There is a system for dealing with bad loans made by bank officers: it’s called bankruptcy. The EU/IMF solution to Ireland’s problem is to borrow from someone else to pay for the mistakes made by the Irish banks. The people who should really lose money, as Jim Rogers pointed out, are the shareholders and bondholders in the banks. This is not a risk free world we live in.

Rogers pointed out that Ireland’s banks borrowed up to 80% of Irish GDP to fund that country’s property boom. A lot of the loans went to developers as well as individual borrowers. When the property market went bust after the banks soon turned to the European Central Bank for repeated helpings of credit to delay the inevitable. This week, the inevitable arrived.

Could such a thing happen here? Well, according to the June issue of APRA’s always-scintillating “Quarterly Bank Performance,” Aussie banks have a combined $1.45 trillion in housing loans. The report says, “The banks showed a 4.0 per cent decrease in total assets over the year to 30 June 2010, driven predominantly by falls in other assets. Total housing loans increased by 12.3 per cent to $1,145.0 billion over the year.”

Advertisement

Hmm. So total housing loans (assets) for banks are about equal to total GDP. Now keep in mind Aussie banks have not borrowed all that money from abroad. Just some of it (quite a lot of it). This is one reason why Australia’s net foreign debt is around $670 billion. The housing boom has been financed with foreign money.

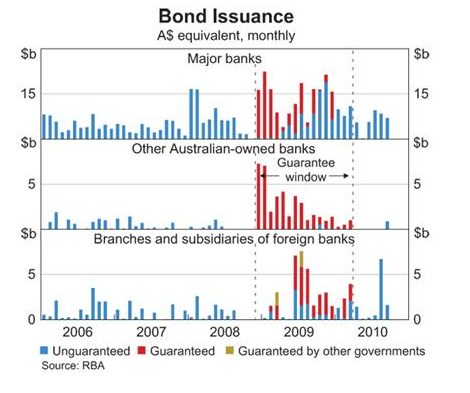

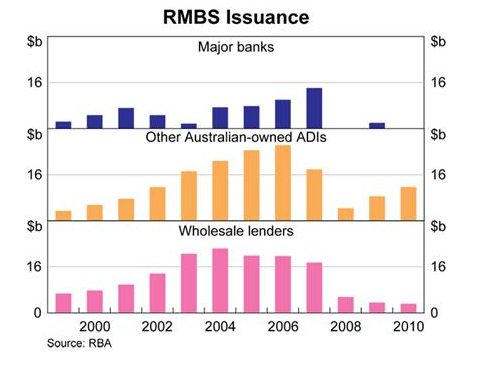

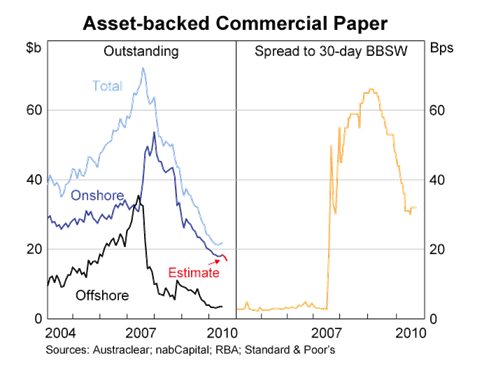

That’s not a problem, unless foreign money gets expensive or is no longer as forthcoming. As long as you can sell bonds to foreign borrowers you’re alright. But it’s a bit of a worry for the major banks, based on the charts below from the RBA, that foreigners may not be as keen to buy bonds issued by Aussie banks, although keep in mind the banks might not be keen to sell debt right now either when they can raise money through equity financing.

Advertisement

All three charts show that conventional and unconventional debt instruments have all declined as a source of funding since the GFC. The government has stepped into the Residential Mortgage Backed Securities (RMBS) market to support non-bank lenders and offer other sources of competition for bank lending. But for the most part, the unconventional sources of asset securitisation haven’t recovered to their pre-crisis highs.

Which brings us to covered bonds. No, it’s not a new type of underwear. It’s a source of funding for banks which uses deposits as collateral against default. In other words, the bank sells a security and the buyer of the security is first in line to be paid from bank deposits in the event that the bank is wound up.

You might wonder why a lender would have first access to bank deposits ahead of, say the depositor himself (you). And that’s a fair question. It’s also why covered bonds are a bit controversial. Putting creditors ahead of depositors in line for the distribution of assets would be a public relations disaster.

But it would only be a disaster if the bank is actually wound up and creditors (the buyers of covered bonds) get your money while you (the depositor) get nothing. And of course, if a bank sources just a small portion of its funding from covered bonds, it doesn’t represent a mortal threat to depositors and their deposits (you and your money in the bank).

Yet it’s telling that the Gillard government and Treasurer Wayne Swan are considering the introduction of covered bonds in Australia. Joe Hockey likes this idea, which should scare you even more. It’s a bi-partisan agreement on how to put housing even more at the epi-centre of Australia’s economy. Anytime politicians from the major parties agree on something, it’s bound to be bad for you.

The Big Four would claim that covered bonds are an additional source of funding for the housing boom that allows banks to lower borrowing costs to Australians because it lowers their aggregate cost of funding. But remember, the collateral for the bonds is your money in the bank.

What could possibly go wrong?

Well, hypothetically, a fall in bank asset values (housing crash) would raise concerns about bank liquidity and lead to doubts about the likelihood of a bank paying out on its covered bonds. This is what has happened in Ireland.

When Anglo-Irish Bank had ratings on its covered bonds cut by Moody’s, it showed that the Irish banks increasingly at the mercy of the ECB for continuous funding and that alternate sources of funding were tapped out. It also meant that the collateral for the bonds was in doubt, and forced the Irish government to try to make it good.

This last point is really the most important. Covered bonds were just the last in a long-line of ideas to keep Ireland’s housing boom going beyond all bounds of normality. Once the money ran out to keep prices inflating, the housing market collapsed and took the entire banking sector with it. This is how housing hijacks an economy.

So what does all this have to do with Australia? Well, in our view, Australia’s market has been partially hijacked by housing. Covered bonds would only make the bubble bigger, which would make housing even more unaffordable and lead to bigger losses down the track.

The recourse to covered bonds is being sought to keep the housing bubble from deflating. The banks, having exhausted the supply of first buyers, need to find new sources of funding to offer new mortgage products. And they might be worried that the traditional sources of funding are getting more expensive and more reluctant to feed Australia’s bubble.

The big risk with covered bonds is that they get abused as a cheap of way of sourcing funding for reckless lending. It works as long as house prices go up and up. But if house prices fall, then not only are depositors imperilled, but the government will be asked to help the banks with more cash to pay off investors. And when the value of bank loans exceeds GDP, not even the government can make that good.

Of course that could never happen here.

By the way, covered bonds are legal now in New Zealand. In fact, kiwi banks are selling the bonds denominated in foreign currency, which you think would expose them to massive currency risk. Incidentally, Aussie banks have a heaping helping of assets. We’ll get the figures for you tomorrow.

And finally, get a load of this from Dow Jones Newswires overnight: Standard & Poor's Monday shifted its outlook on New Zealand's foreign currency credit rating to negative from stable, warning on the country's dependence on offshore markets to fund its banking network and putting a spotlight on the its tepid economic recovery.

Hmmn.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon