The US November employment number of an extra 178,000 jobs for the month was greeted by the market as a fairly benign number. Sure, the number was strong enough to suggest that the Fed would increase interest rates at its meeting on 13 and 14 December. Still, the employment number was not the strongest in the past year. More importantly the growth rate of employment was declining. We can see this from Figure 1 below. Here we see the year on year growth rate of US payroll employment since January 2004.

Employment growth peaked way back in December 2014 at a rate of 2.33%. Since then employment growth has been declining. The year on year growth rate of employment for the year to November was only 1.58%. This is the slowest year on year growth rate recorded in calendar 2016. Surely this shows that growth in the demand for labour is only proceeding at a modest pace. Think again. What this slowing growth rate shows is not decline in demand. What this slowing growth rate is declining supply. Employment growth is slowing because there a fewer and fewer people available to give jobs to.

Advertisement

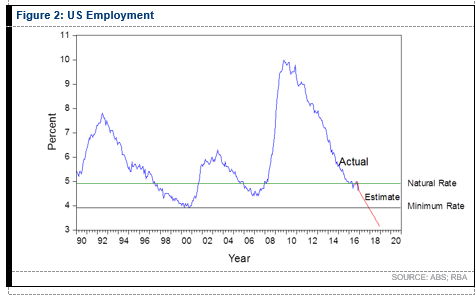

We can see the problem by looking at the level of US unemployment in Figure 2 on the next page. Figure 2 shows us the monthly level of unemployment since January 1990 as the blue line. Our projection of unemployment should it continue to decline at the current rate is shown as the red line. The green line shows the natural rate of unemployment. The natural rate is the level below which wage growth starts to put upward pressure on inflation. We calculate that the natural rate of unemployment is now 4.9%.

The black line is the minimum level of unemployment that has been recorded in the United States since January 1990. We calculate that the minimum level of unemployment since January 1990 is 3.9%. Experience shows us that when unemployment falls to this level, the level of graduate unemployment declines to around 1.2%. At that level, there are no more qualified people available to move around the US economy to generate more growth.

Wages growth becomes exponential. Core inflation breaks out above the Fed targets. Experience shows us that the Fed then intervenes aggressively to slow economic expansion. It is this process that the late Rudiger Dornbusch was thinking of when he said "US expansions do not die of old age; they are murdered by the Fed".

What the Fed has told us that it wants to do is to slow the growth rate of the US economy so that it stabilises unemployment below the natural rate of unemployment but above the minimum rate of unemployment. Should it succeed in doing this, then it will combine modestly rising living standards at the same time as avoiding the next US recession.

What concerns us is how the Fed actually achieves this. The red line in Figure 2 shows our projection of unemployment. This is where unemployment will go if it continues to decline at the same rate as it has in the past year. We can see that the red line continues to decline as we go through 2017. Our estimate of future US unemployment collides with the minimum rate of unemployment at 3.9% in December 2017. For the Fed to avoid a recession in 2018, it has to have slowed the decline of unemployment and stabilised it in a sideward path before we reach the second half of next year.

Advertisement

The first thing we can conclude from that is that the Fed needs to act more rapidly and more aggressively than the market may think. Firstly, it must definitely increase rates in December 2016. There is more than that. In order to slow the decline of unemployment, the Fed needs to start moving up rates on a regular basis from now on.

We think there will be at least three further rate increases in 2017. The same will be needed in 2018. There may be more rate hikes than this. We remember that the incoming Trump administration will be cutting corporate tax rates in 2018.

Conclusion

These tax cuts expand the US budget deficit and provides additional stimulus at that time. With the economy at full employment in 2018, the Fed will need to further increase rates to soak up some of that stimulus. Rates may begin to normalise very rapidly. We could begin to move to higher rates much more quickly than the market currently thinks.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

3 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon