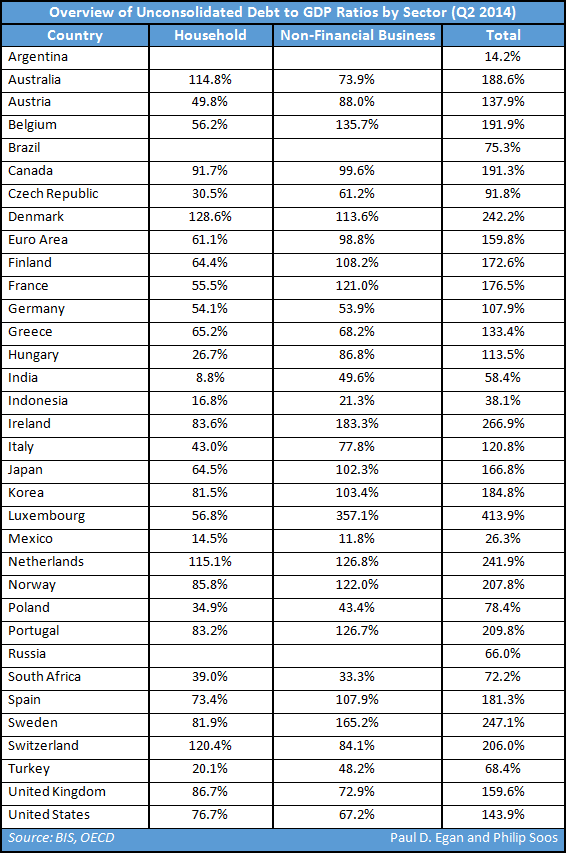

The BIS has done a commendable job in gathering long-term unconsolidated data from the OECD and BRIC nations and making it publicly available. It would be helpful if the data was further classified into categories of personal, mortgage and non-banking financial sector debt, as the latter is important when analysing banking and financial cycles.

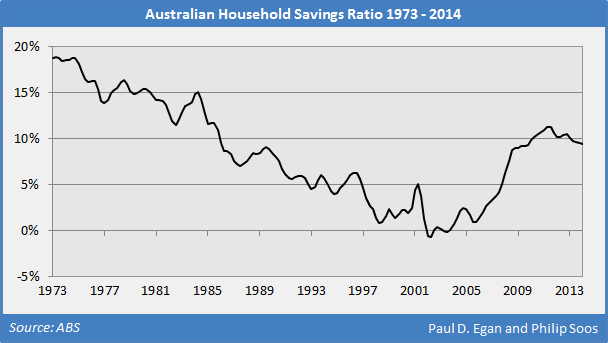

As household debt has boomed exponentially over the last two decades, the savings of the household sector has plunged. According to the official household savings ratio provided by the ABS, it briefly became negative during the early 2000s, and then rebounded as the GFC shocked households into saving more.

Advertisement

In 2013, analysis by Credit Suisse revealed that the official ratio included superannuation contributions and extra principal repayments, which arguably should not be counted as disposable savings. After controlling for these two artefacts, the ratio falls significantly, exhibiting a persistently negative trend since 1997.

The household sector's savings situation is dire, as reported by ME Bank in a 2014 report:

- Only 46 per cent of households reported the ability to save each month;

- Only 32 per cent would easily be able to raise $3,000 in an emergency;

- 50 per cent aren't confident they have enough savings to last if unemployed for three months;

- 35 per cent reported having less than $1,000 cash on hand;

- 17 per cent have less than $100 in savings;

- 60 per cent have less than $10,000 in savings; and

- In 2009, Australians were saving a median $300 per year (AMP/NATSEM).

Australia's private sector is grossly over-indebted, especially the household sector. The hysteria surrounding Australia's non-existent public budget 'emergency' is a smokescreen cloaking the critical household budget crisis. The fictional narrative concerning public debt arises from an unshakeable adherence to pseudo-scientific economic theory and class war, such as 'justified' public austerity policies which target the poor and marginalised.

Meanwhile, the public is distracted from the true threat: the unrestrained private spending spree that further enhance the power, profit and authority of the horde of private monopolists, usurers, speculators, rent seekers, free riders, financial robber barons, control frauds and indolent rich.

Advertisement

The current dynamics of the political and economic system means private debts will continue to spiral out of control, until the catastrophically-inefficient FIRE sector inevitably implodes. Nevertheless, the current housing booms in Melbourne and Sydney show no sign of abating in the short-term, with 2012 an opportune time to purchase according to the 'Speculative Index', which measures the irrational exuberance embedded in prices.

If the real estate fever gripping the nation does not break soon, Australia may well secure the top OECD ranking for the most over-indebted household sector. A financial crisis beckons, for history documents that extraordinary over-lending routinely precipitates chaos; falsifying expert claims that 'this time is different'.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

7 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon