We are in a bind, a complex predicament of our own doing. We have designed a financial system that must grow or it will implode. Was the GFC the first of a series of tremors signalling the onset of that implosion? Can we prevent or delay the implosion? I think we can and what I would like to do is propose one aspect of a plan that would use our superannuation in manner that might very well reduce the size and impact of future tremors on Australia and perhaps even prevent an implosion.

Before I do that however, let’s filter out the noise that surrounds our economy, examine some of the basic building blocks and consider its future direction. Fundamentally our society needs to be organised in such a way that our basic needs – food, shelter, health, education- are catered for with hope fully some spare capacity for the “nice to haves”. To date we have risen to this challenge by consuming more and more of everything, resulting in levels of economic activity that have consistently grown. Maintaining or increasing this level of economic activity relies upon there being sufficient inputs such as raw materials, energy and labour. This is where it becomes a little tricky. According to Justus von Liebig’s law of the minimum, growth is not controlled by the total resources available but by the scarcest resource or limiting factor (which I will call “Liebig factors”) in relation to the systems needs. Whilst Liebig developed this law after researching plant growth, it can equally be applied to economic systems.

According to Chris Clugston, 23 of 26 non-renewable natural resources that form the basis of industrial civilisation are likely to experience permanent global supply shortfalls by the year 2030. This includes such key inputs as oil, phosphate rock and metals such as gold, tungsten and cadmium. Even if Clugston is wrong by half, the outcome is the same - growth and economic activity is set to decline and with it our capacity to meet our most basic needs.

Advertisement

Now let’s consider money. Whilst many, if not most people think of money as being wealth, it is not. Money is simply an instrument to make accessing real wealth easier. Real wealth lies in the value of the goods and services that are purchased. Because there are so many goods and services in advanced societies such as ours, we need a common standard to facilitate the transfer of goods and services and this is the role of money. Sometimes however, we don’t have enough money to purchase things that we want, such as a home. In this case we borrow money from someone on the agreement that we will repay both the principal and the interest.

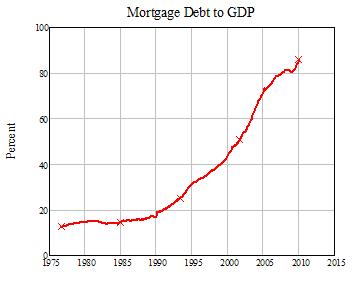

The term used to describe the situation where we owe someone something is debt and Australians along with just about everyone else seem to have fallen in love with debt. This willingness to take on debt coupled with the governments first home owners grant (or is that vendors grant?) as convincingly argued by Steve Keen, has resulted in the Australian real estate market remaining strong despite the GFC. The unfortunate consequence is that Australia’s Mortgage debt to GDP is at historic highs.

Source: Steve Keen’s Debtwatch No 44, http://www.debtdeflation.com/blogs/. Steve Keen suggests a healthy mortgage debt to GDP ratio is between 25 – 50%.

So let’s take these two factors, debt and declining economic activity, and fast forward a couple of decades to see what the economy might look like. Let us assume that oil is the key Liebig factor. As per Liebig’s law, as the amount of oil available declines, the price will increase as an indicator of scarcity. This will reduce the discretionary income available for activities such as travel and in turn increase unemployment in associated sectors. As unemployment increases, downwards pressure will be placed on wages, as the labour force rises in proportion to the jobs required to maintain a lower level of economic activity. Higher unemployment and lower wages will result in loan defaults and downwards pressure on asset prices. Indeed much of the long term debt on issue is unlikely to be re-paid once this process commences. The US housing market is a prime example where one quarter of mortgage holders are underwater and foreclosures continue at historically high levels. The availability of credit will decline as financial institutions realise that the ability for people to repay debt will fall as the level of economic activity contracts. Whilst we are likely to see periods of inflation and hyper-inflation in the transition to a shrinking economy, as governments attempt to keep the old system alive through methods such as quantitative easing, the overall trend, at least for assets such as real estate will be deflationary. In contrast inflation is likely to be the trend for commodities, particularly those commodities that become Liebig factors. It is the deflationary pressure on asset prices, particularly real estate that I will now consider.

Advertisement

Steve Keen argues that a property market crash is essential for positioning Australia for sustainable economic growth. This view in my opinion assumes there must be a day of reckoning in our economy and in particular the property market. But what if there was a course of action that allowed property debt to be reduced to manageable levels thus avoiding the property collapse and maybe even that of the financial system. This is arguably the most important predicament facing society today. The reason it is so important is that a zero-growth economy is incompatible with a debt based monetary system as eloquently explained by the University of Sussex’s Steve Sorrell. This situation is likely to be catastrophic in a contracting economy and thus timing thus becomes critical. Deflating the debt bubble must occur before Liebig factors take hold of the economy and we have few options with which to adapt. Enter your superannuation.

Most banks these days offer offset accounts for mortgages, where any balance effectively reduces the principal of the loan and hence interest payments. We should be able to use our superannuation in a similar fashion, with the option of using both our employee and employer benefits, where possible, as an offset to the mortgage balance. The advantages of this would be many. Firstly it would enable mortgage holders to pay off their mortgages far more rapidly, reducing the number of under water mortgages and foreclosures as Australia’s property bubble deflates, as it must in a contracting economy. Secondly, it would effectively increase the savings rate of Australia’s banks, reducing the requirement for international borrowing and limiting the requirement for banks to raise interest rates. It might also pave the way for a transition to 100% reserve requirements in our banking system. For mortgage holders, it would essentially provide a rate of return equivalent to the banks interest rate on their superannuation. In a contracting economy this would be a very good return indeed.

Of course there would need to be safeguards, such as ensuring that the mortgage holders continue paying their minimum repayments, lending criteria are maintained and perhaps only a certain percentage of a mortgage could be offset. As the economy shrinks and the credit/debt bubble deflates, house prices are likely to fall, probably significantly. With the lending of three of the big fours banks favouring home mortgage lending, this would place significant stress on Australia’s banks. This proposal would reduce the likelihood of bank collapses by keeping the number of foreclosures and the rate at which home prices fall at more manageable levels.

So what are the downsides to such a plan? Interestingly enough, both the capitalisation of shares on the ASX and the value of superannuation investments were just over $1 trillion as of June 2009. If a large percentage of mortgage holders withdrew the superannuation from other forms of investment, such as the share market, it would possibly trigger a collapse in equity prices. If the global economy contracts, this will probably happen anyway, the benefit here being that you the superannuation investor have an alternative choice. It could also result in a downsizing of the financial industry; however economic specialisation has a tendency to decline as societies reduce to lower levels of complexity, so the numbers of financial planners are likely to decline regardless of this proposal. It would also reduce bank profits, but at the same time reduce the risk of bank failures, arguably a price worth paying.

With the Governments review into superannuation due soon, perhaps it is an appropriate time to consider our superannuation as tool to reduce the systemic risk to our financial system as we enter an era of limits and consequences.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon