Finally, although we are pessimistic about the long-term prospects of government debt, we are aware of the possibility of a near-term rally; especially if there is another round of risk aversion in the financial markets. So, if we do get another deflationary scare and bond prices rally, holders of government debt are best advised to liquidate their positions.

Furthermore, if our world-view is correct, extremely high inflation is now inevitable. As long as the monetary velocity in the US is weak, inflationary expectations will remain subdued, but once the economic activity picks up, the world will experience spiraling inflation. When that occurs, hard assets will protect the purchasing power of your savings. Accordingly, we have allocated a large portion of our clients' capital to energy (upstream companies, oil services plays and alternative energy plays), precious metals miners and diversified base metals miners.

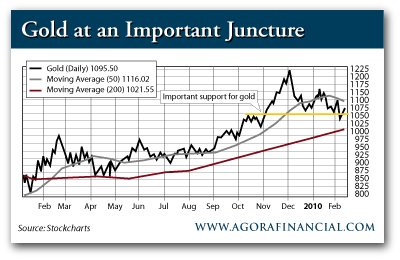

At the time of writing, precious metals are at a critical juncture and the price of gold is trading above an important support level.

Advertisement

Figure 2 shows that the price of gold peaked at US$1,075 in October 2009 and that level is now acting as important support. Now, if the bull-market's trend consistency is intact, then the price of gold must rally immediately and challenge its December high. At the very least, the price of gold must hold above US$1,075 per ounce. So, will gold manage to stay above this critical support level?

Before we attempt to answer this question, we must confess that short-term forecasting is extremely difficult and we really do not know what will happen over the following days. However, what we do know is that the macro-economic environment has never been better for the yellow metal. After all, mined supply is in decline, investment demand is rising, the public sector has become a net buyer of gold and hatred towards paper currencies is on the rise. Under these circumstances, we expect gold to perform very well. However, you must remember that the American currency is in rally mode and this is exerting downward pressure on all metals.

Now, if we were forced to take a stand at gunpoint, we would say that the odds of a rally in gold are 65/35. Accordingly, we are holding on to our positions in precious metals mining stocks and may consider lightening up during (northern) spring (which is when precious metals usually make an intermediate-term peak).

Figure 2

Now, if gold does the unexpected and breaks below US$1,075 per ounce, then we envisage a deeper correction to the US$1,000 per ounce level. Even if that happens, we will continue to hold on to our positions in gold mining companies, which have already depreciated in the ongoing stock-market correction.

Advertisement

Short-term setbacks notwithstanding, we continue to believe that hard assets are in a secular bull-market, which will probably end in a gigantic mania. According to our guesstimate, the bull-market will end in the latter half of this decade; at a time, when inflationary expectations are spiraling out of control.

Make no mistake, the policy actions of the past 18 months are extremely inflationary and once the American economy stabilises, we will experience a significant increase in the general price level. And before this is all over, government bonds will (once again) be recognised as “certificates of confiscation”.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

11 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon