There is much anxious discussion today about the low economic growth rates, or 'secular stagnation', besetting the global economy. As many have noted, this has played a crucial role in the rise of anti-establishment 'populist' parties across the globe. But are mainstream economic theories – i.e. neo-classical, Keynesian, etc. – adequate for explaining the phenomena, or is a new 'biophysical' approach needed?

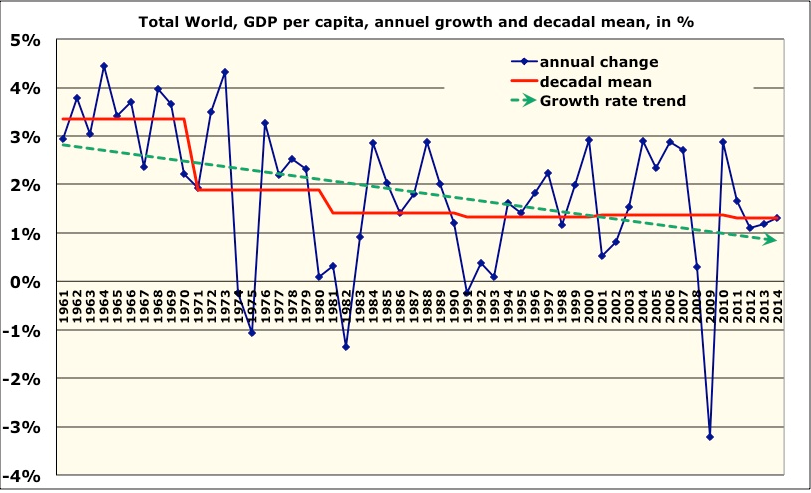

While most analysts have focused on the slowdown in GDP growth rates over the last decade, one can notice a declining trend beginning as far back as the 1960s. Jean-Marc Jancovici shows that in the 1960s world GDP per capita was increasing at +3.5 % per year, however, in the 1970s the rate declined to +2% on average across the decade, and for the last three decades it has been about +1.5%.

Advertisement

Source: World Bank, 2015

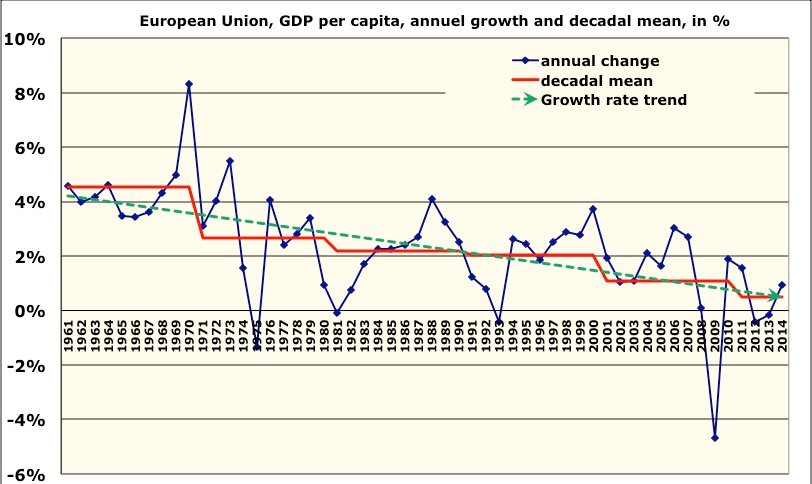

This global trend, of course, hides major regional variation – in Asia, for example, growth in per capita income has accelerated over the same period. The reason for the overall declining trend, is largely a consequence of the OECD countries (i.e. advanced industrial) which, until recently concentrated a large share of global GDP, but which have collectively experienced a much steeper decline in per capita income growth than elsewhere.

Source: World Bank 2015

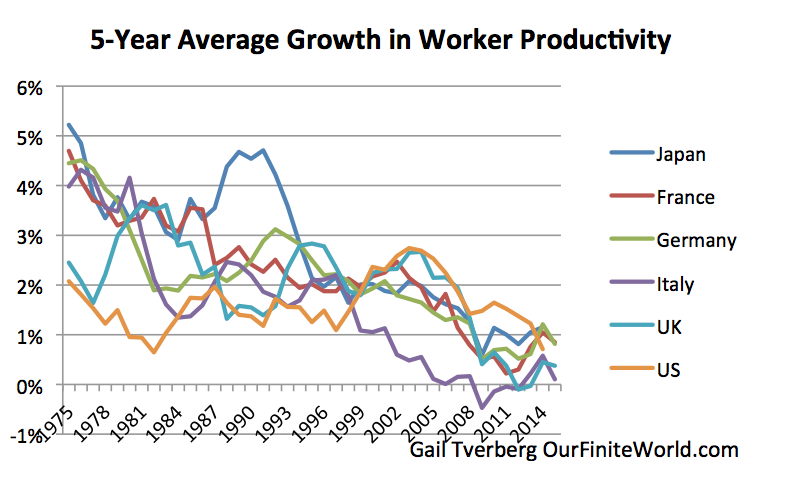

The decline in OECD income growth is strongly related to a parallel decline in labor productivity over the same period, which is not surprising given productivity improvement has long been understood a key driver of growth.

Advertisement

This declining rate of growth is more surprising given, much of it has been driven by spiraling rates of public and private debt. Beginning in the mid-1980s, the global debt to GDP ratio has increased dramatically to the point now where the global economy is saddled with an estimated $152 trillion worth of debt, which is equivalent to 225% of global GDP. And how have governments responded? Largely via monetary policies such as negative interest rates, which make credit (and thus debt) easier to attain in a desperate effort to restore historical growth rates – but so far to little avail.

These trends have sparked a wide-ranging debate among economists. Explanations have varied according to those that put more emphasis on supply-side against demand-side factors. On the supply side the slowdown in productivity has been attributed to diminishing returns from new technical innovations, whereas on the demand side, the problem is believed to lie in the decline in aggregate demand due to a build-up in the rate of saving. This demand side diagnosis is usually followed by a call for more active fiscal policy, or a redistribution of income towards lower income groups with a higher propensity to consume.

But despite their differences, what these theories all have in common is that they tend to look at factors 'internal' to the economic system – such as innovation levels, the rate of savings, rising inequality, or the lack of Keynesian fiscal stimulus – to explain low-growth. An emerging school of 'biophysical' economists, however, argue that these type of explanations, while no doubt valid to some extent, overlook the importance of factors 'outside' the formal economic system in the determination of growth. These economists argue that the theoretical models of conventional economics, by only factoring in capital and labour, overlook, or at least vastly underestimate, the contribution of resources – and particularly energy resources – in making economic growth possible. But given the reality of resource depletion, and particularly of fossil fuels, it is precisely this understanding of the economic system as a subset of a wider energy (and ecological) system that, biophysical economists argue, is key to understanding the current stagnation.

Bio-physical economists make two (related) claims about the connection between the depletion of energy resources and economic stagnation. The first regards the declining rate of growth in energy (and particularly oil) supply, and the second regards the declining rate of net energy delivered to society.

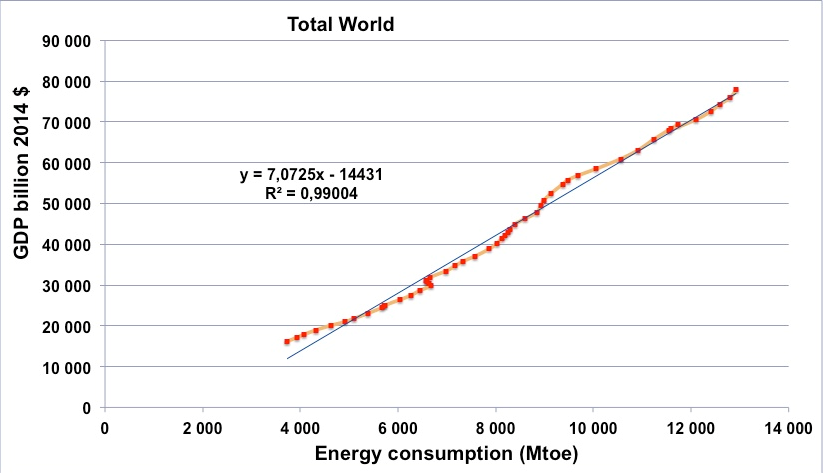

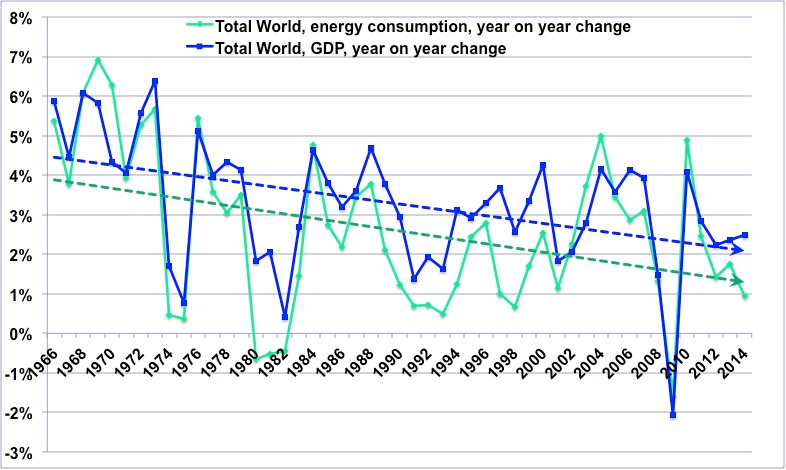

Regarding the rate of energy supply growth, French theorist Jean Jancovici alerts us to the tight historical correlation between economic growth and increased energy consumption. This can be seen clearly in the following graph.

Source: Jancovici's calculation based on primary information coming from BP statistical review (energy) and World Bank (GDP).

From this premise Jancovici contends that secular stagnation can chiefly be attributed to the declining rate of growth in per capita energy consumption which, he shows, is closely correlated to the declining income growth as noted above.

Source: Jancovici's calculation on primary data coming from BP statistical review & various sources before 1965 (energy) and World Bank (GDP).

At a global level, since the twin oil shocks of the 1970s, the growth in per capita energy supply has slowed, from an average growth rate of 2.5% per annum between 1860 to 1980, to just 0.4% per annum since 1980. And if one looks just at the OECD, per capita energy supply has entirely stagnated since the 1980s, with many countries now experiencing a gross decline. It's true that the increasing efficiency of energy use means we can get more GDP growth from every unit of energy, but efficiency gains have not made growth any less dependent on rising energy consumption and thus the declining rate of per capita energy growth, Jaconvinci contends, is a critical factor in explaining secular stagnation.

A key question here, however, is whether correlation implies causation? That is, does the tight relationship between the declining per capita energy growth rate and GDP, mean that the former always causes the latter? Jaconvici argues that it does because historically the drop in per capita energy supply growth usually preceded the drop in per capita GDP. But his charts, such as the one above, do not always show this clearly. It could be that GDP growth is slowing for other reasons and – given the strong dependence of growth on rising energy – this is merely reflected in the declining rate of energy supply. Thus, while Jaconvici thesis may be correct, its far from proven to be so. It seems likely that declining gross energy supply is just one factor among several that have historically caused the slow-down in growth.

Most biophysical economists place more stress on the significance of a second manifestation of energy depletion, which is likely to be impacting the economy, particularly since the roughly the turn of the century – that is, the declining rate of energy return on energy invested (EROI). This is different from gross energy supply, because it looks instead at what proportion of gross energy is being delivered to society, once allowance has been made for the energy need for the supply task. The problem, biophysical economist point out, is that with the peaking of conventional oil in 2005, the global economy has become increasingly dependent on unconventional source of oil and gas, which are far costlier, in both energy and financial terms, to extract.

This has resulted in a declining EROI ratio, with the EROI for oil & gas estimated to have fallen from about 35:1 in 2000 to about 17:1 today – and dropping. This declining EROI is, in turn, reflected in the rising costs associated for extracting energy. For example, whereas in the 1990s oil and gas exploration and discovery costs were rising at 0.9% per year, between 2000-2014 they rose by an average of 10.9% per year – a tenfold increase! What this effectively means is that the economy has to plough far more resources into the extractive sector, which leaves less remaining to fund the activities of the wider economy, let alone high growth rates. This not only helps to explain today's low-growth and stagnant real wages, but also the fact that what little GDP growth there is, is increasingly based on debt driven asset and financial bubbles (that will someday burst!), rather than real economic activity.

At this point, it may be asked, what about the current low oil price? Surely this is a sign of excess oil supply, rather than a lack of it? This is correct; the addition of (mainly) unconventional oil from Canada and the U.S has flooded the world market, outstripping demand and leading to the price collapse. But, as analysts such as Gail Tversberg have argued, this can be interpreted as a consequence of a fundamentally sick global economy, worn out under the weight of 14 years of almost continuously high oil prices and ever growing debt – the upshot being that investors and consumers simply could no longer afford the higher price. And while the current low oil price gives consumers a reprieve, it is a nightmare for oil producers who are rendered increasingly unprofitable and are rapidly accumulating unsustainable debts. Indeed as Tim Clarke argue, the current oil price is likely to be "lower than just the breakeven price of all but a small proportion of global oil reserves." Hence the current predicament of the global economy: oil prices that are too high cripple economic growth, but too low that they cripple oil producers.

Whatever one makes of these historical arguments, what seem undisputable is that increasingly deteriorating biophysical conditions will negatively impact on the economy in the near future. In terms of gross energy, the fundamental fact is that fossil fuels are finite resources and will all inevitably peak and decline. The situation for oil is especially critical. A recent HSBC report found that 83% of conventional oil fields are already post there peak in production, and that oil discoveries are at record lows. No wonder, notwithstanding the current oil 'glut', many predict a return to tight oil supply in the next few years, triggering a spike in the oil price and a recession of the debt-ridden global economy. But whatever the case, the global economy will in coming years be increasingly dependent on lower EROI unconventional fossil fuels, as well as even higher cost renewable energy, and all the problems that implies for growth.

Perhaps more importantly, the depletion of energy is only one aspect of the wider biophysical crisis, the impacts of which will certainly intensify in coming decades, including climate change, water stress, soil degradation and chemical build up. And meanwhile, as Nafeez Ahmed points out, "4.3 billion people - nearly two-thirds of the global population - live on less than $5 a day", suggesting further development from the poor majority will intensify the above pressures in all directions. A new book by Ahmed argues that these biophysical realities are already today crucial to understanding the growing turmoil and conflict in the Middle East, with a strong likelihood of spreading to other regions, including the affluent West in coming decades.

So irrespective of whether growth slows or stops soon, rich countries like Australia would be wise to get off that track anyway – better to do so by design rather than disaster.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon