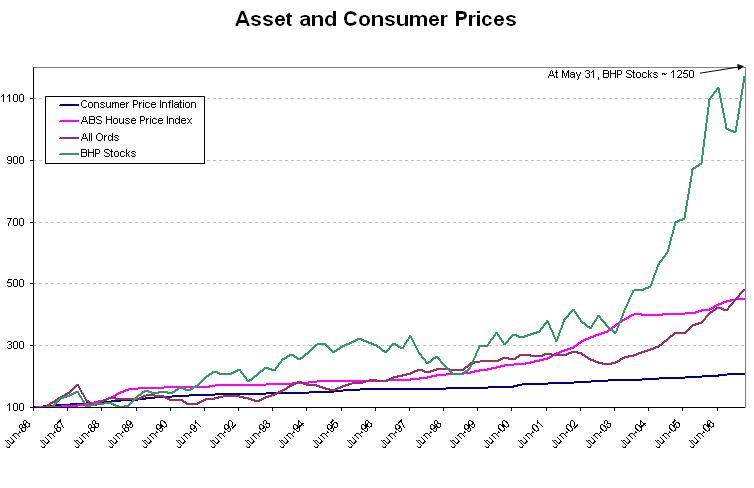

House prices have soared, share prices have rocketed, resource company shares have glowed in the dark, but consumer prices are subdued. The graph (see below) shows the extent of the dislocation between asset inflation and consumer inflation in Australian markets.

Take a moment to reflect on the magnitudes involved. Each price index is set at a value of 100 in June quarter 1986. By March 2007, consumer prices have slightly more than doubled, implying annual goods and services inflation of 3.8 per cent.

Over the same 21 years, average Australian house prices have risen by 450 per cent, the share price index has risen by a similar 480 per cent while shares in BHP Billiton have soared by a massive 1,150 per cent.

Advertisement

While the out-performance of BHP shares may in part, perhaps large part, be ascribed to the "China boom", other asset prices have risen by an order of magnitude faster than prices of goods and services.

This is a common theme around the world. China share prices have been rising almost vertically. In the mighty US, analysts worry about the next share price correction and the current house price correction. And in other nations, strong asset inflation co-exists with subdued consumer goods and services inflation.

Extreme asset inflation with subdued consumer inflation is a global phenomenon. Is it also a global problem? This is a big question for modern central banks and we encourage independent directors to ask RBA governor Glenn Stevens and his team for their answer at today's meeting of the board.

We need to be concerned because extreme booms in any market are followed by busts. The inevitable global asset price bust will create substantial misery.

This generation of policy makers has blamed loose monetary policy for past consumer inflation. The great damage created by past consumer inflation has led governments to give central banks a measure of "independence" and a mandate to fight goods and services inflation. This approach has been dramatically successful in all civilised countries.

A major part of the cost of consumer price inflation is the unemployment specifically, and unused resources generally, that accompanies the end of consumer price inflation. For example, the great inflation of the 1970s and 1980s in Australia was eventually killed by a recession that saw the measured rate of unemployment reach almost 11 per cent - with the effective rate far higher. Only now, half a generation later, is unemployment approaching an acceptable level.

Advertisement

Past asset price inflation has had major adverse economic consequences. Think about the ending of the Dutch tulip boom, or of the great Melbourne land boom of the 1880s or of the US stock market boom of the 1920s, arguably the first global asset boom. In each of these examples, the boom was followed by a bust and in the third case the bust was, like the preceding boom, also global.

In trying to avoid responsibility for asset booms, central bankers will undoubtedly argue that asset inflation relative to goods and service inflation may simply reflect a change in the attractiveness of assets relative to consumption.

A version of this argument was presented in The Weekend Australian, attributed to a wealthy executive from Macquarie Bank, whose market price has itself risen dramatically.

"It's a simple demand and supply equation," he said, pointing to the flood of savings going into superannuation and the strong outflow of capital from developing countries such as China, India and Russia to developed countries.

These flows may help to explain the rise in the price of Macquarie Bank shares, but they cannot explain the global rise in the relative value of assets compared with consumer goods and services.

I note in particular that the rise of China shares is itself relatively large, which cannot be due to a rise in capital flowing out of China!

The alternative theory is that the rise of China, India and Russia helps to explain the low level of goods and services inflation. The growth of manufacturing capacity in these and other developing nations has been matched by a flood of cheap workers to produce a global check to goods and services inflation notwithstanding excessively lax monetary policy in the major nations. The net result has been the spill-over of excess money into asset prices, as asset demand has run well ahead of supply.

Of the major developed nations, US monetary policy was the easiest, with the US Fed allowing cash rates to reach an amazingly low 1 per cent in 2003. Other central banks, including Australia's, have run monetary policy that was easy to a greater or lesser degree, and the resulting flood of cheap money has fuelled massive asset price inflation globally.

If this analysis reminds you of the debate over climate change, you have grasped the main points. And the consequences of too sudden corrective action would be similarly costly.

The question of course is what should be done about the situation. Easy money has helped fuel a global asset boom, and asset booms always lead to busts. So what can be done to avoid a bust?

It is a bit rich to see Alan Greenspan warning of the coming bust in China shares, when it was his policy that helped create that boom and the global asset boom in general.

Clearly, savage deflation is not the answer; just as inhibiting industry suddenly is not a sensible approach to global warming. The best approach may be to hold monetary policy firm while asset prices stabilise and then correct, easing only if the inevitable correction seems likely to turn into a bust. The problem is global, so a co-ordinated response among major central banks will be needed. There should be no complaints if Reserve Bank officials spend a disproportionate amount of time at the front of large aeroplanes.

In the longer term, in setting the degree of ease or tightness of monetary policy two matters need to be kept firmly in mind. The first is that global conditions must be well to the fore. The second is that asset inflation needs to be given equal weight to goods and services inflation.

First published in Henry Thornton and The Australian on June 5, 2007.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon