The Statement of the Federal Reserve of 20 March 2024 contained two paradoxes. The first paradox was the difference between the language of the official statement and the outlook that was then provided in the Summary of Economic Projections. The second paradox was within the estimates for GDP growth in the Summary of Economic Projections.

The paradox of policy

The language in the Statement seemed quite severe. It stated, "The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective." This seemed to indicate that the Fed would hold a stern position of firm monetary policy well into the foreseeable future.

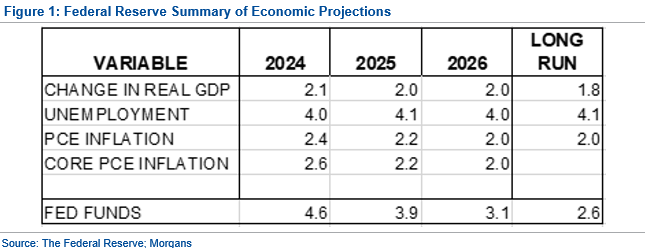

An examination of the Summary of Economic Projections, however, revealed that the Fed expected to reduce rates at least three times by the end of 2024. During this year, the Fed expected that the Fed Funds rate would fall from the current level of 535 basis points to a level at the end of 2024 of 460 basis points. This would involve three rate cuts of 25 basis points. This is a move towards decisively easier monetary policy.

Advertisement

The paradox of growth

The second paradox was within the estimates for GDP growth within the Summary of Economic Projections. The longer-term growth rate for GDP was shown at 1.8%. Usually, for inflation to fall, GDP growth would have to fall below 1.8%. This lower growth would allow rising unemployment. The higher unemployment would then generate lower inflation. Inflation would then fall to the target level of 2.0%. What happens is that for 2024, 2025 and 2026, growth is higher than the long-term average of 1.8%. Unemployment is flat through that three-year period, yet inflation falls to the target of 2.0%.

How is this possible? In answering questions during the press conference, Fed Chair Jay Powell explained this paradox to us. What was happening was that supply was improving in the economy. This increase in supply was driving down prices. During the pandemic he explained there was damage to both supply chains and to the labour market. He said that what was happening was that supply chains were healing as the economy was normalising. The labour market was also healing.

Powell noted that during the pandemic, the US lost several million workers. These workers left the workforce for fear of becoming ill. This effect was particularly severe in 2021 and 2022. This changed in 2023 as labour force participation recovered. Immigration had slumped in 2021. Powell said that this had recovered in 2023. This increase in the size of the workforce in 2023 had increased supply in the US economy, allowing inflation to ease. He noted that "growth is solid to strong. We have seen inflation come down." Then he went on "the base of labour market growth will narrow." This improvement in labour supply was coming to an end.

The solution of this paradox allows us to understand why growth in 2025 at 2% and growth in 2026 at 2% can be stronger than long-term growth of 1.8%, and yet inflation can fall. This is a temporary effect because of the recovery in the labour market. Others might call this simply good luck.

The Summary of Economic Projections suggests that there can be three cuts in the Fed Funds rate in 2024: three more cuts in 2025 and three more cuts in 2026. Indeed, 2027 will allow two further cuts to take the Fed Funds rate to 2.6%. Our view is rates may fall in 2024 and 2025, taking the Fed Funds rate to 3.9% by the end of 2025. At this point, rates will fall no further.

Advertisement

Our model of the Fed Funds rate suggests an equilibrium level of 3.8%. Other work by Summers and Blanchard of the Peterson Institute, suggests a final equilibrium of 4.0% (see references). This is because of the increasing real cost of maintaining a very high level of US government debt to GDP. Net debt to GDP near 100% of GDP will require both short rates and long-term rates, consistently higher than we have experienced in previous periods.

Still, until then, we may enjoy the benefits of a falling Fed Funds rate.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

1 post so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon