There's a lot of hand wringing at the vacancy rates being reported for office markets at the moment but in more than 20 years, the analysis hasn't progressed much beyond basic questions of new supply and gross demand. Other factors are at work.

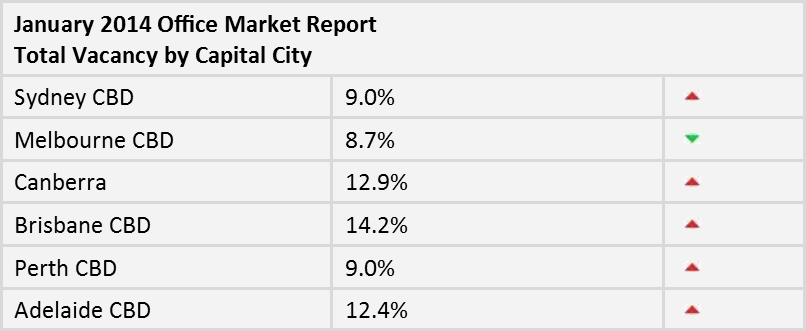

The latest Property Council office market survey reports Brisbane CBD vacancies as 'the highest level on record' at 14.2%. That's up from 12.8% the year before. The report attributes this to weak demand, specifically a "reflection of the impact of the Queensland Government's continued withdrawal from leased space, coupled with the mining sector's revaluation of its office space requirements."

No, it's not a pretty number and according to the PCA figures it's at present the worst of major markets in the country:

Advertisement

But these are just headline figures. Sure the Queensland Government has reduced its requirement for space, but that followed a sustained period of bloated public sector growth under the previous government. And sure the mining sector isn't on fire any more, but no one seriously thought it would ever stay that way. That's why mining related businesses were only taking space on 5 year leases: they knew themselves this wouldn't last.

So beyond the headlines, what are some of the other things that might be driving change in the market?

First, remember that a 14.2% vacancy rate is the same as an 85.8% occupancy rate. Most industries with that sort of capacity utilisation would be over the moon. It's a quirk of history that office markets have always reported on vacancies rather than focus on the occupancies. That's unlikely to change but what it means to seasoned observers is that this isn't the calamitous disaster media headlines might have us believe. Plus, take into account that a fully occupied market is generally regarded to be around 95% occupied; that 5% vacancy being required for normal movement. Any less and the market is under supplied. So really we've got about 10% of surplus space sloshing around in the market now.

Much of that space is sloshing around in lower grade buildings and what typically happens is that these are withdrawn from stock because they can't compete with contemporary space and the facilities it provides. Owners can refurbish older buildings, or convert them to alternate uses such as residential or short term accommodation. Expect a lot of both to happen in coming years. Those stock withdrawals will to an extent offset stock additions through some of the new projects under construction.

On the demand side, apart from blaming a downsizing by government and mining tenants, what other factors are in play?

Advertisement

Rents are surely one. Talking about office space demand without mentioning rents is a bit like talking about demand for petrol without mentioning the price. High construction costs, site acquisition costs and development costs mean that delivering new CBD office buildings is not a cheap exercise. Our CBD rents are some of the highest in the world. This Cushman & Wakefield report makes for interesting reading. According to the report, Brisbane is roughly 80% of Manhattan Grade A prices, is more than Melbourne, is 50% more than Houston Texas and three quarters of Sydney rents. Sydney rents are higher than New York. Go figure that one. Ask Holden, Ford or Qantas about the globalisation of markets and what happens to Australian product that is overpriced. Will that affect demand for office space if companies simply shift operations elsewhere, or are they faced with no choice but to pay globally high rents for what are not global scaled cities?

The other effect of high CBD rents is also force some hard thinking about the relative benefits of CBD over fringe. A lot of companies have recently opted for the latter. This could also be affecting demand for space in key CBD markets.

Floorspace ratios are another factor at play. New tenancies for major business are often being designed around per person space ratios as low as 10 metres per person. Concepts like 'hoteling' where staff don't have their own desk and where personal effects are discouraged, have fad surfers enthralled and financial controllers impressed. Personally, I can't see this lasting. We're human beings after all. Plus, it's only ever a handful of companies that explore the boundaries of these management fads and seek publicity for doing so. The silent majority of office tenants are as inefficient as ever, with spare desks and large common areas so the average in my opinion still works out at around 20 metres per person. Either way, it's an important factor on the demand side which isn't discussed much.

Parking costs are another factor. This is more a problem for casual parkers than permanents but both are paying exorbitant prices. If you are CBD based and have clients visiting your office, you should feel some sympathy for the $50 they'll shell out just for a two hour visit. These are some of the highest costs in Australia and equally some of the highest in the world. Those urban planners wanting to 'keep cars out the city' may succeed if this pricing response to limited supply keeps following the same trajectory. But if you keep the cars out of the city, you'll keep the people out too, and along with them, their business. The very high cost of parking, both for tenants and customers of those tenants, could be another factor weighing against demand for CBD space.

These are just some of the considerations that reach beyond the basic numbers. There are more but the point is that a 14% vacancy rate owes itself to a wider range of market forces than superficial reports deal with.

Is 14% a cause for concern? That depends on where the vacancies are… in someone else's building or yours.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon