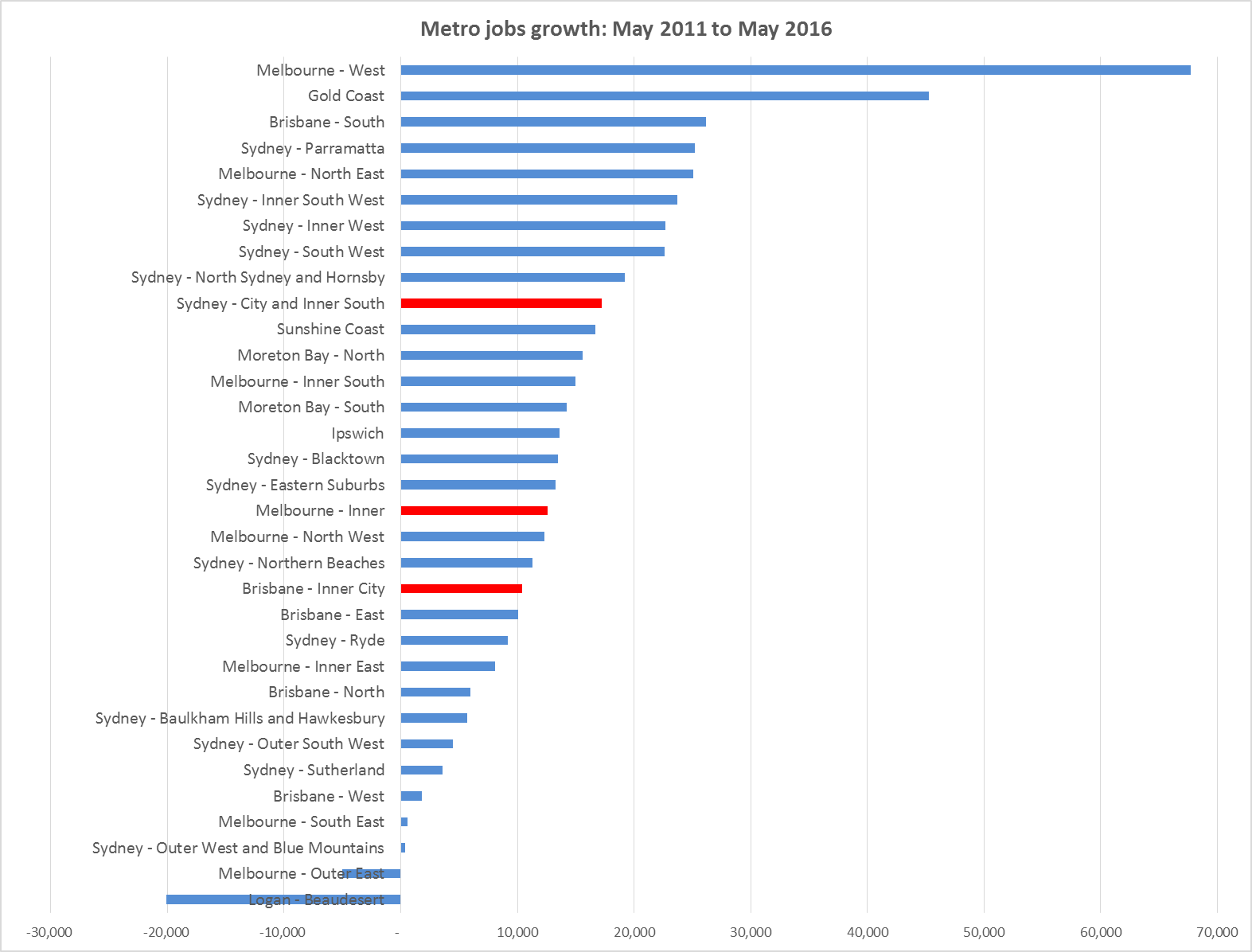

The chart below shows employment growth of non-central parts of our metro regions in blue, while the CBD and inner city regions are highlighted in red. (click on the image to expand)

What’s immediately apparent is how many blue non-central locations are outperforming the inner city regions. Cities may well be the engine rooms of the economy but it’s evident from this data that those engines, in job terms at least, are producing more output in the suburbs.

Advertisement

In fact, of the total 468,300 new jobs created in these three large urban areas in this five year period, 91% of them were for people created in non-central locations.

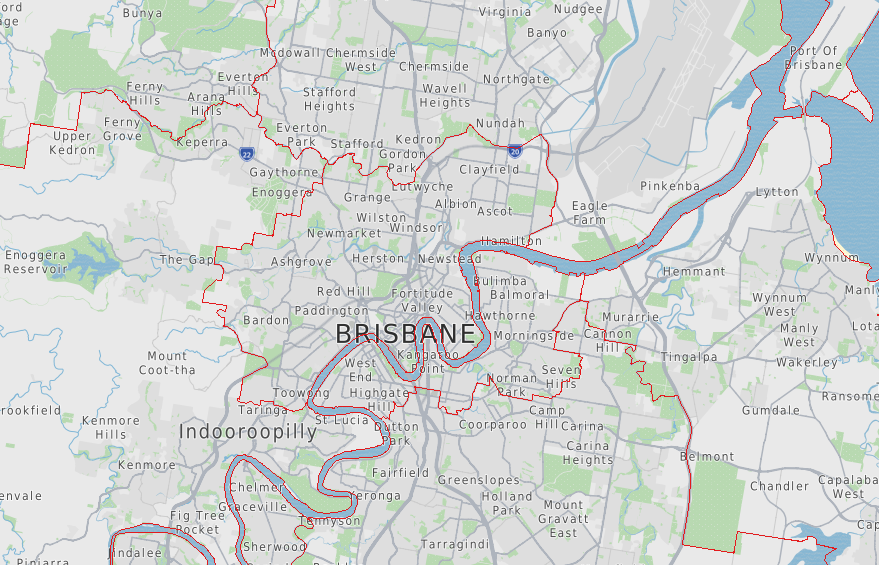

Keep in mind that this definition of inner city is much broader than just a CBD and fringe, as popular opinion and industry convention might define the inner city. For Brisbane, its boundary stretches from Toowong to Bardon, The Grange, Clayfield and south to Seven Hills and Norman Park.

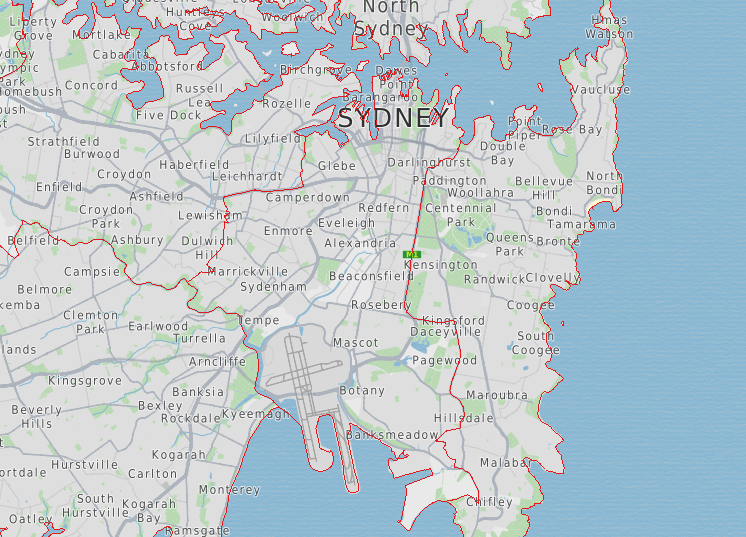

For Sydney, the ‘City and inner south’ stretches from the CBD south to the Airport, and as far west as Marrickville.

And in Melbourne’s case, the “Melbourne inner” area follows the Maribyrnong River in the west, north to Essendon North, across to Coburg, Fairfield and south as far as Malvern and Ripponlea.

The point being that these are very generous boundaries for inner city areas. They are large enough to include dozens of inner city suburbs and some that are considered middle ring. And yet despite these large boundaries, it was the areas that lie beyond these inner city areas that have been powering the jobs growth performance of our major cities. This economic reality may not sit well with the true believers of inner urban supremacy, but it is statistically undeniable.

The strongest performance of all was Melbourne West, which added over 60,000 jobs in the five year period. The Gold Coast, bouncing out of one its many cyclical downturns into an upswing, was second, followed by Brisbane Southside, followed by Parramatta. All are what we would generally define as middle to outer urban areas (the Gold Coast being either its own distinct city or part of the south east Queensland conurbation, depending on your point of view).

If we look at the numbers in percentage terms, there are a significant number of SA4 regions that have grown by more than 10% in the period.

Of the three inner city markets, only Sydney just crept into this league. Inner Melbourne’s 3.8% growth is anemic by comparison with the suburban performance of many of its metro areas, and Brisbane’s inner city growth of 7% over the five years looks weak compared to its Southside, or Moreton Bay regions which grew by double that in the same period.

What’s driving this suburban growth?

Looking at the four fastest growing regions of our largest metro areas, the answer is mostly ‘health care and social assistance.’ This type of industry, which is Australia’s fastest growing at present, has little need for centralised locations but requires access to the communities it serves, which are largely to be found in suburban locations. In the case of the Gold Coast, having a new major hospital open in this period obviously helps. Health and social assistance is broadly followed by education and training (another non-centralised type of industry) and then there’s also retail trade (non-centralised by nature) followed by various other more localised strengths.

The so called ‘knowledge workers’ are represented by the ‘professional, scientific and technical services’ category which also made significant contribution to the four fastest growing areas. This is an interesting feature of the changing economy because it was a long held article of faith that knowledge workers (white collar service industries from engineers to architects to bankers and lawyers) would always instinctively gravitate to CBDs. This remains mostly so for larger firms but increasingly we are seeing these functions also select suburban centres which offer lower cost structures and a more village scale amenity that rivals the large scale and anonymity of a large bustling CBD.

So what’s this telling us?

There is a growing orthodoxy which claims that it will be the professional services industry that drives our growth as a nation. No argument there. But the orthodoxy then seems to go on to suggest that workers in the professional services industry will all (mainly) be working in our CBDs and inner city areas, and that the sensible strategy for supporting that growth in the future is to funnel greater concentrations of infrastructure into servicing this demand, and to support further rapid escalations in inner urban density so that more people can live closer to their inner city jobs. This, we are told, is where all the action is and where it’s going to continue.

The evidence, however, keeps resolutely pointing another way. Rapid changes in business and personal mobility thanks to digital technology are paving the way for businesses to be more flexible in their location choices. Plus, the fastest growing industries at present are not the types of industries that need the highly centralised and densified work and living arrangements found in our CBDs.

Our CBDs will continue to maintain their headquarter function for many businesses, and will continue to the seats of government, but it may well be that their role as a central business district will begin to morph into more of a central amenity district – providing cultural, entertainment and recreational opportunities for the wider metropolitan community that cannot (due to cost or other factors) be replicated many times in suburban areas.

If this is true and we are living through a period of fundamental economic change in business location decisions, the role and importance of suburban business districts will only continue to increase. This should mean that – along with identifying infrastructure priorities for inner urban areas – we need to turn our attention to the equally valid claims of growing suburban centres for improved economic and social infrastructure.

The evidence is that some 90% of new jobs in our largest urban areas over the last five years were created outside the magical inner city ‘rings’. Recognising this statistical reality will be the first step toward a more balanced approach to urban growth and the setting of urban economic priorities.

Footnotes:

These SA4 statistical boundaries are very large areas, useful for general analysis like this but the larger the area, the more complexity hides behind the numbers. For example, within some of the inner city SA4 areas, it is entirely possible that within the SA4 boundary actual CBDs are shrinking while near city areas are growing, or the opposite. You need to drill down to a smaller area to answer that question. Let me know if you are interested to find out.

Nor can I explain the abnormally strong performance of West Melbourne in this data, nor the weak performance of Logan-Beaudesert (south of Brisbane). I am looking further into both. It could be due to a small boundary change (although the ABS makes no mention of it that I could find) or due to mixed industry areas jumping boundaries as brownfields close down in favour of newer development areas next door.

The very strong performance of many Sydney regions, including those near the inner city, is also worth comment. Six out of the top ten fastest growing SA4s are in Sydney. The story of Sydney’s increasing national economic muscle is something I wrote about here. Sydney is at present dragging the rest of the Australian economy along behind it. Without this one city, the technical word for our national economic condition would be is ‘rooted.’

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon